A critical challenge has emerged for Lotte Non-Life Insurance Co., Ltd., placing the company under intense market and regulatory scrutiny. The insurer has taken the significant step of filing an injunction and a lawsuit against a ‘management improvement recommendation’ issued by financial authorities. This is not merely a legal procedural matter; it is a pivotal event that could redefine the financial trajectory, market credibility, and strategic direction of Lotte Non-Life Insurance. This comprehensive analysis will dissect the situation, exploring the underlying financial pressures, the potential fallout from this legal confrontation, and the essential factors investors must monitor closely.

The Core Conflict: Regulatory Action and a Bold Legal Response

On November 11, 2025, Lotte Non-Life Insurance escalated its dispute with regulators by challenging the ‘management improvement recommendation’ in court. This recommendation is a formal action taken by financial authorities when an insurer’s financial health, particularly its capital adequacy, falls below required thresholds. The company’s legal filing, as documented in the Official Disclosure (DART), signals a direct challenge to the regulator’s assessment and an attempt to prevent potential operational restrictions. This proactive, albeit confrontational, stance has created significant uncertainty and raised the stakes for the company’s management and its investors.

A Deeper Look at Lotte Non-Life Insurance’s Financials

The company’s fundamentals present a conflicting picture of operational success overshadowed by capital adequacy concerns. Understanding both sides is crucial for a complete analysis.

Warning Signs: The Declining K-ICS Ratio

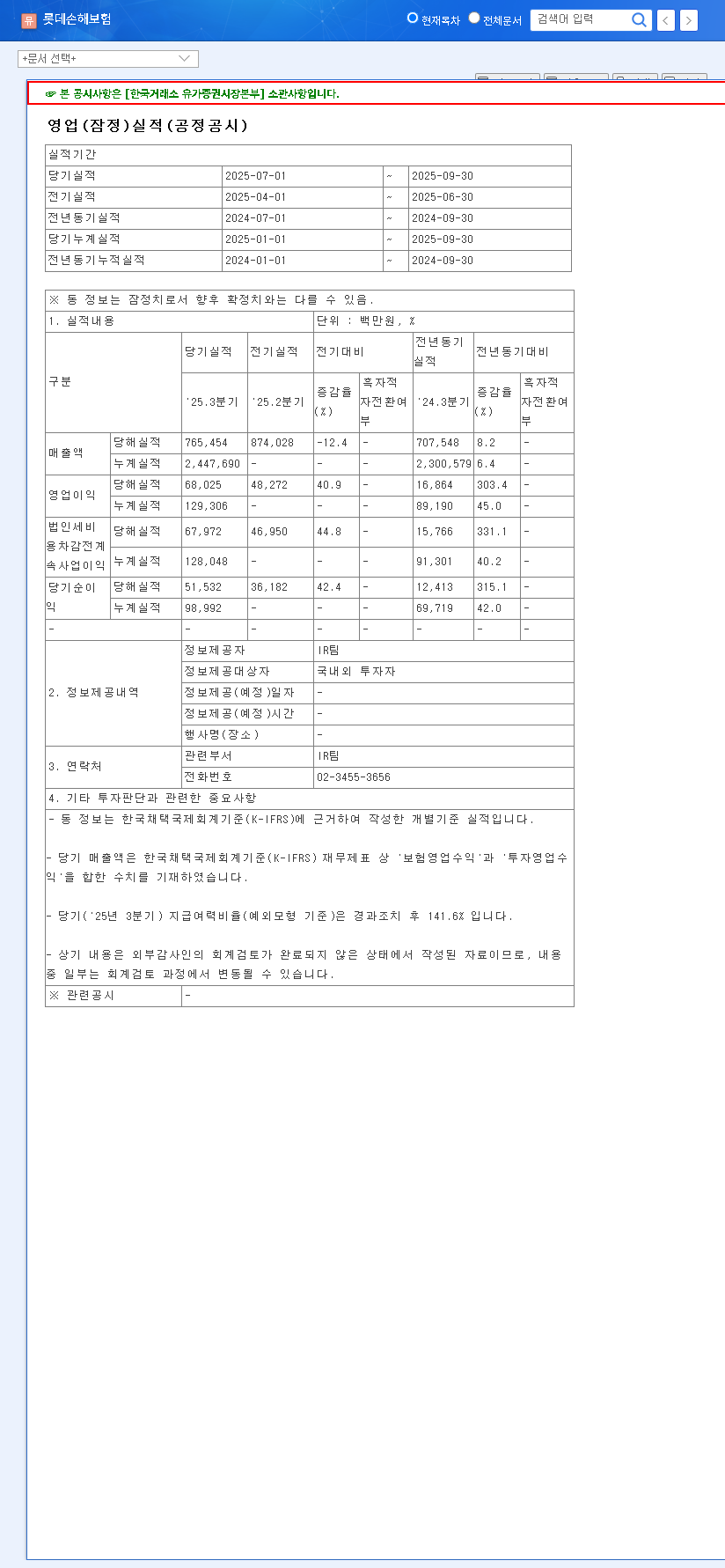

The primary catalyst for the regulatory action is the company’s deteriorating solvency ratio under the Korean Insurance Capital Standard (K-ICS). This metric is a key indicator of an insurer’s ability to withstand financial shocks and meet its obligations to policyholders.

The sharp decline in the K-ICS ratio to 129.46% is a major red flag. Regulators typically expect a ratio of at least 150%, making the need for significant capital replenishment an urgent priority for Lotte Non-Life Insurance.

- •K-ICS Ratio Plunge: The interim report for H1 2025 confirmed a ratio of 129.46%, a steep fall from 154.59% the previous year and 213.20% two years prior.

- •Credit Outlook Downgrade: Reflecting these concerns, the company’s insurance payment capacity rating outlook was revised from ‘Stable’ to ‘Negative’, even while maintaining its ‘A’ grade.

For a deeper understanding of these metrics, investors can review our guide on Understanding the K-ICS Standard for Insurers.

Positive Signals: Profitability and Growth

Despite the capital concerns, the company’s core business operations show resilience and growth.

- •Turnaround to Profit: Lotte Non-Life Insurance reported a net profit of KRW 47.5 billion, a marked improvement from the KRW 24.2 billion profit in the same period last year, thanks to better investment income and premium growth.

- •Sustained Premium Growth: Gross written premiums grew a healthy 5% to KRW 1.4216 trillion, driven primarily by its strategic focus on the long-term insurance market.

Market Environment and Strategic Challenges

Lotte Non-Life Insurance does not operate in a vacuum. It faces intense competition in the South Korean market, with over 30 players vying for market share. Furthermore, macroeconomic volatility, including shifting interest rates and currency fluctuations, presents both opportunities and risks for its investment portfolio. In this environment, the company’s push towards digital transformation with platforms like ALICE and Wonder is a critical initiative to enhance efficiency and competitiveness. The current legal dispute, however, could divert crucial management attention and resources away from these strategic goals. Global economic trends, as reported by sources like Bloomberg, continue to add layers of complexity to the operating environment for all insurers.

Investor Outlook: Key Recommendations

The legal action introduces significant risk. While a successful lawsuit could be a major victory, a loss could result in stricter sanctions and further damage to its reputation. The market will be closely watching how Lotte Non-Life Insurance navigates this period. The company’s future value hinges on its ability to execute a multi-pronged strategy:

- •Execute a Capital Plan: The most pressing issue is the K-ICS ratio. The company must urgently formulate and execute a clear plan to raise capital and restore its solvency ratio to a stable level above 150%.

- •Communicate Transparently: To mitigate market uncertainty, proactive and transparent communication with investors regarding the lawsuit and its capital strategy is non-negotiable.

- •Strengthen Core Business: The company must not lose sight of its operational strengths. Continuing to grow its profitable long-term insurance portfolio and advancing its digital innovation are key to long-term value creation.

In conclusion, while the operational performance of Lotte Non-Life Insurance shows promise, it is currently overshadowed by a critical solvency issue and a high-risk legal battle with its regulator. The company’s ability to resolve its capital deficiency and manage the outcome of the lawsuit will be the ultimate determinant of its future success and stock performance.