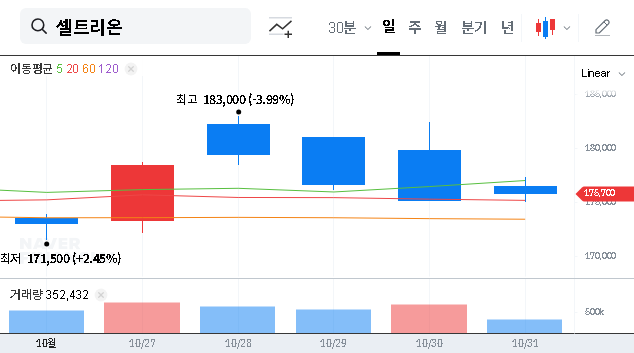

For those considering a Celltrion investment, the landscape just shifted dramatically. Biopharmaceutical giant Celltrion, Inc. has announced a landmark co-development and licensing agreement with Mustbio, valued at up to KRW 712.5 billion (approx. USD 520 million). This move, hot on the heels of the successful U.S. launch of Zymfentra, signals a bold new chapter for the company. This comprehensive Celltrion Inc. investment analysis will dissect the crucial details of this new drug deal, evaluate its potential impact on Celltrion’s valuation, and outline practical strategies for current and prospective investors.

Unpacking the Landmark KRW 712.5 Billion Deal

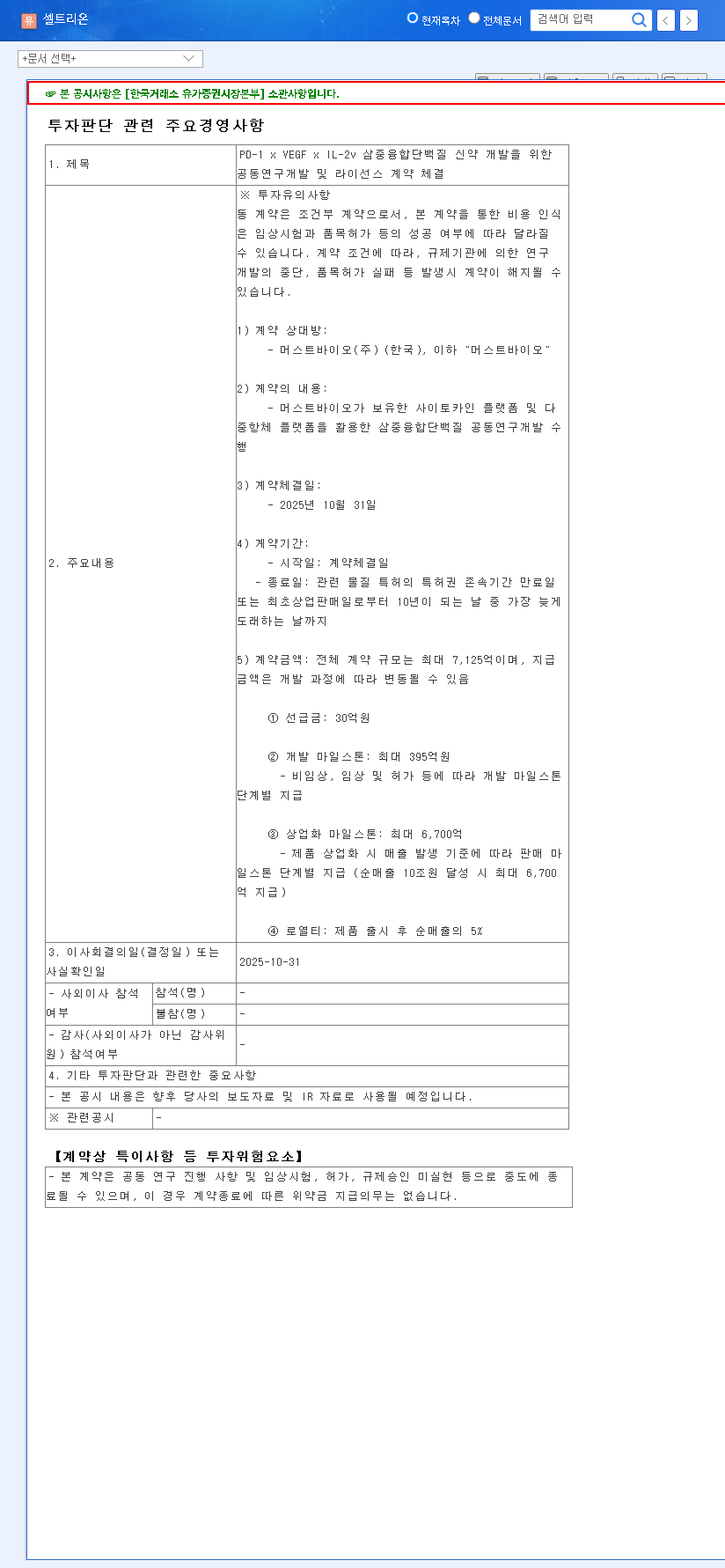

On October 31, 2025, Celltrion formalized a joint research and licensing agreement with Mustbio Co., Ltd. for an innovative “PD-1 x VEGF x IL-2v Triple Fusion Protein New Drug.” This next-generation therapeutic is designed for the highly competitive oncology market. The agreement structure is significant: an upfront payment of KRW 3 billion, followed by milestone payments tied to development and commercialization, plus a 5% royalty on net sales. The sheer scale of the deal is underscored by a potential KRW 670 billion milestone payment upon reaching KRW 10 trillion in cumulative net sales, highlighting the monumental expectations for this new drug. For full transparency, you can review the Official Disclosure (DART).

The Bull Case: Why This Deal Could Propel Celltrion Stock

1. A Strong Foundation & Proven Execution

Any sound Celltrion investment thesis must acknowledge its existing strengths. The company posted robust H1 2025 results with KRW 961.5 billion in sales and a healthy 25% operating margin. More importantly, the recent U.S. FDA approval and launch of Zymfentra (an injectable form of Remicade) serves as powerful validation of Celltrion’s drug development and commercialization capabilities. This success provides a solid financial and strategic launchpad for more ambitious projects like the Mustbio collaboration.

2. Fortifying the Next-Generation Drug Pipeline

This deal is a clear signal of Celltrion’s commitment to evolving beyond its biosimilar dominance. By partnering with Mustbio, Celltrion gains access to innovative cytokine and multi-antibody platform technology, which is crucial for creating next-generation cancer treatments. Key strategic benefits include:

- •Oncology Portfolio Diversification: Securing a high-potential asset in the lucrative oncology field.

- •Innovative Technology Access: Enhancing R&D efficiency for future drug discovery.

- •Future Revenue Streams: Successful commercialization opens doors for massive direct sales revenue or further out-licensing deals.

Celltrion is leveraging its stable, cash-generating biosimilar business to fund high-risk, high-reward ventures in novel drug development. This balanced approach is a key component of a long-term growth strategy.

A Prudent Investor’s Guide to Key Risks

No investment is without risk, especially in the volatile biopharmaceutical sector. Investors must remain vigilant of the following factors:

- •Clinical Trial Uncertainty: The agreement is conditional. New drug development is a long and arduous process with a high rate of failure. A setback in clinical trials could terminate the agreement and negatively impact Celltrion stock.

- •Intense Market Competition: The global oncology market is crowded with pharmaceutical giants. As noted by industry reports from sources like Bloomberg Intelligence, successful market penetration will require superior clinical data and a robust commercial strategy.

- •Macroeconomic Volatility: As an international deal, fluctuations in currency exchange rates can impact the real value of milestone payments and royalties. Broader economic factors like interest rates can also affect funding costs.

Investment Strategy & Overall Assessment

Our overall investment opinion on Celltrion, Inc. is Positive, particularly for investors with a long-term horizon. The Celltrion new drug deal represents a significant step towards becoming a fully-integrated global biopharmaceutical company. For those considering a position, we recommend the following approach:

- •Adopt a Long-Term Perspective: View this as a multi-year growth story. Consider a phased buying strategy to average your cost basis rather than focusing on short-term price movements.

- •Practice Diligent Risk Management: Closely monitor company disclosures regarding clinical trial progress and milestone achievements. This is critical for managing the inherent risks of biopharmaceutical investment.

- •Monitor the Competitive Landscape: Stay informed about competitor advancements and market trends. For more context, you can read our guide to understanding the biosimilar market.

Disclaimer: This report is for informational purposes only and does not constitute investment advice. All investment decisions are the sole responsibility of the investor.