The latest DONGWON INDUSTRIES Q3 2025 Earnings announcement has painted a complex but intriguing picture for the market. While the company celebrated a robust revenue beat and a staggering 520% explosion in net profit, a slight miss on operating profit has left investors with critical questions. This report offers a comprehensive deep dive into these mixed signals, analyzing the fundamental drivers, segment-by-segment performance, and the strategic outlook for Dongwon Industries stock. Our goal is to equip you with the clarity needed to make well-informed investment decisions in a volatile market.

Breaking Down the DONGWON INDUSTRIES Q3 2025 Earnings Report

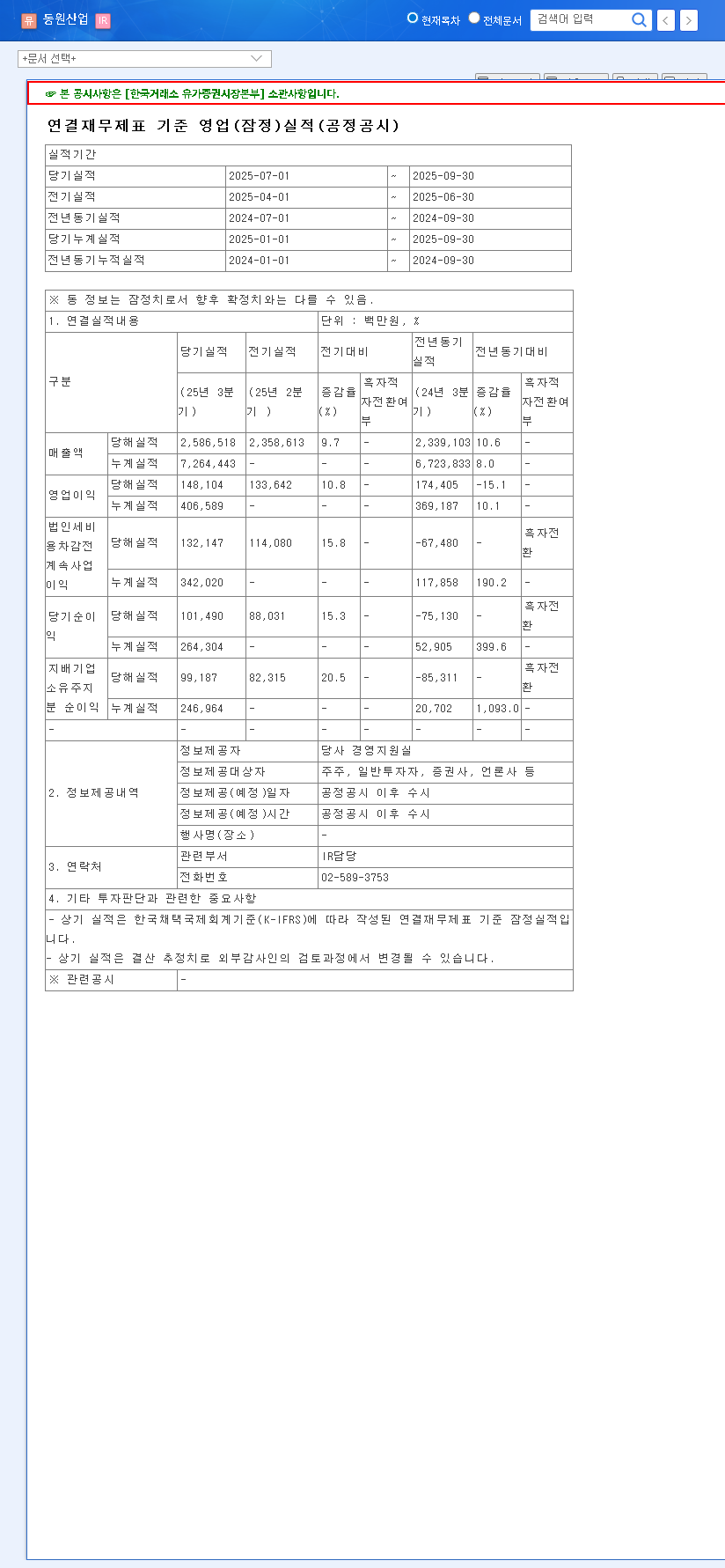

On November 7, 2025, DONGWON INDUSTRIES CO., LTD released its preliminary consolidated financial results, sending a wave of mixed signals. While top-line growth was strong, underlying profitability faced headwinds. Here are the headline figures compared to market consensus estimates, based on the Official Disclosure:

- •Revenue: KRW 2,586.5 billion, a healthy +4.0% above market estimates.

- •Operating Profit: KRW 148.1 billion, falling -6.7% short of forecasts.

- •Net Profit: KRW 99.2 billion, an astonishing +520.0% surge over expectations.

Analysis: The Story Behind the Numbers

Robust Revenue Fueled by Core Segments

The impressive top-line growth suggests resilient consumer demand and strong performance in Dongwon’s key business areas. The food and logistics segments likely served as the primary growth engines. This positive signal indicates that the company’s market positioning and brand strength remain formidable, allowing it to capture value even in a challenging economic climate. To dive deeper into market trends, investors can consult authoritative sources like Reuters Business News.

Operating Profit Squeeze: A Tale of Rising Costs

The shortfall in operating profit is a critical data point. It strongly implies that Dongwon Industries is grappling with significant cost pressures. These likely stem from a combination of elevated raw material prices (such as tuna and aluminum), increased global logistics costs, and persistent wage inflation. Furthermore, intensified competition in the packaging segment and potential margin deterioration in fisheries could have compounded this issue, preventing the strong revenue from translating into expected operational earnings.

Decoding the 520% Net Profit Anomaly

The extraordinary leap in net profit is the highlight of the DONGWON INDUSTRIES Q3 2025 Earnings. This surge is almost certainly driven by non-operating factors. Potential causes include significant foreign exchange gains due to currency fluctuations, valuation gains on financial assets, or a one-time gain from the sale of an asset. While a major positive, investors must determine if this is a sustainable, structural improvement or a non-recurring event before factoring it into long-term valuations.

“While the net profit surge provides a powerful short-term catalyst, long-term value will be dictated by Dongwon’s ability to manage operational costs and successfully execute on its new growth initiatives, particularly in the 2nd battery materials space.”

Strategic Outlook & Investor Action Plan

Given the mixed results, investors should adopt a nuanced approach. The short-term reaction may be positive, but long-term success hinges on several key factors. A look back at our previous quarter’s analysis can provide additional context on these ongoing trends.

Key Factors to Monitor Moving Forward:

- •Profitability Management: Can the company implement effective cost-efficiency measures to restore and grow its operating profit margin?

- •New Growth Engines: Progress in the high-potential 2nd battery materials business is critical. Investors should look for tangible milestones and market penetration.

- •Macroeconomic Headwinds: The impact of exchange rates, interest rates, and global commodity prices on Dongwon’s diverse portfolio remains a key risk.

- •Synergy Across Segments: How effectively can the holding company structure maximize synergy between its fisheries, food, logistics, and packaging units to create a competitive advantage?

Key Questions Answered

How did Dongwon Industries’ Q3 2025 revenue perform?

Revenue was KRW 2,586.5 billion, exceeding market expectations by 4.0%. This indicates robust underlying demand for its products and services, particularly in the food and logistics sectors.

What are Dongwon’s most promising growth drivers?

Beyond its stable food business, Dongwon is strategically investing in future growth engines. The most notable are its entry into the 2nd battery materials business via its packaging segment and the continued high-growth potential of its logistics segment, which benefits from the expanding cold chain and e-commerce markets.

What are the main risks for Dongwon Industries stock?

Investors should remain cautious of several key risks: ongoing volatility in raw material prices and currency exchange rates, the potential for rising interest rates to increase borrowing costs, and intensifying competition across its core business segments. A thorough Dongwon Industries analysis requires constant monitoring of these external factors.

Disclaimer: This article is for informational purposes only and is based on publicly available data. It does not constitute investment advice. The ultimate responsibility for investment decisions rests with the individual investor.