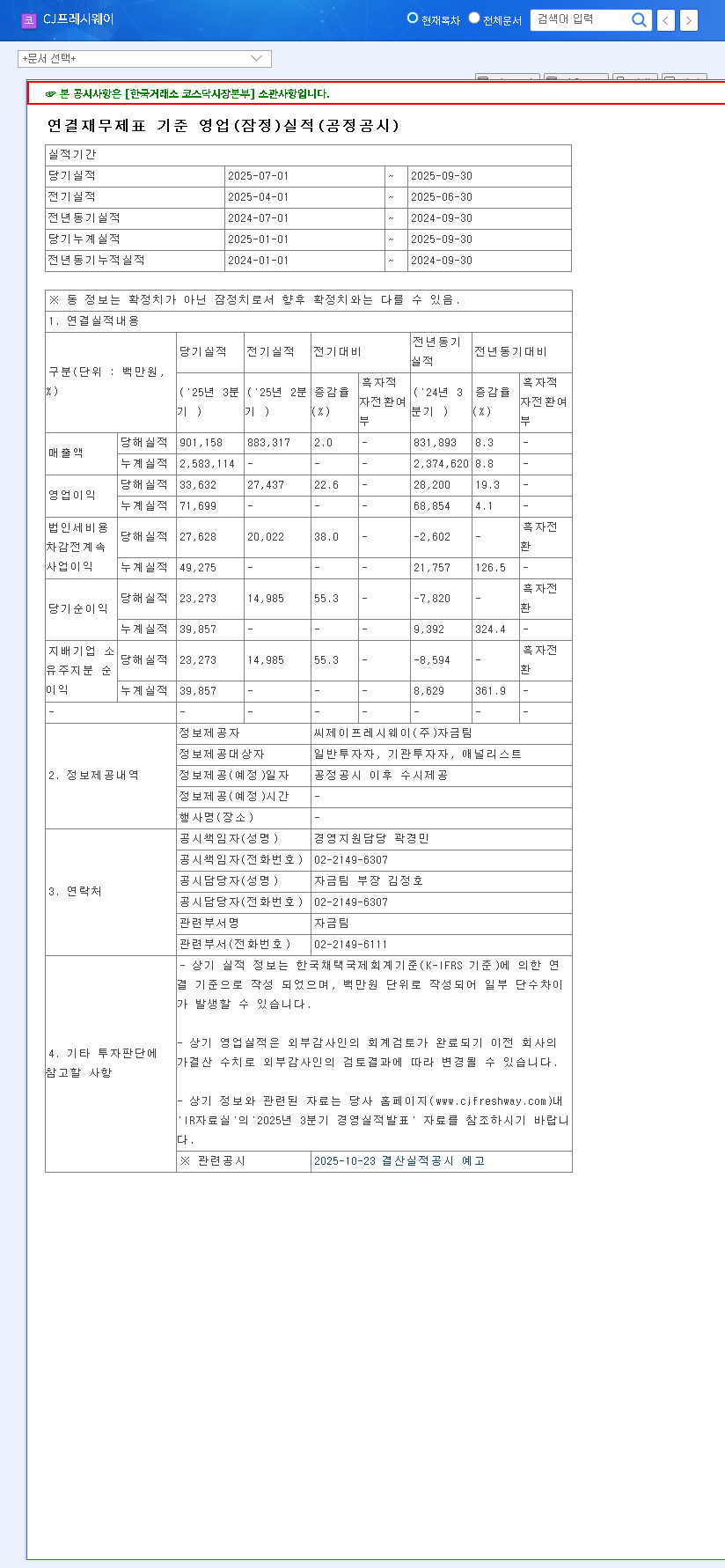

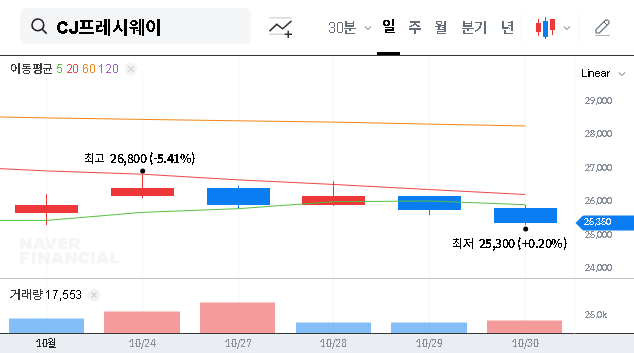

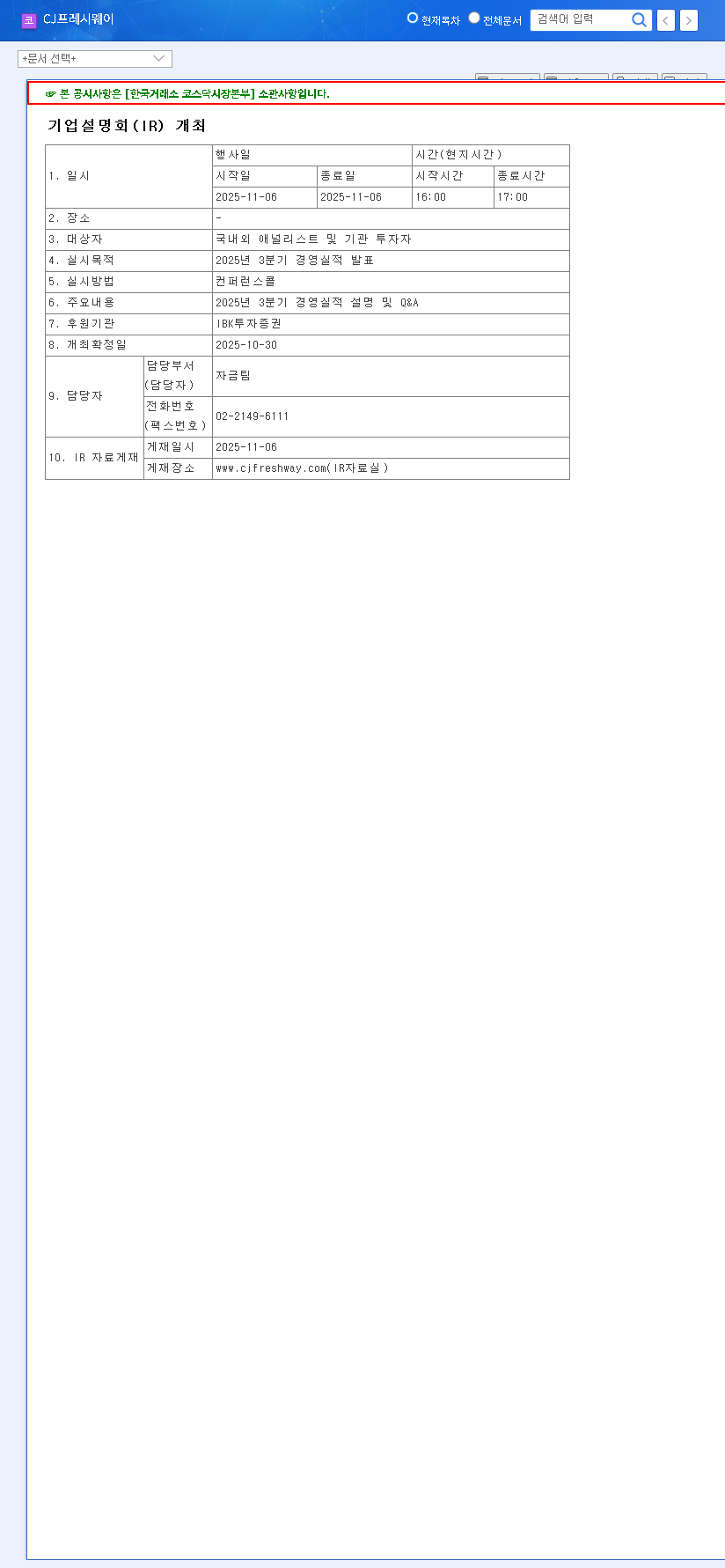

The upcoming CJ Freshway IR (Investor Relations) event is set to be a pivotal moment for the company (CJ프레시웨이) and its stakeholders. Despite reporting a commendable 9.02% revenue increase in the first half of 2025, the company faces a troubling financial reality: plummeting profitability and a negative operating cash flow. This paradox has created significant uncertainty in the market, placing immense pressure on management to deliver a clear and convincing turnaround plan.

This comprehensive CJ Freshway financial analysis delves into the core issues plaguing the company, examines the macroeconomic headwinds, and outlines the critical points investors must scrutinize during the IR. Can the leadership team quell anxieties and present a viable CJ Freshway growth strategy that reignites confidence?

The H1 2025 Financial Paradox: Growth Without Profit

On the surface, CJ Freshway’s top-line growth seems robust. However, a closer look at the numbers reveals a concerning decline in financial health and operational efficiency. This disconnect is the central theme heading into the CJ Freshway IR event.

Key Financial Performance Summary (H1 2025)

- •Revenue Growth: Achieved KRW 1,681.95 billion, a year-on-year increase of 9.02%, driven by food ingredients distribution (+11.87%) and food services (+5.74%).

- •Operating Profit Decline: Dropped to KRW 38.07 billion, a decrease of 6.37% from the previous year, highlighting severe margin compression.

- •Net Profit Collapse: Plummeted to KRW 16.58 billion, a staggering 39.49% year-on-year decline.

- •Negative Operating Cash Flow: Turned negative to -KRW 3.98 billion, a significant deterioration that signals potential liquidity challenges.

- •High Debt-to-Equity Ratio: Stood at a concerning 264.68%, increasing the company’s financial risk profile.

Compounding these issues is a fine of approximately KRW 24.5 billion levied in August 2024 for a Fair Trade Act violation, which casts a shadow on both financial health and corporate governance. Further details can be found in the Official Disclosure (DART).

Diagnosing the Decline: Internal and External Pressures

CJ Freshway’s deteriorating profitability is not the result of a single factor but a perfect storm of internal cost pressures and a volatile macroeconomic landscape.

The core challenge for CJ Freshway is proving it can translate top-line growth into bottom-line results amidst rising costs and economic uncertainty. The upcoming IR is their primary stage to make this case.

Internal Cost Headwinds

- •Raw Material Inflation: Persistent increases in global food commodity prices have directly squeezed gross margins.

- •Soaring Logistics Costs: Elevated oil prices and global freight rates have significantly increased the cost of distribution, a core part of their business.

- •Working Capital Strain: A buildup in inventory combined with a reduction in accounts payable has negatively impacted cash flow. For more on this, see our guide on how to analyze a company’s cash flow statement.

External Macroeconomic Factors

Global economic trends are further exacerbating the situation. As reported by leading financial outlets like Bloomberg, central banks worldwide are tightening monetary policy.

- •Exchange Rate Volatility: A rising USD/KRW exchange rate inflates the cost of imported goods, directly impacting costs.

- •Rising Interest Rates: Increased rates will escalate interest expenses on the company’s substantial debt load, further pressuring net income.

Investor Focus: Key Questions for the CJ Freshway IR

The success of the IR event hinges on management’s ability to provide concrete, actionable answers. Investors should look beyond vague promises and demand a specific CJ Freshway growth strategy. Key areas of scrutiny include:

- •Profitability Roadmap: What specific cost-control measures (e.g., procurement optimization, logistics efficiency) are being implemented? How will profitability be enhanced in the core food service segment?

- •Cash Flow Improvement: What is the plan to improve working capital management and return operating cash flow to positive territory?

- •New Business Ventures: What are the tangible revenue models and growth projections for the new ‘Freight Transport Brokerage’ and ‘Online Welfare Mall’ businesses?

- •Risk Management: How will the Fair Trade Act fine be managed, and what compliance measures are in place to prevent recurrence and restore trust?

Conclusion: An Investor’s Action Plan

The CJ Freshway IR is more than a standard corporate presentation; it’s a litmus test for the company’s future. For investors, the path forward requires careful listening and critical analysis. A vague or defensive presentation could signal continued struggles, while a transparent, data-driven plan could restore confidence and create a buying opportunity.

Ultimately, a successful CJ Freshway financial analysis will depend on the company’s ability to demonstrate a clear path to sustainable, profitable growth. Investors must weigh the potential of new strategies against the execution risks and persistent macroeconomic challenges to make a well-informed decision.