The latest H1 2025 earnings report for BNK Financial Group Inc. presents a complex narrative for investors. As a cornerstone of South Korea’s regional financial market, the group showcases impressive capital strength. However, this stability is contrasted by emerging challenges, including declining profitability amid shifting interest rate policies and fierce market competition. This comprehensive analysis will dissect the group’s performance, evaluate the strategic implications of its recent dividend announcement, and outline a prudent investment strategy for navigating the path ahead.

H1 2025 Performance: A Tale of Two Realities

In the first half of 2025, the financial results for BNK Financial Group Inc. painted a mixed picture. While the group’s capital foundation remains rock-solid, its core profitability metrics have faced headwinds. Let’s break down the key indicators that define this period.

Key Financial Metrics

- •Capital Soundness: The consolidated BIS Capital Ratio stood at a robust 13.96%, significantly surpassing regulatory minimums and signaling excellent capital management and risk absorption capacity.

- •Interest Income Pressure: Net Interest Income (NII) saw a 2.3% year-on-year decline to KRW 1,443.9 billion. This was primarily driven by lower interest income from core deposit and loan activities, a direct reflection of a lower interest rate environment.

- •Profitability Metrics: Net profit attributable to controlling shareholders fell by 3.4% to KRW 475.8 billion. Consequently, Return on Assets (ROA) was 0.63%, and Return on Equity (ROE) was 8.97%.

- •Asset Quality: The group maintained stable asset quality, with a Non-Performing Loan (NPL) ratio of 1.62% and a delinquency ratio of 1.39%, indicating diligent risk management.

Segment Performance Breakdown

The performance varied significantly across the group’s subsidiaries. The banking segment, led by Busan Bank and Gyeongnam Bank, remains the profit engine, contributing 84.0% of the total. While Busan Bank delivered a solid KRW 251.7 billion in net profit, Gyeongnam Bank’s performance faltered, declining by KRW 45.8 billion to KRW 158.5 billion. The non-banking arms, including BNK Capital and BNK Savings Bank, also faced profitability slowdowns, though BNK Investment & Securities showed improvement.

Drivers Behind the Slowdown & The Dividend Signal

The performance of BNK Financial Group Inc. is not occurring in a vacuum. It is shaped by broad macroeconomic trends and specific company strategies. The downward pressure on profits is largely attributable to the external environment, including projected interest rate cuts in Korea, as discussed by financial analysts at reputable global news outlets. This trend directly squeezes the Net Interest Margin (NIM), the lifeblood of traditional banking.

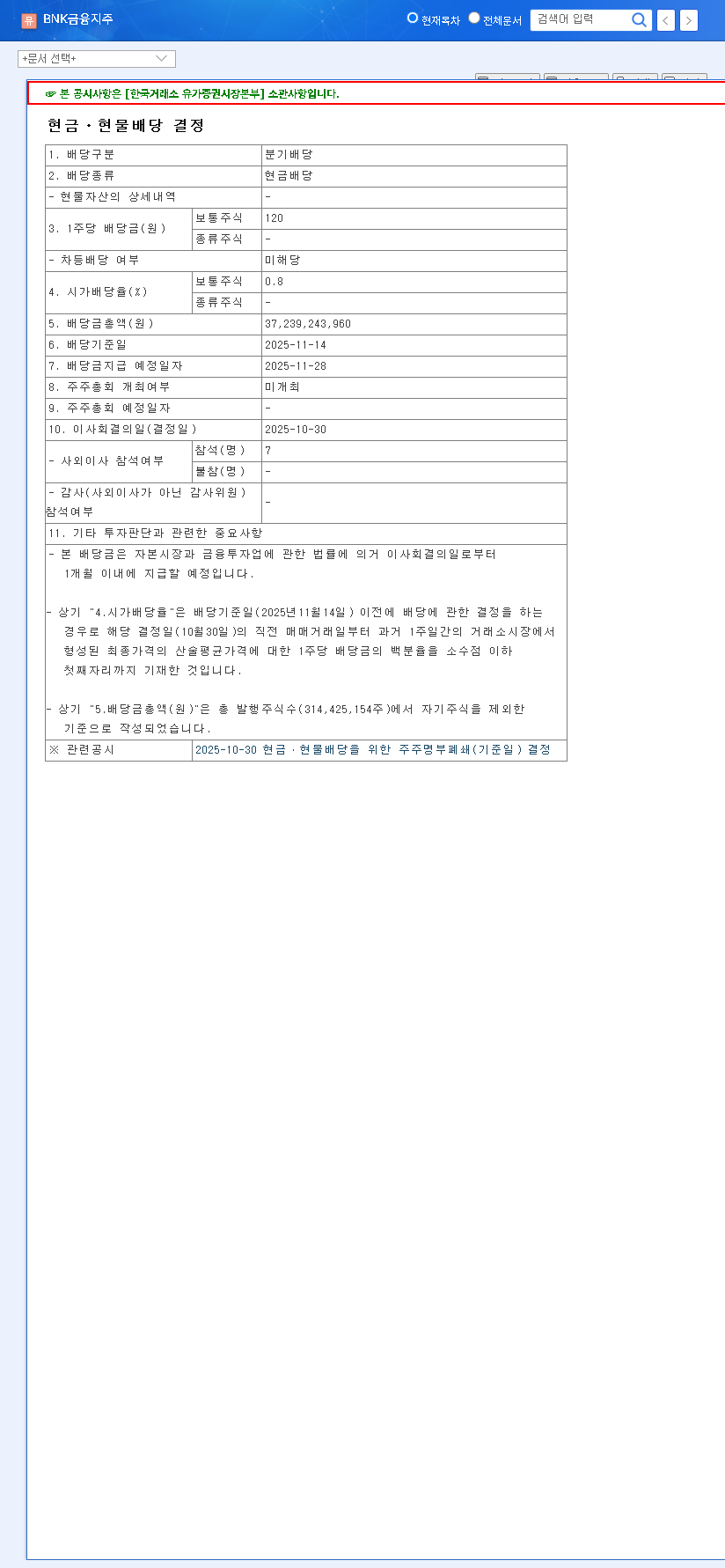

Despite these headwinds, the company’s commitment to shareholder returns remains unwavering, signaling confidence in its long-term financial stability and cash flow generation.

On October 30, 2025, the board announced a Q3 cash dividend of KRW 120 per common share. This decision is a crucial piece of the group’s plan to achieve a shareholder return ratio exceeding 50% by 2027. This move is a clear, positive signal to the market about management’s focus on shareholder value. The official filing can be reviewed here: Official Disclosure (DART).

Future Outlook: Strengths, Weaknesses, and Growth Drivers

Looking ahead, investors should weigh the group’s inherent strengths against its pressing challenges. The future success of any BNK Financial Group Inc. investment strategy depends on the company’s ability to leverage its advantages while mitigating its risks.

Positive Catalysts

- •Strong Capital Base: The high BIS ratio provides a formidable defense against economic shocks.

- •Digital Transformation: Ongoing investments in digital innovation and fintech partnerships are key to enhancing operational efficiency and long-term competitiveness.

- •Shareholder-Friendly Policies: The commitment to dividends and shareholder returns can attract and retain long-term investors.

Concerns and Challenges

- •Profitability Squeeze: Continued pressure on NII requires a strategic pivot towards growing non-interest income streams.

- •Non-Banking Diversification: Improving the performance and diversifying the portfolios of non-banking subsidiaries like BNK Capital is critical for balanced growth.

- •Risk Management: Past disciplinary actions necessitate a continued focus on strengthening internal controls to ensure long-term stability and investor trust.

Investment Thesis: A Neutral Stance with Key Monitors

Given the balance of strong capital and profitability pressures, the current investment opinion for BNK Financial Group Inc. is ‘Neutral’. A cautious, observant approach is recommended. Investors should closely monitor several key performance indicators before adjusting their position. For a deeper dive into financial metrics, consider reading our guide on how to analyze banking stocks.

Key Monitoring Points for Investors:

- •Quarterly changes in Net Interest Margin (NIM) and growth in non-interest income.

- •Profitability recovery in key subsidiaries, especially Gyeongnam Bank and BNK Capital.

- •Trends in asset quality metrics (NPL and delinquency rates).

- •Execution and sustainability of the announced shareholder return policy.

In conclusion, while the quarterly dividend is an encouraging sign of management’s confidence, fundamental improvements in earnings power must follow. Investment decisions should be based on tangible progress in addressing the group’s strategic challenges.