The Q3 2025 earnings report for the INDUSTRIAL BANK OF KOREA (IBK) presents a nuanced picture for investors. As a pivotal institution for South Korea’s Small and Medium-sized Enterprise (SME) sector, IBK’s performance is a critical barometer of the nation’s economic health. While the latest figures showcase financial stability and continued dominance in SME finance, they also reveal a significant deceleration in growth momentum amidst a challenging macroeconomic landscape. This deep-dive analysis unpacks the IBK Q3 2025 results, exploring the underlying causes and future strategies to provide a clear perspective for informed investment decisions.

IBK Q3 2025 Performance: A Tale of Stability and Slowdown

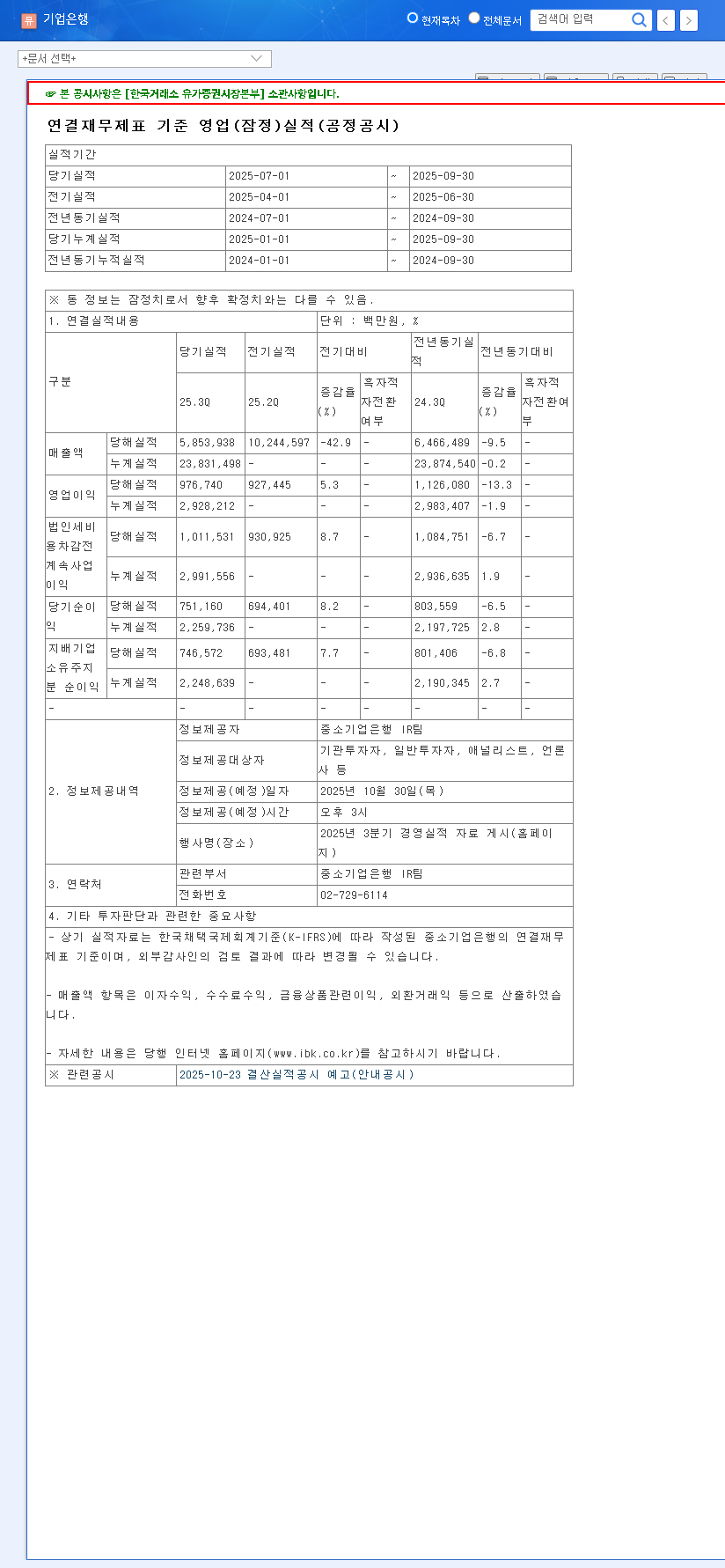

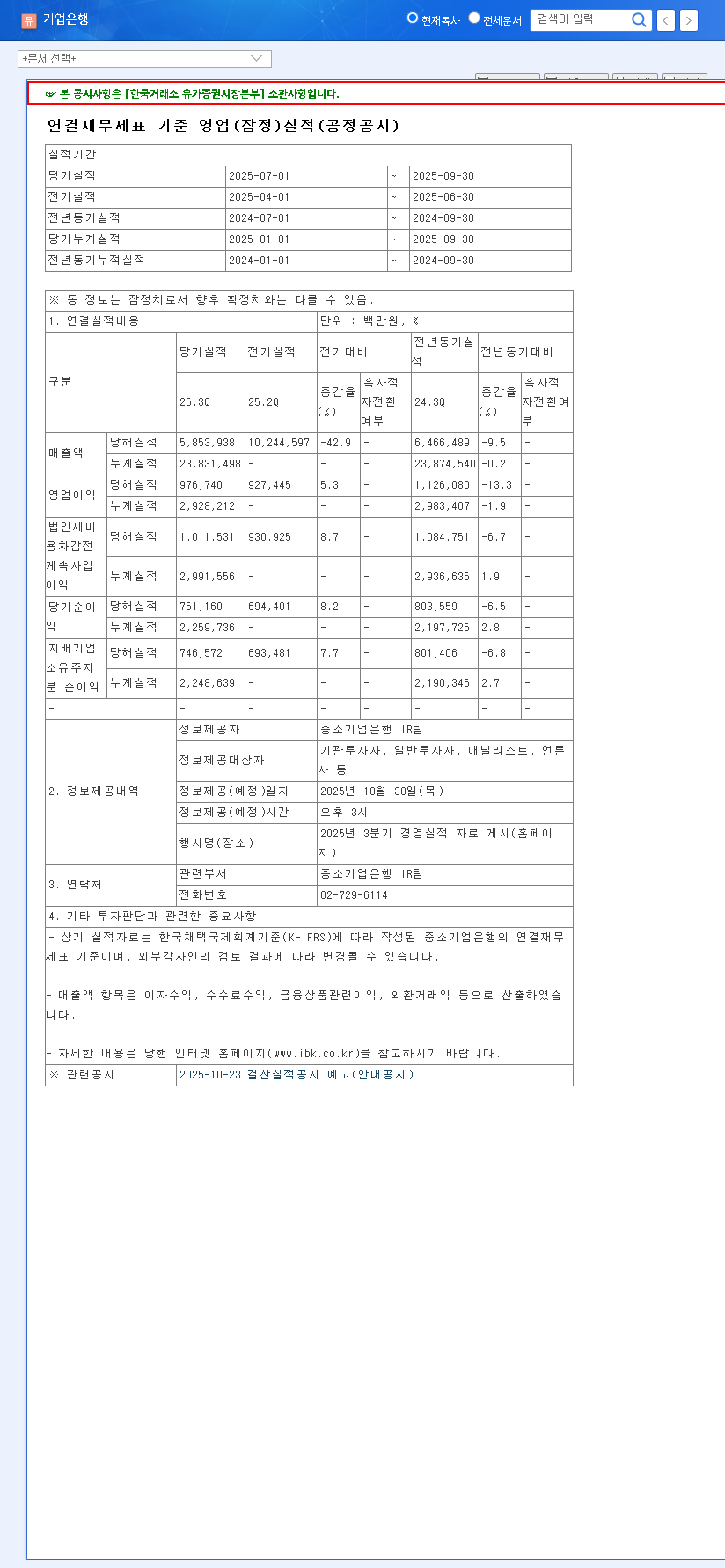

In its latest financial disclosure, the INDUSTRIAL BANK OF KOREA reported a consolidated net profit of KRW 2.2597 trillion and a separate net profit of KRW 1.9973 trillion for the third quarter of 2025. While the consolidated figure marked a modest 2.8% year-over-year increase, the separate net profit’s nearly flat growth of 0.1% signals clear headwinds. (Official Disclosure: Source)

Despite the growth concerns, IBK’s foundational strength remains evident. The bank reinforced its leadership in SME finance, with its SME loan balance reaching KRW 260.3 trillion, capturing an impressive market share of 24.33%. Key financial health indicators also remain robust, including a BIS capital ratio of 14.88% and a Liquidity Coverage Ratio (LCR) of 108.03%, well above regulatory requirements and indicating a strong capacity to withstand financial shocks.

While top-line stability is commendable, the minimal growth in separate net profit is a critical data point that investors must scrutinize. It reflects intensifying pressures that extend beyond IBK’s direct control.

Dissecting the Headwinds: Why the Growth Engine is Sputtering

The slowdown in IBK’s earnings growth is not an isolated issue but a reflection of a complex interplay of external factors. Understanding these pressures is key to a comprehensive IBK stock analysis.

Macroeconomic and Competitive Pressures

South Korea’s economy is navigating a period of low growth and persistent interest rate volatility, as reported by global financial analysts. This environment directly squeezes bank profitability. Furthermore, the financial market has become a battleground. Stiff competition from traditional banks and the agile entry of ‘big tech’ firms like Kakao Bank and Toss Bank are eroding margins and forcing incumbents like IBK to innovate rapidly or risk losing market share.

Internal Challenges and Subsidiary Performance

Internally, the performance of the broader IBK group has been dragged down by certain subsidiaries. Specifically, IBK Savings Bank has struggled amidst a downturn in the real estate project financing (PF) market and a rising number of vulnerable borrowers. This highlights the concentrated risks within specific sectors and the need for stringent group-wide risk management.

IBK’s Strategic Pivot: Charting a Course for Future Growth

In response to these challenges, the INDUSTRIAL BANK OF KOREA is not standing still. Management has outlined a multi-pronged strategy aimed at reigniting growth and building long-term resilience.

- •Revenue Diversification: A core focus is to boost non-interest income from investment banking, wealth management, and financial market activities, reducing reliance on traditional lending spreads.

- •Aggressive Digital Transformation: Enhancing mobile banking platforms, streamlining digital loan applications, and leveraging data analytics are crucial for improving efficiency and competing with fintech challengers.

- •New Growth Ventures: IBK is actively seeking new revenue streams by entering the green finance market and expanding financial support for high-potential technology and bio-health startups.

- •Global Expansion: The planned establishment of a subsidiary in Poland is a key step in expanding its global footprint, aiming to serve Korean companies operating in Europe and tap into new markets.

Investor Outlook: A ‘Neutral’ Stance with Key Monitors

Given the current landscape, our investment opinion for the INDUSTRIAL BANK OF KOREA is a cautious ‘Neutral’. The bank’s unique public-private role in SME finance, sound asset quality, and stable capital base provide a strong defensive floor. However, the evident slowdown in core profit growth, coupled with external uncertainties, caps the short-term upside potential.

Investors should closely monitor the execution of IBK’s growth strategies. Tangible progress in digital service adoption, non-interest income growth, and successful global expansion will be critical catalysts for a potential rating upgrade. For a broader context, investors can explore our analysis of the South Korean banking sector. Future IBK earnings reports will be crucial in determining if the bank can successfully navigate these turbulent waters.

Frequently Asked Questions (FAQ)

Q1: What was IBK’s net profit for Q3 2025?

A1: For Q3 2025, IBK reported a consolidated net profit of KRW 2.2597 trillion (a 2.8% YoY increase) and a separate net profit of KRW 1.9973 trillion (a 0.1% YoY increase).

Q2: Is the INDUSTRIAL BANK OF KOREA financially sound?

A2: Yes. With a BIS capital ratio of 14.88% and an LCR of 108.03%, IBK maintains a robust financial position with strong capital and liquidity buffers.

Q3: Why is IBK’s growth slowing down?

A3: The slowdown is due to a combination of macroeconomic uncertainty, intense market competition from traditional and tech-based banks, and the underperformance of some subsidiaries, particularly in the real estate sector.

Q4: What is the current investment outlook for IBK stock?

A4: The current investment outlook is ‘Neutral’. While its dominant position in SME finance is a major positive, the risks from slowing profit growth and a challenging economic environment warrant a cautious approach from investors.