The investment community is buzzing with speculation surrounding the potential Hanwha Galleria Five Guys sale, a move that could significantly alter the trajectory of HANWHA GALLERIA CORPORATION (452260). With the company’s core department store business facing significant challenges, its F&B division, led by the popular American burger chain Five Guys, has emerged as a critical driver of growth. This detailed analysis explores the rumors, dissects the company’s recent financial performance, and provides a strategic outlook for investors navigating this period of uncertainty.

The Core Issue: The Hanwha Galleria Five Guys Sale Rumor

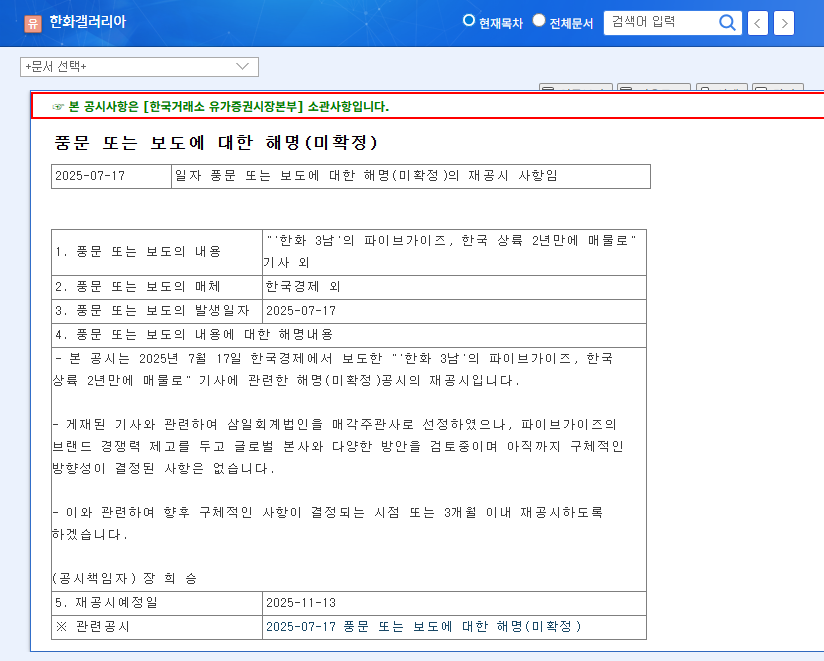

The situation escalated when reports surfaced on July 17, 2025, suggesting that the Five Guys Korea franchise, managed by ‘Hanwha’s third son’, was on the market. In response, Hanwha Galleria issued a clarification disclosure to quell the speculation. The company’s official stance, re-disclosed on November 13, 2025, remains deliberately ambiguous.

Hanwha Galleria is ‘reviewing various options with its global headquarters to enhance brand competitiveness, but no specific direction has been decided.’

This statement, available in the company’s Official Disclosure (Source: DART), indicates that while a sale is not confirmed, it is a tangible possibility. With a commitment to re-disclose by May 12, 2026, investors are left in a state of suspense, waiting for a clear strategic direction.

A Look Under the Hood: Hanwha Galleria’s Q3 2025 Financial Health

To understand why the Hanwha Galleria Five Guys sale is even being considered, one must look at the company’s challenging financial landscape. The Q3 2025 results paint a picture of a company struggling in its primary market while being propped up by a newer, more dynamic business segment.

Key Performance Indicators (Jan 1 – Sep 30, 2025)

- •Consolidated Revenue: 381.7 billion KRW, a slight decrease year-over-year, primarily due to the department store segment’s underperformance (331.1 billion KRW).

- •F&B Segment Growth: The Food & Beverage division was the sole bright spot, growing to 79.7 billion KRW, fueled by the aggressive expansion of Five Guys stores and a robust ice cream business.

- •Operating Profit Collapse: A dramatic drop to just 320 million KRW from 3.12 billion KRW in the previous year, crushed by rising administrative expenses and financial costs.

- •Widening Net Loss: The company’s net loss expanded to a concerning 21.7 billion KRW.

- •Rising Debt: The debt-to-equity ratio climbed to 144.26%, signaling increasing financial leverage and risk.

Macroeconomic Headwinds

The company’s struggles are compounded by a difficult macroeconomic environment. Volatile exchange rates (USD/KRW ~1,321) negatively affect the cost of imported goods for both its retail and F&B segments. Furthermore, elevated interest rates, though frozen in South Korea, increase borrowing costs and dampen consumer sentiment, which is critical for a luxury retailer. These external pressures, as noted in many global economic outlooks, create a challenging operational climate.

Strategic Crossroads: The Impact of a Potential Five Guys Sale

Divesting the Five Guys brand presents both significant opportunities and substantial risks for HANWHA GALLERIA CORPORATION.

The Upside: Potential for Financial Rejuvenation

A successful sale could provide a much-needed cash infusion. These proceeds could be strategically deployed to pay down debt, immediately improving the company’s debt-to-equity ratio and strengthening its balance sheet. This would not only enhance financial stability but also free up capital for reinvestment into revitalizing the core department store business or acquiring a new, more synergistic growth engine. It represents a chance to reset and refocus.

The Downside: Losing the Growth Champion

The most significant risk is the loss of its only proven growth driver. Selling Five Guys would leave the struggling department store segment exposed, amplifying concerns about the company’s future growth prospects. Moreover, such a move could damage investor confidence, suggesting a lack of a coherent long-term strategy and potentially harming the company’s corporate image. If the sale falls through or is executed on unfavorable terms, it could leave the company in an even weaker position.

Investor Playbook: Navigating the Uncertainty with 452260 Stock

Given the high degree of uncertainty, a cautious and watchful approach is warranted. The stock’s future trajectory hinges entirely on the outcome of the Hanwha Galleria Five Guys sale discussions.

Investment Thesis and Key Monitoring Points

At present, a ‘Hold’ or ‘Neutral’ recommendation is most prudent. Short-term volatility is highly likely as rumors ebb and flow. The long-term outlook depends on management’s execution. Investors should closely monitor the following:

- •Official Communications: The next official disclosure by May 12, 2026, is a critical catalyst. Any preceding announcements will be heavily scrutinized by the market.

- •Core Business Performance: Watch for any signs of a turnaround in the department store segment. Improved sales or margins would reduce the company’s reliance on a potential asset sale, as we’ve discussed in our broader analysis of the retail sector.

- •Macroeconomic Shifts: Keep an eye on interest rate policies and currency fluctuations, as these will continue to impact profitability and consumer behavior.

Disclaimer: This analysis is for informational purposes only and is based on publicly available data. All investment decisions carry risk and should be made at the investor’s own discretion. Market conditions can change rapidly, and continuous monitoring is essential.