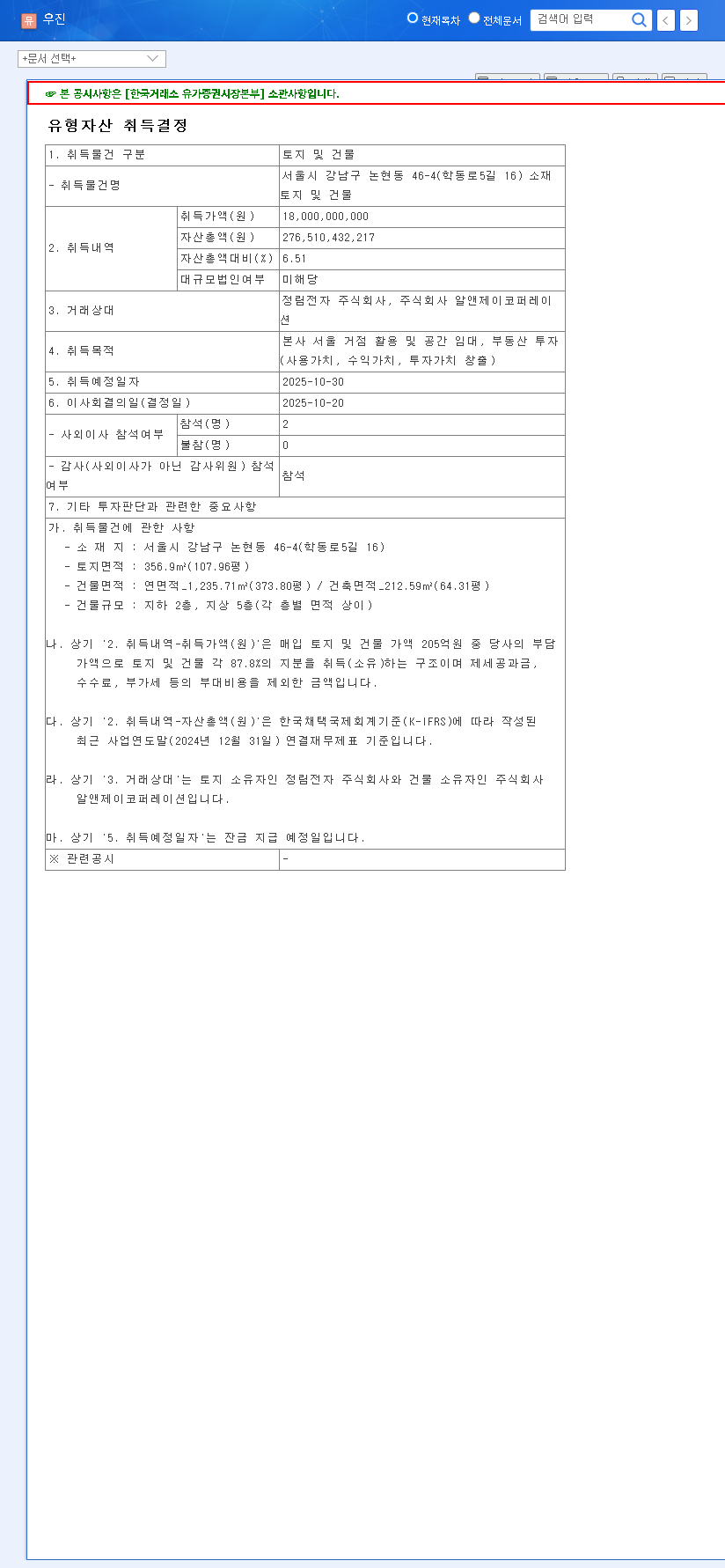

An in-depth analysis of the WOOJIN INC stock profile reveals a significant positive catalyst following the announcement of a landmark ₩10.3 billion contract. Amid a global resurgence in nuclear energy, WOOJIN INC, a distinguished leader in nuclear instrumentation, has solidified its market leadership by securing this pivotal agreement with Korea Hydro & Nuclear Power (KHNP). This contract is more than a financial transaction; it’s a powerful indicator of the company’s stable growth trajectory and its integral role in the burgeoning nuclear sector. This analysis will dissect the contract’s details, its immediate financial implications, and the long-term outlook for investors considering WOOJIN INC stock.

Contract Breakdown: The ₩10.3 Billion KHNP Deal

WOOJIN INC has formally secured a ₩10.3 billion contract with Korea Hydro & Nuclear Power (KHNP) for the ‘2nd Procurement of In-Core Instrumentation (ICI) for the 2026 Standard Nuclear Power Plant Overhaul (O/H)’. This substantial agreement represents a significant portion of the company’s projected revenue, highlighting the deep trust and established relationship with South Korea’s primary nuclear operator. The details of this agreement were confirmed in an Official Disclosure on the DART system.

- •Counterparty: Korea Hydro & Nuclear Power (KHNP)

- •Contract Value: ₩10.3 Billion KRW

- •Subject: In-Core Instrumentation (ICI) for nuclear plant maintenance.

- •Contract Period: Nov 2025 – Nov 2026

- •Revenue Impact: Represents ~7.3% of 2024’s revenue.

Why This WOOJIN INC Contract Matters Strategically

This deal reinforces WOOJIN’s indispensable position within the nuclear supply chain. In-Core Instrumentation is not a simple commodity; it is the central nervous system of a nuclear reactor, providing critical data for safe and efficient operation. WOOJIN’s exclusive domestic supply status for ICI gives it a powerful economic moat, insulating it from direct competition and ensuring a consistent stream of high-margin orders from KHNP’s fleet of reactors.

This contract is a clear affirmation of WOOJIN’s technical excellence and its crucial role in maintaining the safety and reliability of South Korea’s nuclear infrastructure. For investors, it signals predictable revenue and a fortified market position.

This recurring revenue from maintenance and overhaul cycles provides a stable foundation, allowing the company to invest in other high-growth areas. The consistent demand for nuclear instrumentation is a core pillar of the investment thesis for WOOJIN INC stock.

Analyzing the Impact on WOOJIN INC Stock

The direct financial impact and the subsequent effect on stock valuation can be viewed from both short-term and long-term perspectives.

Short-Term Financial Health & Momentum

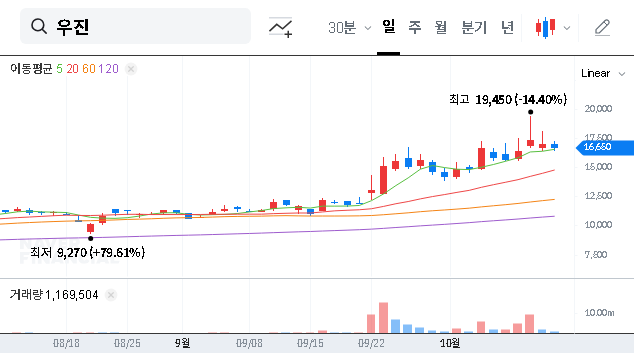

The ₩10.3 billion in revenue will be recognized primarily in late 2025 and early 2026, providing a significant boost to revenue and operating profit during that period. This predictable inflow improves the company’s cash flow and helps offset potential sluggishness in other business segments. For the stock, this news serves as a powerful short-term catalyst, enhancing investor confidence and potentially driving positive momentum, especially as it signals a recovery and stabilization in its core nuclear business.

Long-Term Valuation & Growth Prospects

From a long-term perspective, this WOOJIN INC contract reinforces the company’s fundamental value. With a stable debt-to-equity ratio and a Price-to-Book (PBR) of approximately 0.54, many analysts argue that WOOJIN INC stock is undervalued relative to its tangible assets and market position. This solid foundation is crucial as the company and the industry enter a new growth phase driven by global trends. The global push for carbon-neutral energy sources places nuclear power back in the spotlight. This includes the development of Small Modular Reactors (SMRs), a market where WOOJIN is well-positioned to become a key supplier. To learn more about this technology, you can visit the International Atomic Energy Agency (IAEA). The company’s future stock appreciation will likely be tied to its ability to capture this new market while maintaining its core business, as detailed in our complete analysis of the Korean energy sector.

Investor Outlook: Thesis and Risks

The overall investment rating for WOOJIN is positive, grounded in its market dominance and the favorable industry outlook. However, a balanced view requires considering potential risks.

- •Bull Case: Stable, recurring revenue from its core ICI business, combined with significant long-term growth potential from the SMR market and international expansion. Undervalued fundamentals present an attractive entry point.

- •Bear Case: Potential risks include sluggish performance in non-nuclear divisions, uncertainty in the timeline and profitability of new ventures like its Smart Factory business, and macroeconomic pressures on raw material costs.

Frequently Asked Questions

What kind of company is WOOJIN INC?

WOOJIN INC is a specialized industrial company that supplies critical components and systems for the nuclear power, plant engineering, and industrial instrumentation sectors. It holds an exclusive supply position in the South Korean market for In-Core Instrumentation (ICI).

How will this contract impact WOOJIN’s revenue?

The ₩10.3 billion contract value is expected to be recognized over 2025-2026, directly boosting top-line revenue and operating profit while strengthening the company’s financial stability.

What is the expected impact on the WOOJIN INC stock price?

In the short term, this positive news could improve investor sentiment and drive stock momentum. In the long term, it reinforces the fundamental valuation of WOOJIN INC stock and supports a positive outlook tied to the broader growth of the nuclear industry.

In conclusion, the KHNP contract is a cornerstone event for WOOJIN INC, offering investors a clear and compelling reason to re-evaluate the company’s future value. It highlights a stable, profitable core business that is perfectly positioned to capitalize on the next wave of nuclear energy development.