The ongoing crisis at DKME Co., Ltd. has taken a perilous turn. Already under a trading halt and facing a delisting review for ’embezzlement/breach of trust allegations,’ the company is now embroiled in a severe DKME Co., Ltd. management dispute. A recently filed injunction application threatens to paralyze its leadership, creating unprecedented uncertainty for the company’s future and its shareholders. This comprehensive guide will dissect the legal challenge, analyze the grave implications for the DKME stock, and provide strategic advice for investors navigating this turbulent period.

The Core of the DKME Co., Ltd. Management Dispute

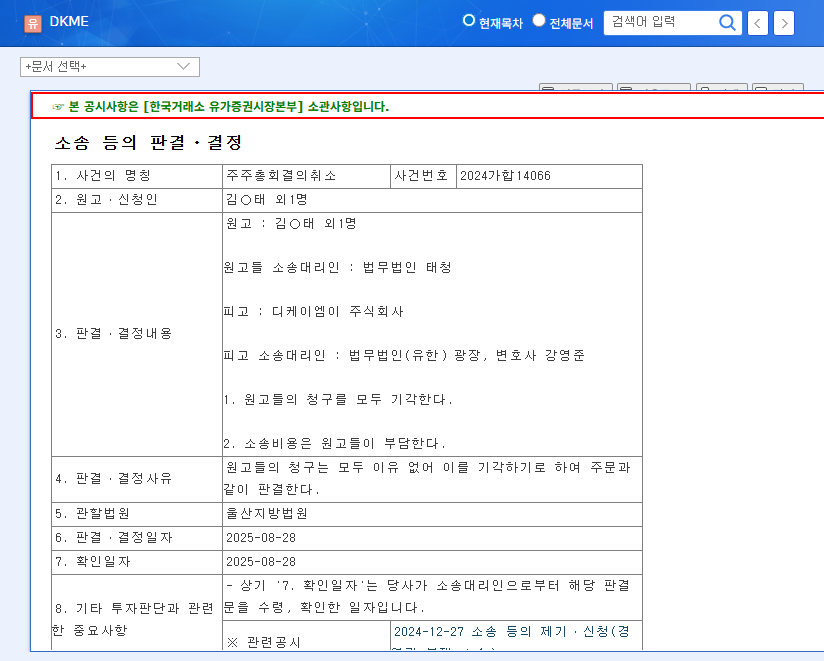

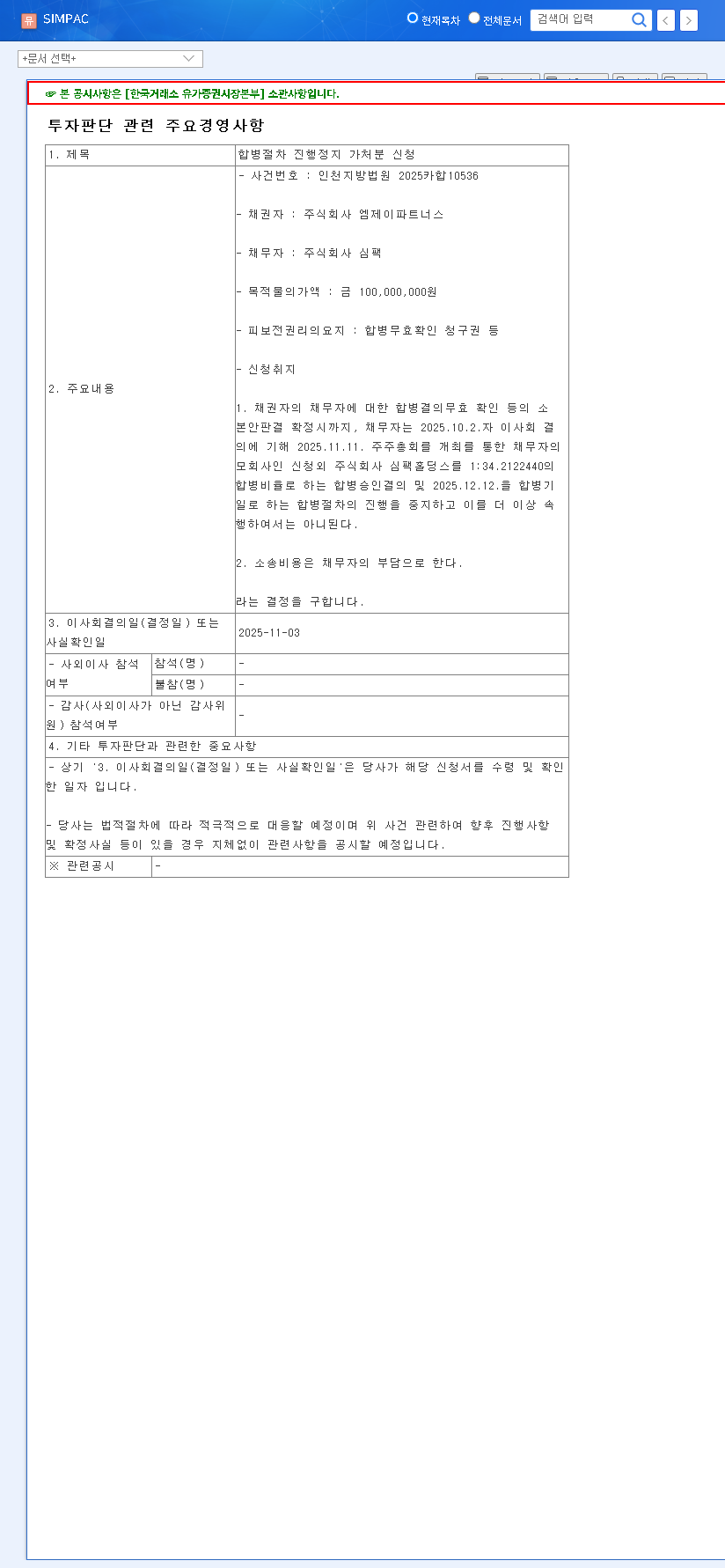

On November 13, 2025, the situation escalated with an official disclosure of a lawsuit application targeting the company’s management. The legal action, filed at the Ulsan District Court, is an injunction request that could fundamentally alter the company’s power structure. The details were confirmed via an Official Disclosure on the DART system.

Key Demands in the Injunction Filing:

- •Suspension of Executive Duties: The plaintiffs seek to immediately suspend the duties of Si OOOO, a key figure operating DKME INC. and Quantum Wealth Management LLC.

- •Return of Company Shares: A claim for the return of DKME Co., Ltd. shares currently held by DKME INC. and Quantum Wealth Management LLC.

- •Prohibition of Voting Rights: A request to prohibit the defendants from exercising their voting rights at any future General Meeting of Shareholders for DKME Co., Ltd.

Impact Analysis: A Cascade of Corporate Instability

This legal battle is far more than an internal power struggle; it represents a systemic shock to the company’s foundation. The potential outcomes could trigger a domino effect, exacerbating the already dire situation and severely impacting corporate value.

For investors, uncertainty is the greatest risk. This management dispute has injected a lethal dose of it into DKME Co., Ltd., making any prediction about its future highly speculative.

Failure of Corporate Governance

The emergence of such a profound DKME Co., Ltd. management dispute is a clear symptom of a severe breakdown in corporate governance. When leadership is contested so publicly and legally, it signals deep-rooted issues in oversight, accountability, and strategic alignment. This failure erodes trust not only among shareholders but also with suppliers, creditors, and employees, threatening the operational fabric of the company. A failure in governance can often precede financial distress, a risk that is now amplified for DKME.

Compounding the Delisting Risk

DKME is already on thin ice with its ongoing DKME delisting review. A management dispute adds another layer of complexity that regulators will scrutinize. The exchange may view the leadership vacuum and internal strife as proof that the company cannot reliably manage its affairs or protect shareholder interests. This significantly increases the probability of an unfavorable delisting decision, which would be a catastrophic outcome for existing investors. For more information, you can read our guide on Understanding the Delisting Process.

Investor Guide: Navigating the Crisis

Given the extreme volatility and existential threats, a cautious and informed approach is paramount. This is not a time for speculative bets but for disciplined risk management.

Strategic Recommendations for DKME Investors

- •Monitor Legal Proceedings Rigorously: Keep a close watch on all rulings from the Ulsan District Court. The outcome of the injunction is the most critical short-term catalyst.

- •Scrutinize Company Communications: Pay attention to every official statement from DKME Co., Ltd. The company’s response strategy—or lack thereof—will provide valuable insight into its viability.

- •Defer New Investments: With the trading halt in place and overwhelming uncertainty, initiating new positions in DKME stock is exceptionally high-risk. It is prudent to wait for clarity on both the legal and delisting fronts.

- •Existing Shareholders – Prepare for All Scenarios: Since the stock is halted, options are limited. However, investors should mentally and financially prepare for outcomes ranging from a heavily diluted recovery to a complete loss via delisting.

In conclusion, the DKME Co., Ltd. management dispute has pushed the company to the brink. The convergence of legal battles, governance failures, and existing delisting threats creates a perfect storm of risk. Investors must prioritize capital preservation and avoid making decisions based on hope rather than a clear-eyed assessment of the severe challenges ahead.