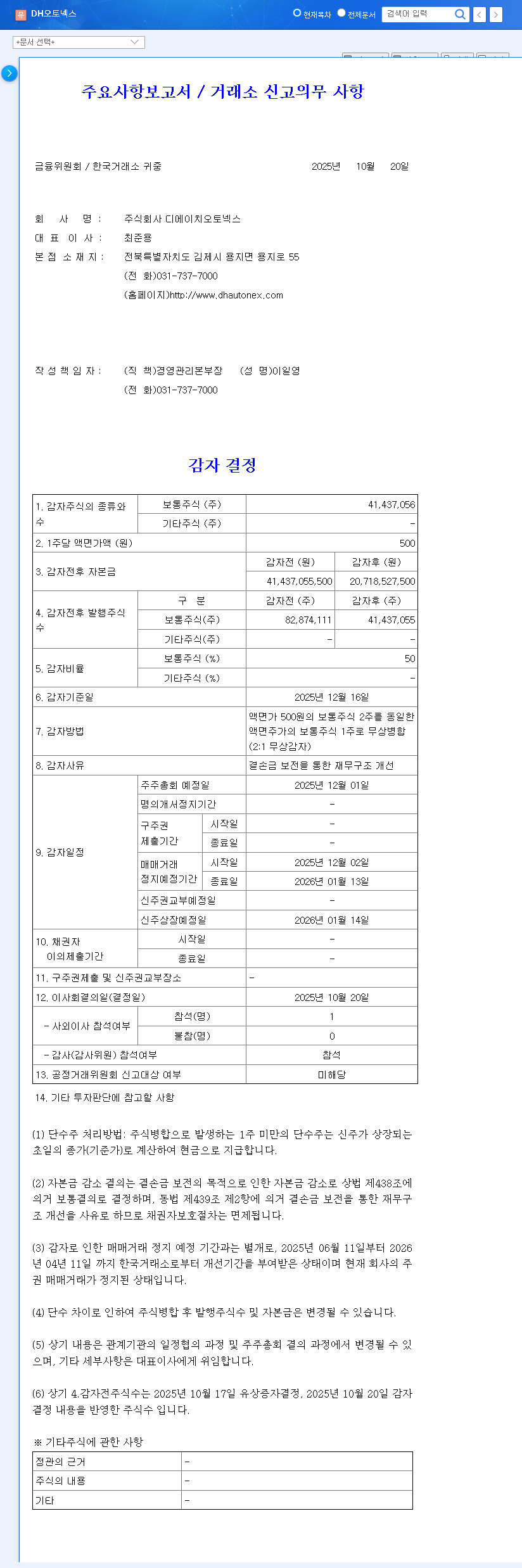

The recent announcement of the DHAUTONEX capital reduction has raised significant questions among investors. On October 20, 2025, DHAUTONEX CO.,LTD (DH오토넥스) declared a 50% capital reduction via a reverse stock split, a strategic move aimed at improving its financial health. While this can be a positive step for the company’s balance sheet, it often introduces short-term stock price volatility and uncertainty for shareholders.

This comprehensive guide provides a detailed analysis from a financial expert’s perspective. We will dissect the reasons behind this decision, break down the potential impact on the company’s stock price, and offer a clear action plan for investors. Our goal is to equip you with the knowledge to navigate this corporate event and make informed decisions about your portfolio.

📈 Understanding the DHAUTONEX Capital Reduction

DHAUTONEX officially announced a 50% capital reduction of its common shares. This is being executed as a 2-for-1 reverse stock split, which means every two existing shares will be consolidated into a single new share. This action will reduce the total number of outstanding shares from 82,874,112 to 41,437,056. The company has made this information public through its official channels.

For complete details and verification, investors should always refer to the primary source. You can view the Official Disclosure on DART, South Korea’s electronic disclosure system.

Key Schedule for the Reverse Stock Split

- •Announcement Date: October 20, 2025

- •Shareholder Meeting: December 1, 2025

- •Stock Trading Suspension: December 2, 2025

- •Record Date for New Shares: December 16, 2025

- •Stock Trading Resumption: January 14, 2026

📉 The Core Reason: Improving Financial Structure

The primary motivation behind any corporate capital reduction, including the DHAUTONEX capital reduction, is almost always related to the company’s financial health. In this case, the stated purpose is explicitly to address past financial difficulties.

The official reason cited by DHAUTONEX is to ‘improve the financial structure by compensating for accumulated deficits.’ This indicates the company has carried significant losses on its books, which can lead to capital impairment and deter future investment.

By reducing the capital account, the company can write off these accumulated deficits, effectively cleaning up its balance sheet. A cleaner financial statement can restore investor confidence, make it easier to raise new capital, and provide a more stable foundation for future operations. It’s a financial reset designed to pave the way for long-term recovery and growth.

📊 Impact Analysis: Stock Price, Financials, and Investors

A capital reduction creates ripple effects across the company. Here’s a breakdown of the key impacts investors need to understand.

1. Financial Impact

- •Cleaner Balance Sheet: The primary goal—offsetting deficits—will be achieved, improving key financial ratios and overall soundness.

- •Potential for Higher EPS: With fewer shares outstanding, future profits will be divided among a smaller number of shares, which can lead to a higher Earnings Per Share (EPS), a key metric for investors.

- •No Change in Equity: Importantly, this is a ‘paper’ transaction. It shuffles numbers between capital and deficit accounts but does not change the company’s total shareholder equity or intrinsic value.

2. Stock Price Impact

- •Price Readjustment: When trading resumes, the stock price will theoretically double to reflect the 2-for-1 consolidation. For example, two shares at 2,000 KRW each become one share at 4,000 KRW.

- •Short-Term Volatility: Markets often react with uncertainty. Expect increased price swings around the trading suspension and resumption dates as investors digest the news.

- •Long-Term Performance: The ultimate trajectory of the stock price depends entirely on the company’s future performance. A cleaner balance sheet is just the first step; DHAUTONEX must follow through with improved sales and profitability.

3. Investor Impact

- •Reduced Share Count: Your number of shares will be halved. If you held 100 shares, you will own 50 post-split.

- •Constant Portfolio Value: Because the share price adjusts upwards, the total value of your holding should, in theory, remain the same at the moment of the split.

- •Need for Vigilance: Given the lack of detailed brokerage reports, investors must be proactive in monitoring company announcements and market sentiment.

💡 Investor Action Plan & Key Monitoring Points

This capital reduction is not a signal to buy or sell but a critical moment to re-evaluate. Prudent investors should focus on the company’s next steps. For more general guidance, you can read our article on How to Analyze a Company’s Financial Health.

Here are the key points to monitor:

- •Shareholder Meeting Outcome: Confirm the final approval of the plan on December 1, 2025.

- •Post-Split Financial Reports: Scrutinize the first few quarterly reports after the reduction to see tangible improvements on the balance sheet and income statement.

- •Future Business Strategy: Look for clear communication from management about how they will leverage the improved financial structure to drive growth.

- •Market and Analyst Commentary: Follow expert analyses and market sentiment as they develop post-resumption of trading.

✅ Conclusion: A New Beginning, Not a Guaranteed Win

The DHAUTONEX capital reduction is a significant and necessary step to repair its financial foundation. However, it is crucial for investors to understand that this action alone does not improve the company’s underlying business operations, competitiveness, or profitability. It simply provides a cleaner slate.

The real test begins now. The focus should shift from this financial event to the company’s ability to execute a successful business strategy moving forward. Careful and continuous monitoring will be the key to making wise investment decisions regarding DHAUTONEX.

Frequently Asked Questions (FAQ)

Q1: What is a capital reduction and why is DHAUTONEX doing it?

A capital reduction (specifically a gratuitous reduction or ‘무상감자’) is a corporate action to decrease a company’s shareholder equity. DHAUTONEX is doing this to offset its accumulated financial losses (deficits), thereby improving its financial statements and stability.

Q2: How does this capital reduction affect the stock price?

Theoretically, the total market value of the company doesn’t change. The stock price should double to compensate for the number of shares being halved. However, in practice, short-term stock price volatility is expected. The long-term price will depend on future business performance.

Q3: What happens to my shares in DHAUTONEX?

The number of shares you hold will be cut in half. If you own 100 shares, you will have 50 after the event. The price per share will adjust upwards, so the total value of your investment should remain the same at the time of the change.

Q4: Is it safe to invest in DHAUTONEX now?

This financial maneuver is just a starting point. It does not guarantee future success. Investment decisions should be made cautiously after monitoring the company’s post-reduction performance, business plans, and actual financial improvements. The uncertainty is high, so thorough due diligence is essential.