The upcoming T. K. CORPORATION IR (Investor Relations) conference on November 17, 2025, is poised to be a pivotal moment for investors. As a global leader in plant fittings, T. K. CORPORATION is navigating a complex landscape, balancing its robust core operations against recent performance declines and the crucial task of scaling its new growth engine: the secondary battery business. This comprehensive T. K. CORPORATION stock analysis will dissect the company’s financial health, competitive advantages, and the immense potential of its subsidiary, HYTC, providing you with the critical insights needed to make an informed investment decision. The information presented is based on public data, including the company’s Official Disclosure.

Event Overview: What to Expect from the T. K. CORPORATION IR

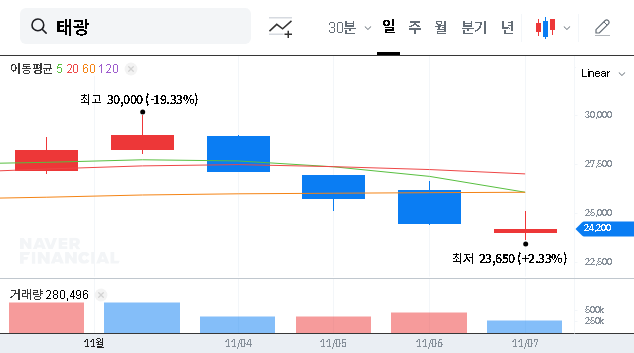

Scheduled for 9:00 AM on November 17, 2025, this IR event is more than a routine update. With a market capitalization of KRW 658.5 billion, the company aims to transparently communicate its performance and strategic direction. Given the current lack of specific brokerage reports, this conference represents a significant opportunity for management to shape the market narrative and investor expectations directly.

This IR is a critical juncture. Investors will be keenly listening for a clear roadmap on how T. K. CORPORATION plans to enhance profitability in its secondary battery segment while reinforcing the stability of its core business.

Analyzing the Dual Engines of Growth

The Bedrock: Dominance in the Plant Fitting Market

T. K. CORPORATION’s primary business is the manufacture and sale of plant fittings—essential components for national key industries like energy and petrochemicals. This foundation provides a stable, recurring revenue stream built on decades of expertise and a formidable market position.

- •Oligopolistic Market: The company operates within a global oligopoly, characterized by high technological barriers to entry, which insulates it from excessive competition.

- •Export Powerhouse: With exports making up 83.1% of its 2024 revenue, the company boasts a global market share of 58.34%, far surpassing domestic rivals and providing a natural hedge against raw material cost fluctuations. For more details, you can read our analysis of the global plant equipment market.

- •Financial Resilience: A high proportion of exports allows the company to effectively manage exchange rate risks and navigate volatile raw material prices.

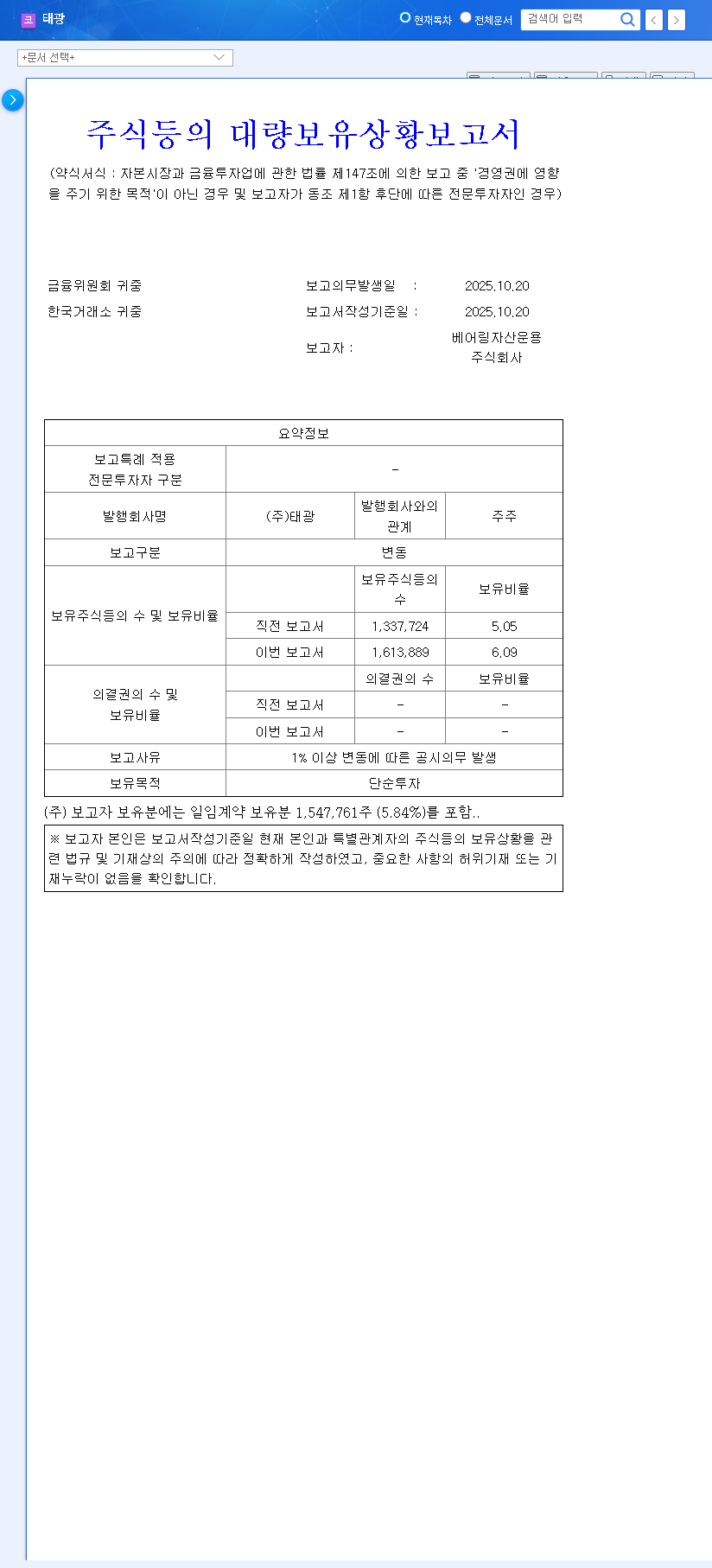

The Future: HYTC and the Secondary Battery Boom

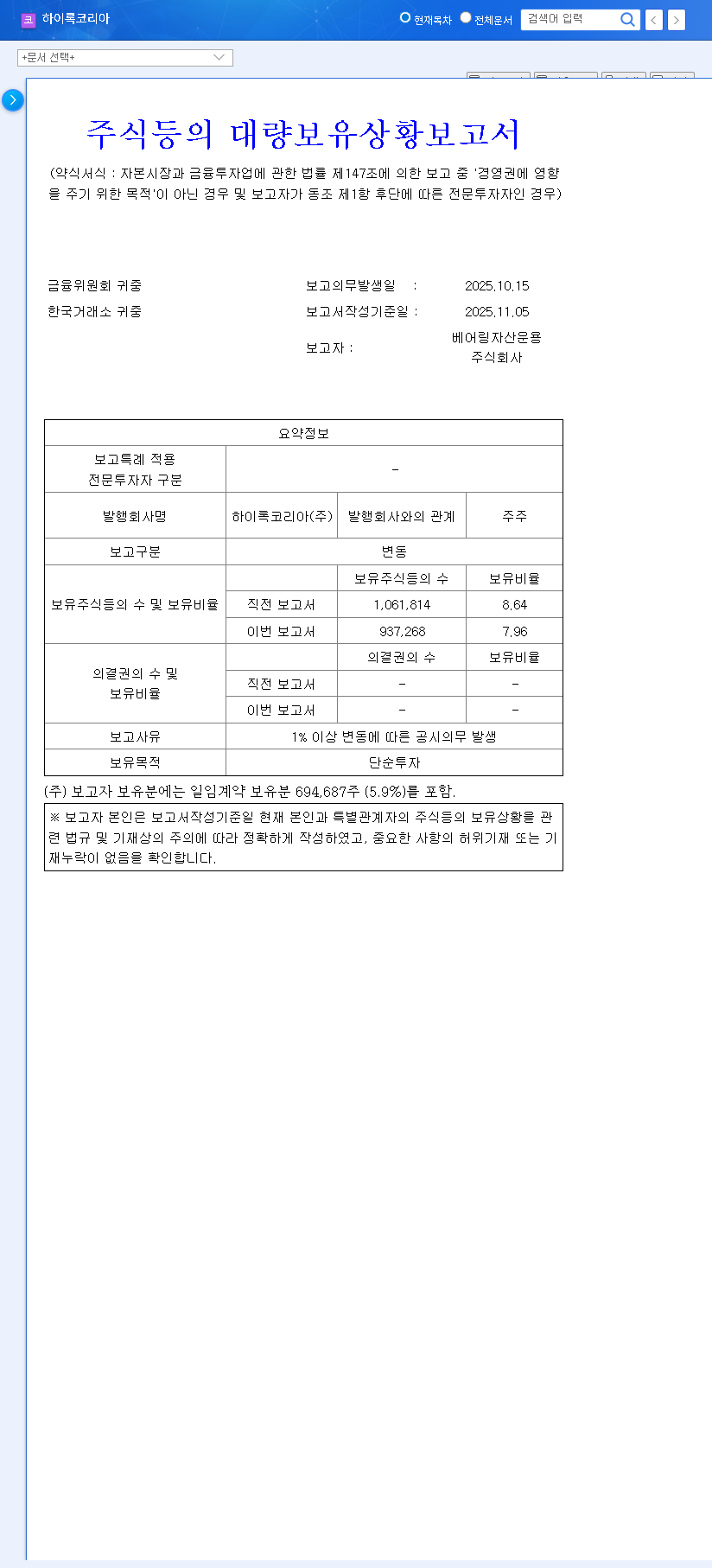

The most anticipated part of the T. K. CORPORATION IR will be the update on its KOSDAQ-listed subsidiary, ‘HYTC’. This venture, focused on secondary battery equipment parts and Slitter manufacturing, is the company’s bet on the future of energy.

The HYTC secondary battery business is positioned in a market with explosive growth potential, driven by the global transition to electric vehicles (EVs) and energy storage systems (ESS). According to authoritative industry reports, this sector is projected to grow exponentially over the next decade. However, this potential comes with challenges. HYTC recorded an operating loss in H1 2025, highlighting the urgent need for a clear strategy to improve profitability. Investors will be looking for concrete plans on technology development, customer acquisition, and cost management to turn this growth engine into a profitable one.

Financial Health and Investor Value

Despite recent performance dips, T. K. CORPORATION’s financial foundation remains exceptionally strong. As of H1 2025, its debt-to-equity ratio stood at a mere 9.07%, signaling remarkable financial stability and low risk. This robust balance sheet provides the company with the flexibility to invest in growth areas like HYTC without taking on undue leverage. Furthermore, the company maintains a shareholder-friendly policy, with a history of consistent dividend payments, offering a degree of stability for income-focused investors.

Investment Outlook & Action Plan

Our current investment opinion is Neutral, pending the outcomes of the IR. The company presents a compelling blend of a stable, cash-generating core business and a high-growth venture. However, the uncertainties surrounding the profitability of the secondary battery segment and broader macroeconomic headwinds (e.g., interest rates) warrant a cautious approach.

Key Points for Investors to Monitor Post-IR:

- •HYTC’s Profitability Roadmap: Look for specific, measurable plans and timelines for achieving profitability in the secondary battery division.

- •Core Business Order Book: Assess management’s outlook on order trends and the recovery timeline for the plant fitting business.

- •Capital Allocation Strategy: Understand the company’s plans for future investments, R&D spending, and potential fundraising.

- •Macroeconomic Impact Management: Evaluate the strategies in place to mitigate risks from fluctuating exchange rates and interest rates.

In conclusion, the T. K. CORPORATION IR is a must-watch event. A compelling presentation of a clear growth strategy and financial outlook could provide significant positive momentum for the stock. Conversely, a failure to address key concerns could deepen investor uncertainty. Careful analysis of the information presented will be paramount to determining the true investment value of T. K. CORPORATION.