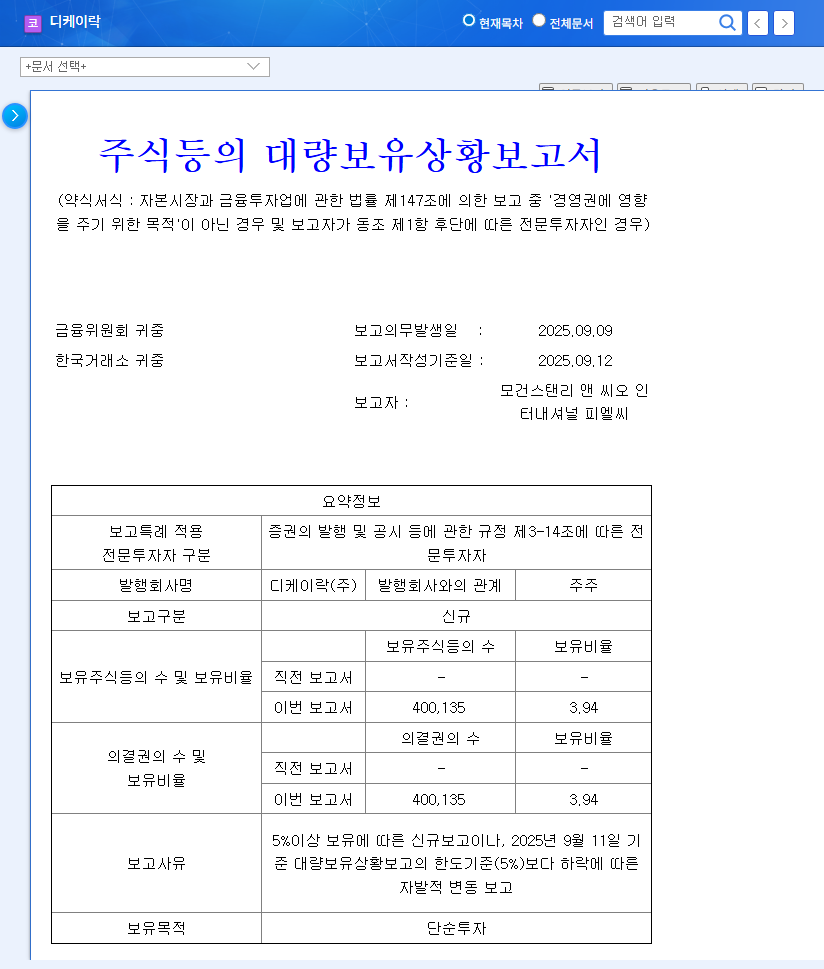

The latest NOVATECH Shareholding Report has caught the attention of the investment community, revealing key insights into the company’s leadership and stability. While the report, filed on November 14, 2025, shows no change in CEO Oh Chun-taek’s significant 54.28% stake, the nuances behind this filing warrant a much deeper look. This comprehensive NOVATECH stock analysis will unpack the report’s implications, weigh management stability against current performance challenges, and provide a clear roadmap for potential and current investors.

We’ll explore NOVATECH’s financial health, the macroeconomic headwinds it faces, and what strategic moves investors should be monitoring in the coming quarters.

Deconstructing the Shareholding Report

What Did the Report Actually Say?

On November 14, 2025, NOVATECH Co., Ltd. filed its ‘Report on the Status of Large Shareholdings, etc.’. The key figure, CEO Oh Chun-taek, confirmed his holding of 54.28% of the company’s shares. The official purpose cited was ‘management influence,’ reinforcing his long-term commitment. Crucially, the filing reason was noted as ‘on-market trading and collateral contract change (extension).’ The full filing can be reviewed in the Official Disclosure (DART).

While ‘no change’ might sound uneventful, the extension of a collateral contract is significant. It suggests the CEO is using his shares as collateral for financing, and the extension indicates a stable, ongoing relationship with lenders, mitigating risks of a forced sale and reinforcing financial stability at the leadership level.

A majority stake held firmly by the CEO is a powerful signal of management stability. However, this stability must be weighed against the company’s real-world performance and market challenges.

NOVATECH Financial Health & Market Pressures

A Mixed Performance Picture

An honest NOVATECH stock analysis must acknowledge the recent performance dip. In the first half of 2025, revenue fell to KRW 29.2 billion (a 5.2% YoY decrease), while operating profit saw a more significant drop to KRW 5.63 billion (-20.3% YoY). This was attributed mainly to reduced sales of general shielding magnets. However, the company is not standing still. An uptick in core material sales shows a positive trend in portfolio diversification.

Despite the profit decline, NOVATECH’s financial health remains exceptionally robust. Key indicators include:

- •Low Debt: A remarkably low debt-to-equity ratio of just 5.45% signals minimal financial risk.

- •Strong Cash Flow: Operating cash flow improved dramatically to KRW 13.402 billion, a testament to efficient operations.

- •Commitment to Innovation: R&D spending at 4.1% of sales demonstrates a focus on future growth and technological competitiveness. Interested readers can learn more by reading about how to analyze tech company R&D spending.

Global Exposure and FX Volatility

With a staggering 95% of its sales generated overseas, NOVATECH’s performance is intrinsically linked to the global economic climate and currency fluctuations. The company’s sensitivity is acute: a mere 10 KRW change in the USD/KRW exchange rate can swing profits by approximately KRW 1.845 billion. As the USD/KRW rate hovers near KRW 1,458, effective currency hedging is not just a strategy—it’s a necessity. Investors should monitor global economic trends, such as those reported by authoritative sources like Reuters, to anticipate potential impacts on NOVATECH.

Investor Takeaways & Strategic Outlook

This NOVATECH Shareholding Report is a vote of confidence in management’s long-term vision. However, the market demands more than just stability; it demands growth. For a prudent investment strategy, here are the key areas to monitor:

- •Turnaround in Profitability: Watch for a rebound in revenue and operating profit. Can the growth in core materials offset the decline in legacy products and drive the company forward?

- •FX Risk Management: Scrutinize quarterly reports for comments on the company’s hedging strategies and their effectiveness against currency volatility.

- •R&D Pipeline: Look for announcements of new products or patents resulting from their consistent R&D investment. This is the primary source of new growth engines.

- •Global Market Health: Keep an eye on the economic health of key export markets, as this will directly influence sales volumes.

In conclusion, while the report confirms rock-solid management stability, the true catalyst for NOVATECH’s stock will be a clear demonstration of performance recovery and innovation-led growth. A long-term, analytical approach is essential.

Frequently Asked Questions

What does the CEO’s 54.28% stake signify?

It signals an exceptionally high level of management stability and a strong, long-term commitment from the company’s leader, Oh Chun-taek. It aligns his interests directly with those of shareholders.

Is NOVATECH’s recent performance a cause for concern?

The H1 2025 decline in revenue and profit is a challenge that needs to be monitored. However, the company’s excellent financial health (low debt, strong cash flow) provides a solid foundation to navigate this period and invest in future growth.

What are the biggest risks for NOVATECH investors?

The two primary risks are its high dependency on overseas sales, making it vulnerable to global economic downturns, and its sensitivity to foreign exchange rate fluctuations, which can directly impact profitability.