Justem.CO.,LTD (417840), a key player in semiconductor and display equipment, is poised for a significant strategic shift. With an investor relations (IR) conference scheduled for November 18, 2025, all eyes are on the company’s ambitious plans. The central theme of this event is expected to be the company’s Justem HBM market entry, a move that could redefine its growth trajectory in the AI-driven tech landscape. This analysis will provide a comprehensive overview of Justem’s capabilities, financial health, and the critical factors investors must watch during the upcoming IR briefing.

This deep dive explores Justem’s core business, the strategic importance of its venture into High-Bandwidth Memory (HBM), and a thorough analysis of its recent financial performance. We will unpack the potential impacts, both positive and negative, that this pivotal IR event could have on the company’s valuation and overall investor confidence.

Understanding Justem: Core Competencies & Market Position

Justem.CO.,LTD has established itself as a critical technology provider, specializing in manufacturing equipment for semiconductor and display fabrication. Its primary competitive advantage lies in its unique technological prowess in the N₂ Purge Load Port market. This technology is essential for maintaining an ultra-clean, inert environment during wafer handling, which is crucial for maximizing yields in advanced semiconductor manufacturing. The company is actively strengthening its global footprint by expanding its client base to include major overseas Integrated Device Manufacturers (IDMs), creating a more stable and diversified revenue stream.

The Strategic Pivot: Justem’s HBM Market Entry

The most significant growth driver on the horizon is the planned Justem HBM market entry. High-Bandwidth Memory is a critical component for powering AI, machine learning, and high-performance computing (HPC) applications, representing one of the fastest-growing segments in the semiconductor industry. HBM involves stacking DRAM chips vertically to achieve significantly higher bandwidth and lower power consumption compared to traditional memory.

By developing specialized equipment for HBM manufacturing processes, Justem is positioning itself to capitalize on the explosive demand for AI hardware. This move is not just an expansion; it’s a strategic alignment with the future of technology.

The complexity of HBM manufacturing requires highly specialized equipment for processes like wafer bonding and advanced packaging. Justem’s expertise in precision equipment gives it a credible foundation to enter this lucrative market. Success in this area could create substantial new revenue streams and elevate the company’s status in the global supply chain. For further reading on HBM technology, you can explore resources from leading tech publications like AnandTech’s HBM overview.

Financial Health Check: Q3 2025 Performance

Justem’s latest financial data from Q3 2025 (consolidated) paints a picture of a stable and financially sound company. This stability provides the necessary foundation for its ambitious growth plans, including the Justem HBM market entry.

- •Total Assets: KRW 84.3 billion

- •Total Liabilities: KRW 31.7 billion

- •Total Equity: KRW 52.7 billion

- •Revenue: KRW 34.0 billion

- •Operating Profit: KRW 4.3 billion

An improving profitability trend and a consistent R&D investment of over 10% of revenue are strong positive signals. This commitment to innovation is vital for securing a competitive edge in fast-moving sectors like semiconductor equipment. For more details, explore our guide on analyzing tech company financials.

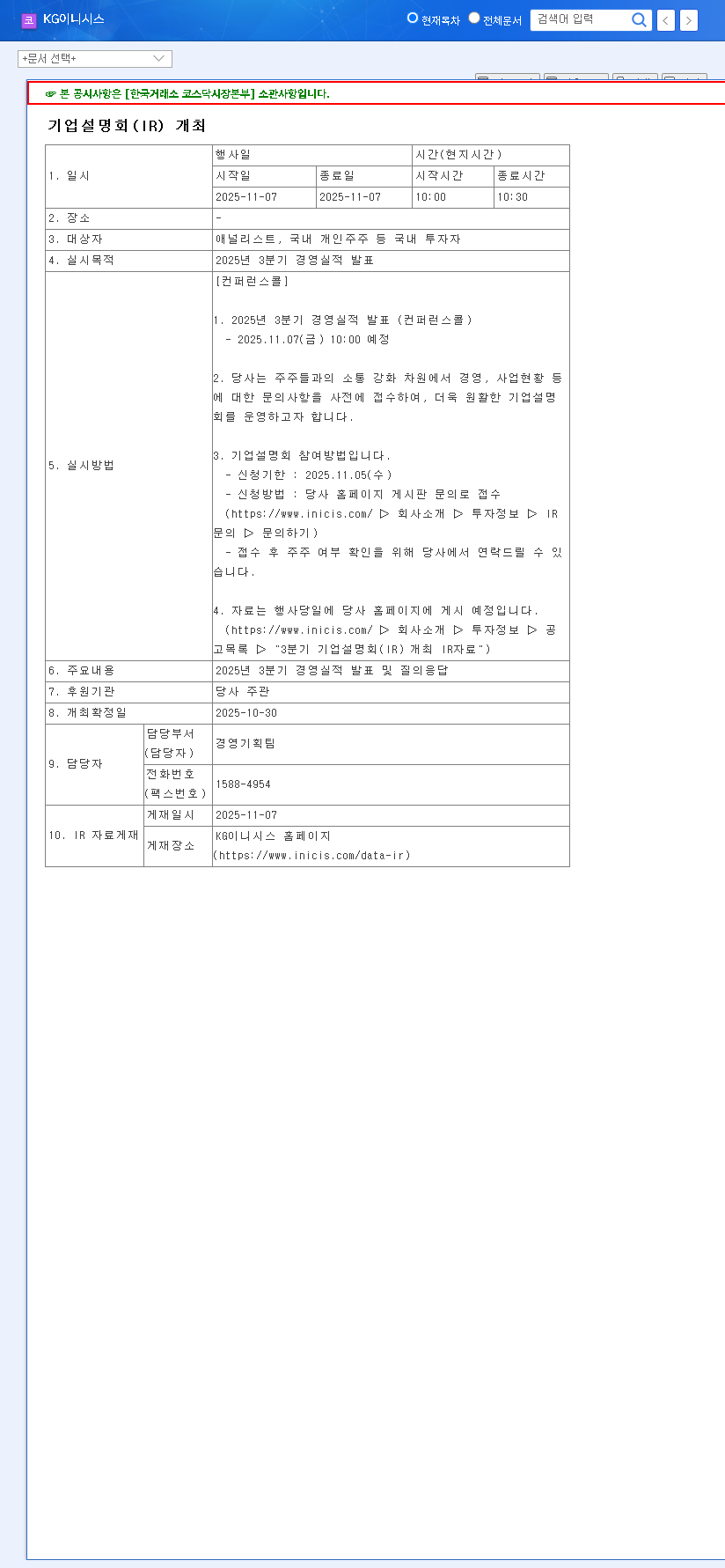

The Upcoming Justem Investor Relations Call: What to Expect

The IR conference on November 18, 2025, at 4:00 PM (KST) is a critical event. According to the Official Disclosure, the purpose is to enhance investor understanding of the company’s vision and business status. The Q&A session will be particularly telling.

Key Questions for Management

Investors should listen for clear, concrete answers to several key questions:

- •HBM Strategy Roadmap: What is the specific timeline for equipment development and market launch? Who are the target customers?

- •Client Diversification: What progress has been made in reducing reliance on its largest customer (Company B)?

- •Financial Risks: How is the company managing financial volatility related to convertible bonds and derivative products?

- •Competitive Landscape: How does Justem plan to compete with established players in the HBM equipment space?

Conclusion: A Pivotal Moment for Justem (417840)

Justem.CO.,LTD is at a crossroads. The upcoming Justem investor relations call will provide crucial insights into its future. A well-articulated and credible strategy for the Justem HBM market entry could significantly boost investor confidence and act as a powerful catalyst for the stock price. Conversely, vague answers or an unconvincing roadmap could introduce uncertainty and short-term volatility.

Investors should approach this event with a critical eye, focusing on the substance and feasibility of management’s plans. The decisions made and the strategies unveiled in the coming months will be instrumental in determining whether Justem can successfully transition from a stable equipment supplier to a high-growth player in the AI revolution.