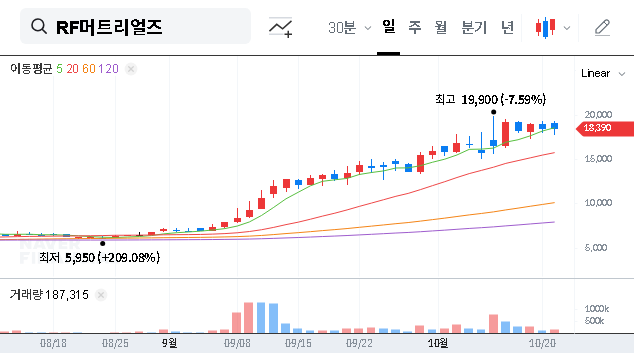

In a significant strategic pivot, RF Materials Co., Ltd. has announced a major RF Materials treasury stock disposal, a move squarely aimed at capturing the explosive growth within the AI sector. This decision to offload 4.5 billion KRW in shares is more than a financial maneuver; it’s a declaration of intent to become a key player in the high-stakes AI data center expansion race. For investors, this presents a critical question: is this a calculated risk paving the way for unprecedented growth, or does it introduce unwelcome volatility? This deep-dive investor analysis will unpack the details, implications, and strategic considerations you need to navigate this pivotal moment for RF Materials stock.

The Details of the Treasury Stock Disposal

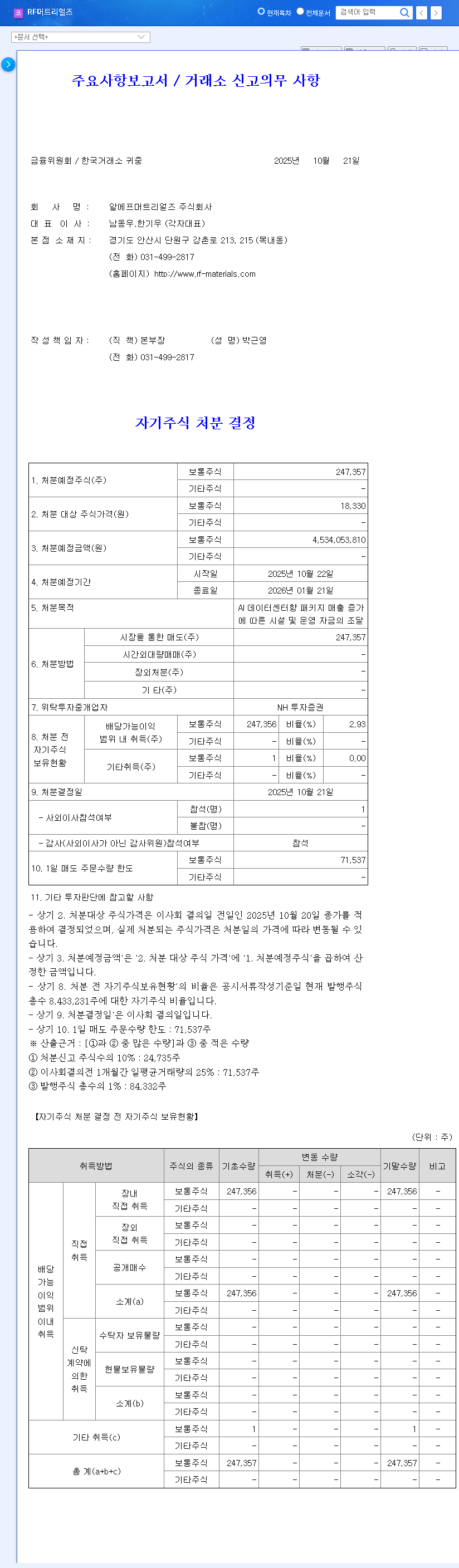

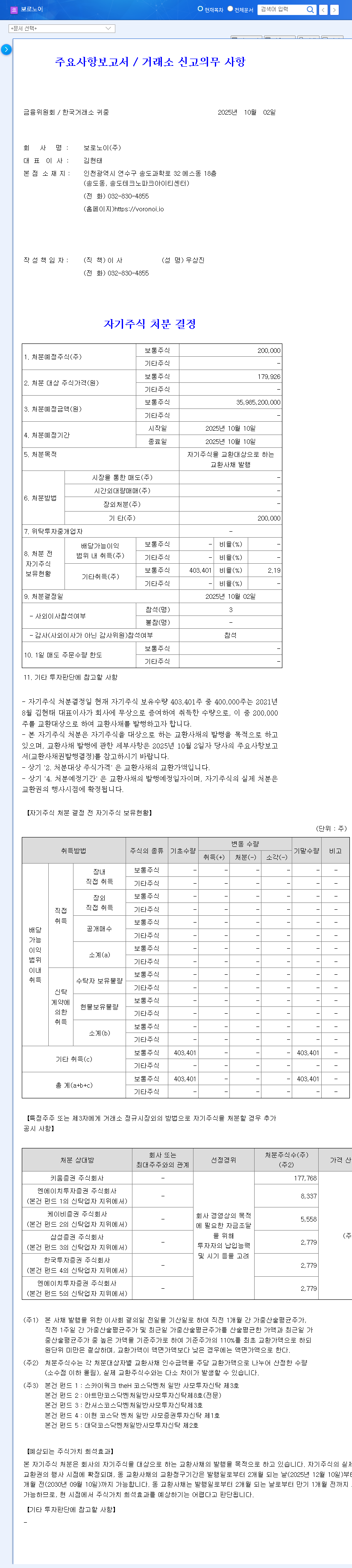

On October 21, 2025, the board of RF Materials Co., Ltd. officially resolved to dispose of 247,357 shares of its treasury stock. This transaction, valued at approximately 4.5 billion KRW, represents 2.93% of the company’s total outstanding shares. The disposal will be managed via a block deal through NH Investment & Securities, a move intended to ensure a stable and transparent process. The primary purpose, as stated in their public filing, is to secure vital capital for facility upgrades and operational expenses directly tied to the surging demand for their packages used in AI data centers. You can view the complete filing here: Official Disclosure (DART Source).

The core objective is clear: to channel funds directly into the company’s AI data center business, transforming existing market demand into a long-term, sustainable growth engine.

Strategic Rationale: Betting Big on AI Data Centers

The decision for the RF Materials treasury stock disposal was not made in a vacuum. It is a direct response to the seismic shifts in the technology landscape. The global AI market is fueling an unprecedented build-out of data centers, with industry reports from sources like Gartner projecting double-digit annual growth for the foreseeable future. These aren’t traditional data centers; they require specialized, high-performance components capable of handling immense computational loads and thermal outputs. RF Materials aims to supply critical ‘packages’—likely advanced semiconductor packaging or housing for AI accelerators—that are essential for the performance and reliability of these next-generation facilities. By securing 4.5 billion KRW now, the company intends to scale its production capabilities, invest in R&D for more advanced materials, and solidify its supply chain position before competitors can catch up.

Analyzing the Treasury Stock Disposal Impact

Any capital event of this nature has a dual impact. A comprehensive investor analysis must weigh the long-term strategic upside against the immediate market mechanics.

The Bull Case: Potential Positive Impacts

- •Accelerated Growth Engine: The capital injection directly fuels expansion in the high-margin AI data center market, potentially leading to significant revenue growth and enhanced profitability over the long term.

- •Enhanced Financial Stability: The immediate cash inflow strengthens the balance sheet, improves liquidity, and provides a buffer for operational scaling without necessarily taking on new debt.

- •Strategic Market Positioning: This proactive fundraising signals to the market that RF Materials is serious about capturing a significant share of the AI infrastructure boom.

The Bear Case: Potential Negative Impacts

- •Short-Term Share Dilution: The introduction of 247,357 new shares into the market increases the total number of circulating shares. This can exert downward pressure on the stock price in the short term as the supply increases. For a deeper understanding, you can read our guide on how to analyze share dilution.

- •Market Sentiment Risk: While the volume (2.93%) is not excessively large, the market’s reaction can be unpredictable. If investors focus solely on the dilution aspect, it could trigger temporary selling pressure on RF Materials stock.

- •Execution Risk: The success of this move hinges entirely on the company’s ability to effectively deploy the new capital and generate a return on investment that outweighs the cost of dilution.

Investor Action Plan & Key Considerations

For current and prospective investors, a wait-and-see approach combined with diligent monitoring is prudent. The focus should be on separating the short-term market noise from the long-term business trajectory.

1. Monitor Disposal Progress Closely

Keep an eye on the execution of the block trade. Key metrics to watch include the final disposal price per share and the speed at which the shares are absorbed by the market. A strong institutional uptake at a good price would be a bullish signal.

2. Scrutinize Future Capital Allocation

The most critical factor will be how RF Materials details its use of the funds. Look for subsequent announcements regarding specific facility expansions, new machinery purchases, or R&D milestones. Concrete plans are the best catalyst for building investor confidence.

3. Adopt a Long-Term Perspective

This RF Materials treasury stock disposal should be viewed as an investment in the company’s future. While short-term price fluctuations are possible, the ultimate success will be measured by revenue growth and market share gains in the AI sector over the next 2-5 years. The core of your investor analysis should focus on this long-term growth story.