In-Depth Hyundai Livart Investment Analysis for 2025

This comprehensive Hyundai Livart investment analysis delves into the furniture and interior giant’s remarkable 2024 profit turnaround and its strategic vision for 2025 and beyond. As the company prepares for a crucial Investor Relations (IR) event, investors are closely watching, seeking clarity on its growth trajectory amidst a challenging economic landscape. This article will provide a detailed breakdown of the company’s fundamentals, potential stock catalysts, and the critical questions that need answers.

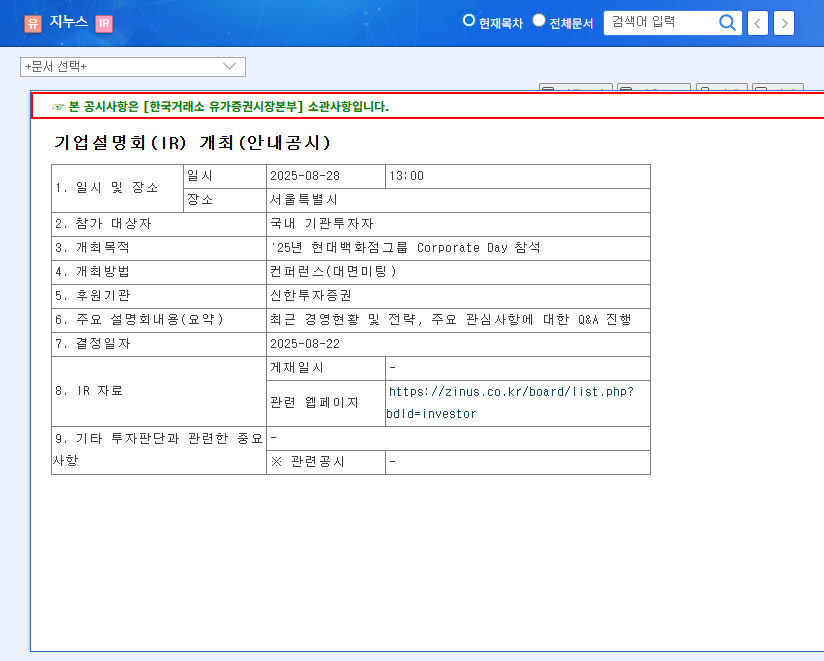

Hyundai Livart has formally announced it will host an Investor Relations (IR) event on November 12, 2025, at 09:10 AM to enhance investor understanding. The event, which will cover the current business status and future strategies, is a pivotal moment for evaluating the Hyundai Livart stock. For verification, you can view the Official Disclosure on the DART system.

Fundamental Deep Dive: The Bull & Bear Case

An IR event is a window into a company’s soul. For Hyundai Livart, it’s a chance to build on the positive momentum from 2024. Here’s a look at the core fundamentals shaping investor sentiment.

The Bull Case: Why Investors are Optimistic

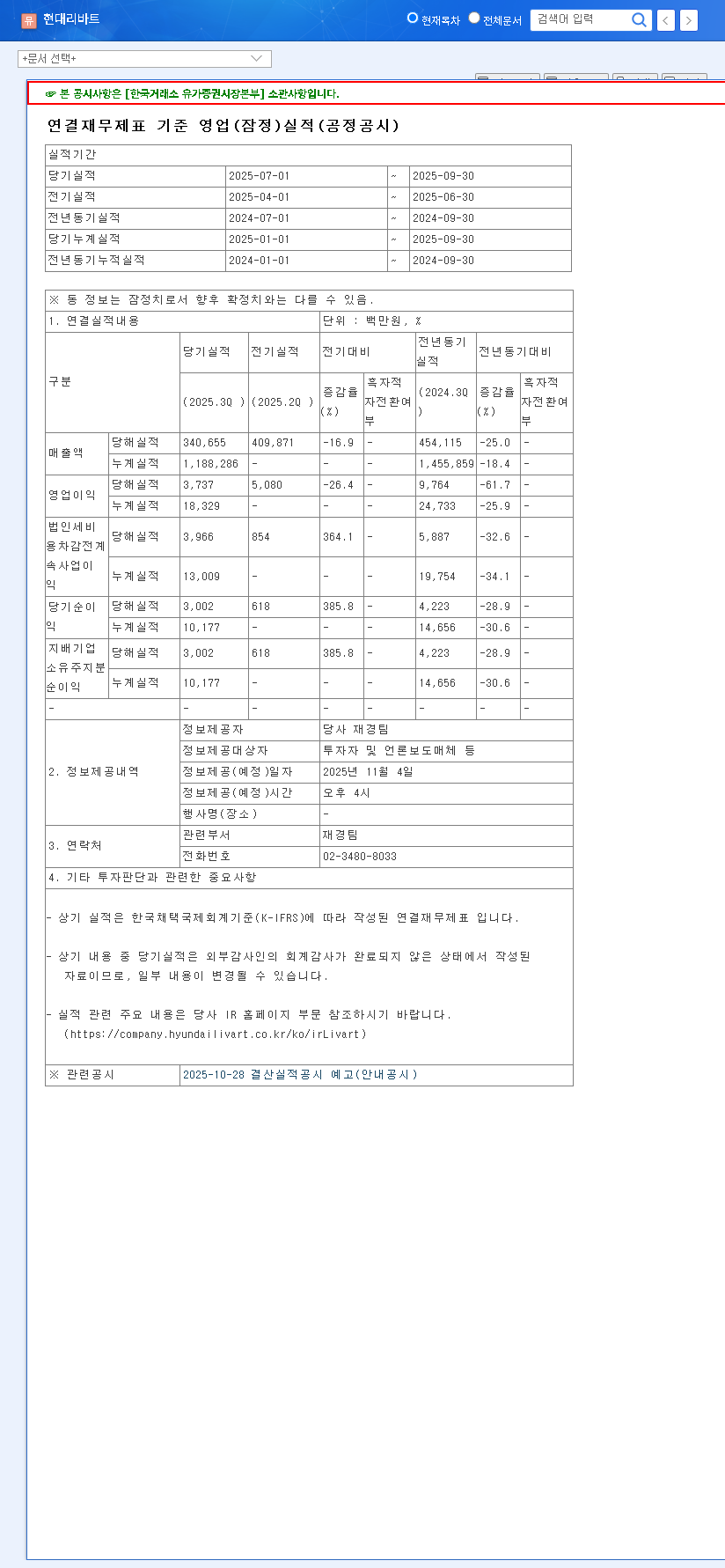

Several strong performance indicators from 2024 suggest a robust foundation for future growth, forming the core of a positive Hyundai Livart investment analysis.

- •Explosive Built-in Business Growth: The built-in segment was a star performer, with sales reaching KRW 638.8 billion—a staggering 36.4% year-over-year increase. This signals strong relationships with major construction partners and a powerful hold on the B2B market.

- •Profitability Turnaround: The shift from an operating loss in 2023 to a KRW 24 billion profit in 2024 is a testament to effective cost management and operational efficiency. This financial discipline is a major confidence booster for investors.

- •Strategic ‘Space Re-Creator’ Vision: The Hyundai Livart future strategy aims to transform the company into a ‘Space Re-Creator.’ This involves launching customized B2C space solutions and package deals, moving beyond just selling furniture to selling holistic living experiences, a key differentiator in a crowded market. More details can be found in our analysis of the Korean interior design market.

- •Rock-Solid Financials: A debt-to-equity ratio of just 47.93% indicates a healthy and stable financial structure, giving the company resilience and flexibility to navigate economic uncertainty.

The Bear Case: Headwinds and Potential Risks

Despite the positives, investors must consider significant external and internal risks that could impact the Hyundai Livart stock performance.

- •Real Estate Market Slowdown: The health of the built-in business is directly tied to the real estate and construction sectors. A prolonged downturn, as reported by outlets like Bloomberg, could lead to a sharp reduction in orders.

- •Macroeconomic Pressures: Persistent high interest rates and inflation directly squeeze consumer discretionary spending, which could weaken demand in the crucial B2C home furnishing segment.

- •Exchange Rate Volatility: With overseas operations, including new orders in Saudi Arabia, fluctuations in currency exchange rates can introduce unpredictability to earnings and profitability.

- •Compliance and Governance: Past issues with the Fair Trade Commission, while addressed, remain a potential risk to corporate credibility if not managed with transparent and robust compliance systems going forward.

The upcoming Hyundai Livart IR event is a critical juncture. The company’s ability to convincingly articulate its strategies for mitigating real estate risks while capitalizing on its ‘Space Re-Creator’ vision will likely determine the stock’s direction for the coming year.

Investor Action Plan: Key IR Focus Points

For investors tuning into the IR, here are the key areas to scrutinize to make an informed decision about this furniture company stock.

- •Real Estate Counter-Strategy: Look for specific, actionable plans to counter the housing market slowdown. Are they diversifying into the remodeling market or developing new business models less dependent on new construction?

- •B2C Growth Metrics: How will the ‘Space Re-Creator’ vision translate to tangible revenue? Ask for concrete KPIs, market share targets, and brand investment plans.

- •Profitability Sustainability: Are the 2024 cost savings sustainable? What is the strategy for improving margins further, such as focusing on high-value products or leveraging new technology?

- •ESG and Governance Commitment: How is the company strengthening its compliance and ESG framework? Clear communication on this front is crucial for building long-term trust.

Overall Opinion

Hyundai Livart stands at a promising yet challenging crossroads. The company has demonstrated impressive operational strength and a clear vision for the future. The upcoming IR event will be the ultimate test of its leadership’s ability to articulate a convincing narrative that addresses legitimate investor concerns. A clear, confident, and transparent presentation could unlock significant value and foster positive sentiment around the stock.

Disclaimer: This report is based on publicly available information and is for informational purposes only. It does not constitute an inducement for investment. All investment decisions must be made at the investor’s own discretion and responsibility.