In a challenging global economic climate, the recent announcement of the SeAH Steel Holdings exchangeable bond (EB) issuance, valued at 19.3 billion KRW, has sent ripples through the investment community. This isn’t just a standard fundraising effort; it’s a complex strategic maneuver that signals both the pressures the company is under and its ambitions for the future. For investors, this raises a critical question: does this EB represent a ground-floor opportunity or an investment challenge fraught with uncertainty?

This comprehensive analysis, based on the company’s official public disclosures, will dissect the fundamentals of SeAH Steel Holdings, explore the unique structure of the exchangeable bond, and evaluate the broader macroeconomic landscape. Our goal is to equip you with the essential insights needed to formulate a sound investment strategy regarding SeAH Steel’s stock and its future trajectory.

The Details: A KRW 19.3 Billion Private Placement

SeAH Steel Holdings is set to issue private placement exchangeable bonds worth KRW 19.3 billion to Shin Young Securities. According to the ‘Report on Major Matters (Decision on Issuance of Exchangeable Bonds)’, the issuance date is slated for October 1, 2025. You can view the complete filing here: Official Disclosure.

Two key terms of this SeAH Steel Holdings exchangeable bond stand out immediately:

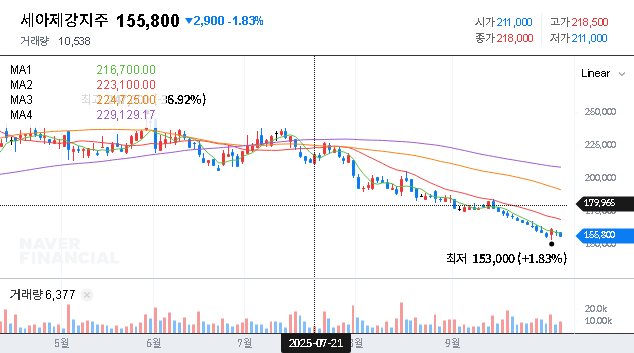

- •High Exchange Price: The exchange price is set at KRW 191,126, a stark contrast to the stock’s price of KRW 39,538 (as of the disclosure date). This makes immediate conversion highly improbable.

- •Zero-Coupon Bond: Both the surface and maturity interest rates are set at 0%, meaning the company secures the funds without any recurring interest payments.

Fundraising in a Downturn: Why Now?

A Challenging Financial Landscape

SeAH Steel Holdings is navigating a perfect storm. The company’s H1 2025 performance reveals a significant downturn, with revenue dropping by nearly 48% year-over-year and profits declining sharply. This is the result of a confluence of factors, including a global economic slowdown, deteriorating steel market conditions due to oversupply, and fluctuating raw material costs. As noted in authoritative industry reports from sources like Reuters, the entire steel sector is under pressure.

The financial data paints a clear picture of rising liabilities and shrinking profitability, putting pressure on the company’s balance sheet. In this environment, traditional bank loans may come with high interest rates. Issuing an exchangeable bond with a 0% coupon is an astute way to secure vital liquidity without adding the burden of immediate interest expenses.

This EB issuance is a calculated gamble. SeAH is securing interest-free capital now, betting that future growth and a rising stock price will turn this debt into equity, effectively deleveraging the company. Failure to achieve this growth means a lump-sum repayment looms at maturity.

Segment Performance and Future Bets

Weakness is apparent across key segments. The core Pipe segment has seen declining revenue and profit amidst fierce competition. While large projects like the Qatar LNG contract offer a silver lining, the overall trend is concerning. The Plate segment has fared worse, slipping into an operating deficit due to weak demand from the construction and home appliance industries.

Against this backdrop, the funds raised will be crucial. The market will be watching closely to see if they are deployed towards the company’s designated future growth engine: the offshore wind power business. A successful pivot into this green energy sector could redefine the company’s long-term valuation and justify the lofty exchange price.

Investment Strategy: Key Factors to Monitor

A prudent SeAH Steel investment requires careful monitoring of several key indicators. A conservative approach is warranted in the short term, but long-term potential exists if key catalysts align.

Your Monitoring Checklist

- •Capital Deployment: Track the specific use of the KRW 19.3 billion. Are funds being effectively invested in the offshore wind business or simply used to plug operational gaps?

- •Stock Price vs. Exchange Price: Monitor the gap between the stock price (KRW ~39k) and the exchange price (KRW 191k). A narrowing gap is a strong bullish signal, indicating market confidence in the company’s turnaround.

- •Steel Market Recovery: Keep an eye on global steel demand and pricing. A recovery in key sectors like construction, automotive, and energy is essential for the core business to rebound.

- •Macroeconomic Indicators: Fluctuations in exchange rates (EUR/KRW, USD/KRW), interest rates, and international oil prices will all impact costs, revenue, and overall profitability.

- •Financial Health Improvement: Look for trends of improving financial ratios, such as debt-to-equity, and a return to consistent profitability in quarterly earnings reports. For more information, read our guide on analyzing corporate financial statements.

In conclusion, the SeAH Steel Holdings exchangeable bond issuance is a pivotal event. It provides the company with a crucial financial lifeline and a pathway to invest in future growth. However, the success of this strategy is far from guaranteed. Investors must remain vigilant, weighing the immediate financial pressures against the long-term potential of the company’s strategic initiatives.