The financial markets are closely watching the potential Hanwha Investment & Securities Dunamu stake sale, a development with significant implications for both companies and the broader fintech landscape. Hanwha Investment & Securities Co., Ltd. has confirmed it is reviewing options for its 5.94% stake in Dunamu, the operator of South Korea’s largest cryptocurrency exchange, Upbit. This deep-dive analysis unpacks the company’s strong fundamentals, the strategic rationale behind the review, and what this pivotal event could mean for investors.

This move is prompted by ongoing strategic alliance discussions between Dunamu and Naver Financial, a major player in the digital finance space. While nothing is finalized, the potential outcomes—ranging from a full sale to holding the stake—create a mix of opportunities and risks that savvy investors must understand.

Official Stance and Market Context

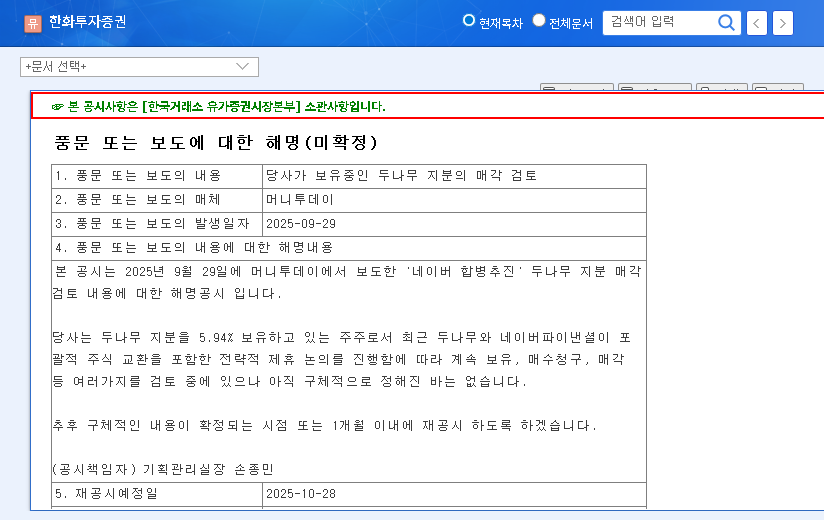

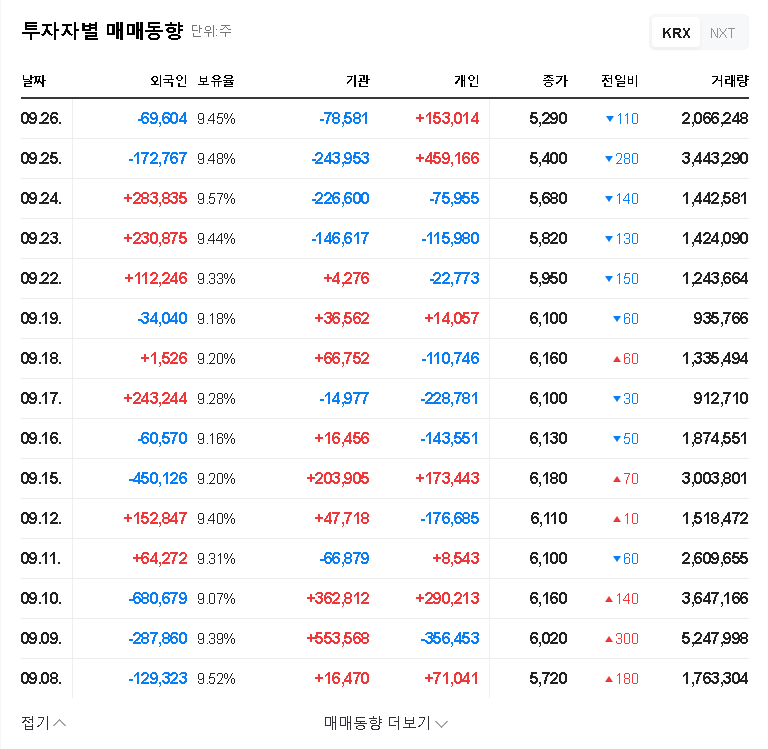

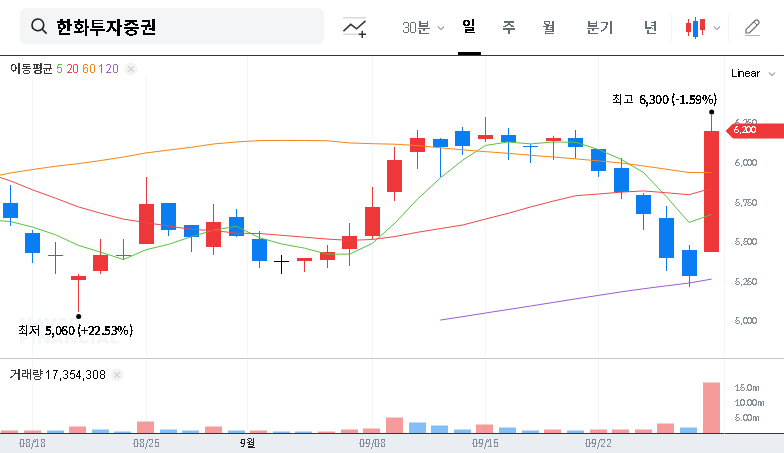

In response to market speculation, Hanwha Investment & Securities issued a formal clarification. The company stated that as a key shareholder, it is “reviewing various options” for its Dunamu holdings. This was confirmed through an official public disclosure, which investors can review for full transparency. (Source: Official DART Disclosure). It’s crucial to note that no definitive decision has been made, with a re-disclosure date set for January 23, 2026. This extended timeline indicates a careful, strategic evaluation process rather than a hasty liquidation.

The review of the Dunamu stake is a pivotal moment for Hanwha Investment & Securities. It’s not just about realizing gains; it’s about strategically positioning the company for its next phase of growth amidst a rapidly evolving financial technology sector.

Deep Dive: Hanwha’s Financial Health (H1 2025)

Before analyzing the stake sale’s impact, understanding Hanwha’s current financial standing is essential. The company has demonstrated remarkable resilience and growth, even within a complex macroeconomic environment. For more context on global market conditions, investors often consult authoritative sources like Reuters’ global financial analysis.

Robust Performance and Profitability

In the first half of 2025, Hanwha’s consolidated total assets grew to KRW 14.7 trillion, with total equity reaching KRW 1.78 trillion. The company posted an operating profit of KRW 84.9 billion and a net profit of KRW 66.5 billion, both significant year-over-year increases. A key driver of this success was an impressive KRW 892.1 billion in derivatives-related profit, showcasing the firm’s sophisticated trading capabilities.

Financial Soundness and Global Expansion

Hanwha’s financial stability is impeccable. It maintains strong credit ratings (A1 short-term, AA- long-term) and boasts an exceptional Net Capital Ratio (NCR) of 743%. This high NCR indicates a substantial buffer against financial risks, far exceeding regulatory requirements. Furthermore, its global footprint is expanding, with profitable subsidiaries in Vietnam and Indonesia strengthening its presence in the high-growth Southeast Asian market. For those interested, you can read our deep dive into the Korean securities market for more context.

Implications of the Hanwha Investment & Securities Dunamu Stake Sale

The decision regarding the Dunamu stake carries a mix of potential benefits and risks that could significantly alter the company’s trajectory and Hanwha Investment valuation.

- •Positive – Capital Injection: A successful sale at a favorable valuation would unlock substantial capital. This cash infusion could be used to deleverage, invest in core business segments like Wealth Management and Investment Banking, or fund further global expansion.

- •Positive – Value Realization: The potential Naver-Dunamu alliance could dramatically increase Dunamu’s valuation. Selling into this strength would allow Hanwha to realize significant gains on its initial investment, directly boosting shareholder value.

- •Risk – Market Uncertainty: As the decision is not yet final, the ambiguity can create short-term volatility in Hanwha’s stock price. The market dislikes uncertainty, and this will be a key overhang until a final decision is announced.

- •Risk – Opportunity Cost: If Hanwha sells and Dunamu’s value subsequently skyrockets due to the growth of Upbit stock value and new ventures in Web3 or NFTs, Hanwha would miss out on substantial future upside. This represents a significant opportunity cost.

Investment Outlook and Final Recommendation

Given the robust fundamentals of Hanwha Investment & Securities and the unresolved nature of the Dunamu stake sale, a ‘Neutral’ investment recommendation is appropriate at this time. The company’s core business is performing exceptionally well, providing a solid foundation. However, the uncertainty surrounding the Dunamu stake introduces a variable that warrants caution.

Investors should closely monitor three key areas: first, any official announcements regarding the stake sale; second, the progress and details of the Naver-Dunamu alliance; and third, Hanwha’s ongoing quarterly performance in its core segments. A positive resolution on the sale, coupled with a clear strategy for capital deployment, could serve as a powerful catalyst for the stock. Conversely, a prolonged period of indecision could weigh on investor sentiment.