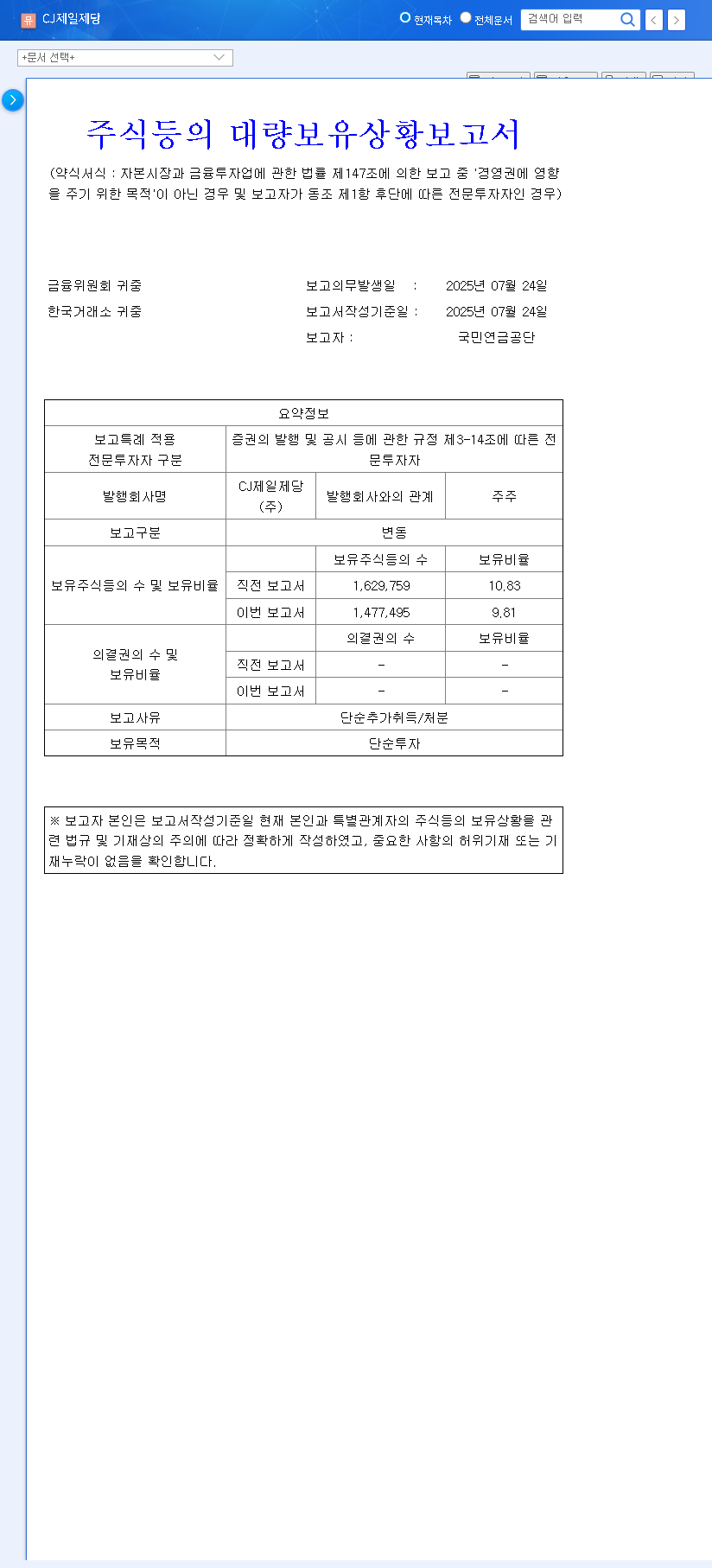

The upcoming CJ CHEILJEDANG CORP. IR for its third-quarter 2025 performance is more than just a financial report; it’s a critical look into the engine room of a global food and biotechnology powerhouse. As the company navigates ambitious K-Food globalization efforts and manages a complex portfolio, investors are keenly watching. This deep-dive analysis will unpack the key fundamentals, potential market-moving factors, and strategic considerations you need to understand ahead of this pivotal event.

Can CJ CheilJedang maintain its growth trajectory amidst macroeconomic headwinds? How are its investments in next-generation food tech and sustainable materials paying off? We’ll explore these questions and provide a comprehensive framework for interpreting the results.

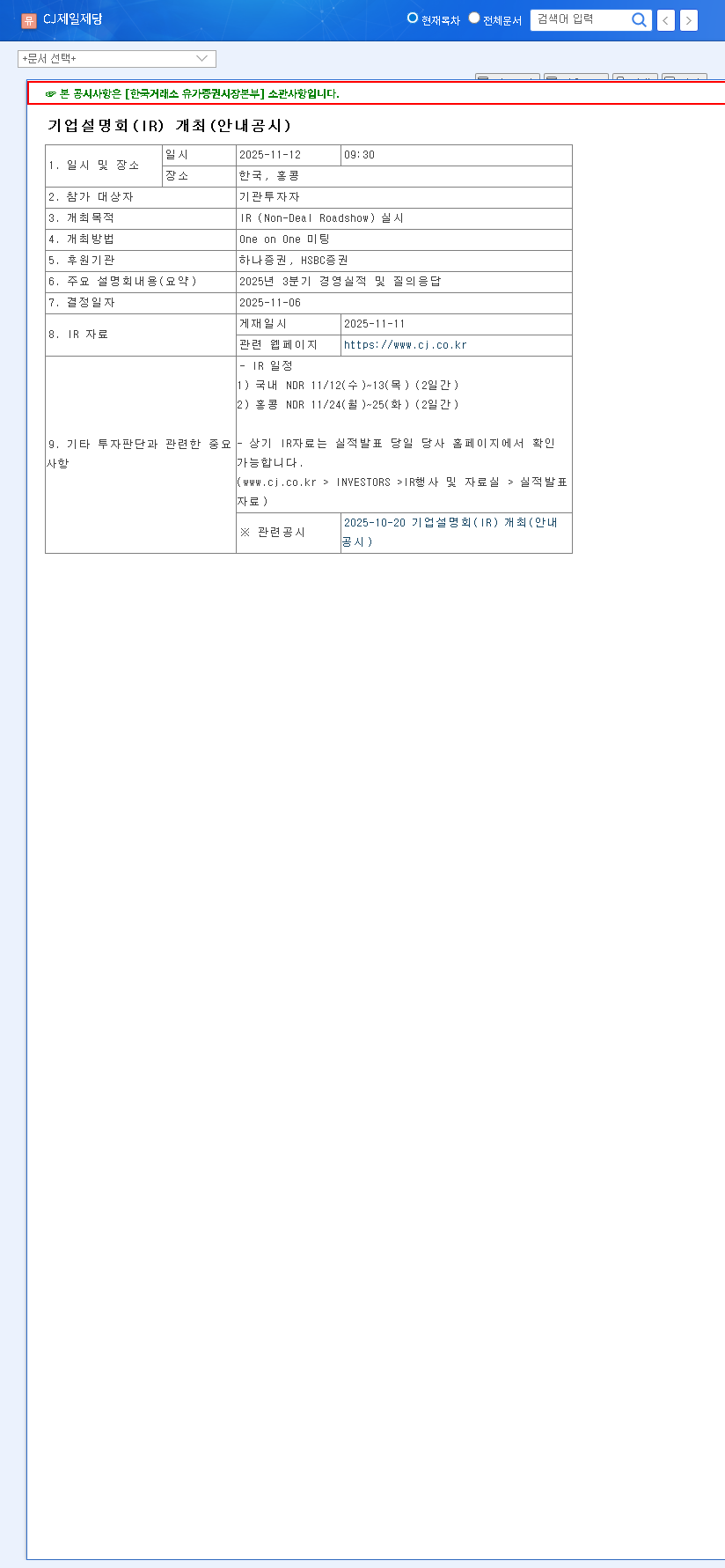

Event Details: The CJ CHEILJEDANG CORP. Q3 2025 IR

CJ CHEILJEDANG CORP. has officially scheduled its Investor Relations (IR) event to announce its Q3 2025 management performance. This session, which includes a detailed presentation and a live Q&A, is a crucial communication channel for stakeholders.

- •Date: November 12, 2025

- •Time: 9:30 AM (KST)

- •Focus: Q3 2025 Financial Results, Business Segment Performance, and Future Outlook.

- •Source: View the Official Disclosure on DART.

Fundamental Analysis: The Pillars and Pressures

A thorough CJ CheilJedang stock analysis begins with its core strengths and potential vulnerabilities. The company’s diversified model is a key asset, but it also creates multiple fronts to manage.

Core Strengths Driving Growth

- •Financial Stability: With a manageable debt-to-equity ratio, significant cash reserves, and a strong credit rating (AA/A1), the company is well-positioned to fund growth and weather economic downturns.

- •Aggressive Global Expansion: The landmark acquisition of Schwan’s Company in the U.S. was a game-changer, providing a powerful platform for its K-Food globalization strategy. Brands like Bibigo are now household names in many international markets.

- •Future-Proofing R&D: CJ CheilJedang is investing heavily in future growth engines. This includes the high-potential alternative meat sector, health functional foods, and the commercialization of PHA, a biodegradable plastic that meets rising consumer demand for sustainability.

- •Commitment to ESG: With clear targets for carbon neutrality and zero waste by 2050, the company is aligning with the values of modern investors and consumers, which can enhance long-term brand loyalty and investment appeal.

Potential Risks on the Radar

- •Commodity Price Volatility: The processed food business is sensitive to fluctuations in international grain prices and currency exchange rates. While hedging strategies are in place, significant swings can still impact profit margins.

- •Intense Market Competition: The global food industry is fiercely competitive. CJ CheilJedang faces challenges from both established international giants and agile local players, especially as consumer tastes diversify.

- •Profitability in Logistics: The logistics arm of the business operates with high fixed costs, making it vulnerable to market slowdowns and economic downturns that affect shipping volumes and rates.

The central theme of the CJ CHEILJEDANG CORP. IR will be balancing the exciting growth in its BIO and global food segments against the need to defend profitability in its more mature domestic and logistics markets.

Market Expectations and Stock Price Impact

The market will be scrutinizing the Q3 results for signs that the BIO business’s upward trend is sustainable and that the company is effectively managing costs in its food division. The CJ CheilJedang investor relations team’s commentary will be just as important as the numbers themselves.

Short-Term Volatility (Post-IR)

Expect increased stock volatility around the announcement. A bull case would be driven by better-than-expected margins in the food segment and continued double-digit growth in the BIO division. Conversely, a bear case could emerge if rising costs significantly erode profits or if global sales show signs of slowing. Management’s confidence and clarity during the Q&A will be critical in shaping immediate market sentiment.

Medium to Long-Term Outlook

Beyond the initial reaction, long-term value will be determined by the market’s belief in the company’s growth narrative. If the CJ CHEILJEDANG CORP. IR successfully conveys a clear and credible roadmap for continued K-Food expansion and profitability from new ventures, it could support a sustained positive re-rating of the stock. For more on this sector, you can read our Guide to Investing in Korean Food Stocks.

Actionable Investment Strategies

Investors should approach this event with a strategic mindset. Here are key areas to focus on:

- •Analyze Profit Margins: Look beyond top-line revenue. Dig into the operating profit margins for each business segment (Food, BIO, Logistics) to understand the true health of each division.

- •Listen for Forward Guidance: Pay close attention to management’s outlook for Q4 and the coming year. Any commentary on raw material costs, consumer demand, and new product launches will be invaluable. Check reputable sources like Reuters for broader market context.

- •Monitor Macroeconomic Factors: Keep an eye on currency trends (especially USD/KRW) and commodity prices, as these external factors will continue to influence performance.

- •Adopt a Long-Term View: While short-term price swings are likely, successful investing in a company like CJ CheilJedang requires focusing on its long-term strategic execution and intrinsic value.

Frequently Asked Questions

Q1: When is the CJ CHEILJEDANG CORP. Q3 2025 IR event?

The IR event is scheduled for November 12, 2025, at 9:30 AM Korean Standard Time. It will cover the Q3 earnings and include a Q&A session with management.

Q2: What are the company’s main strengths?

Key strengths include a solid financial foundation, successful global expansion via its K-Food globalization strategy, investment in future growth areas like alternative proteins, and a strong commitment to ESG principles.

Q3: What are the primary risks for investors?

Investors should monitor risks such as raw material cost volatility, intense competition in the global food market, the logistics business’s sensitivity to economic cycles, and the initial costs associated with R&D investments.

Disclaimer: This analysis is based on publicly available information and is intended for informational purposes only. It does not constitute investment advice. All investment decisions should be made by the investor after conducting their own due diligence.