The recent CJ CheilJedang CJ Feed&Care sale has sent ripples through the market, marking a pivotal moment in the company’s long-term strategy. This significant divestiture, involving CJ Feed&Care Co., Ltd. and 13 other subsidiaries to De Heus Animal Nutrition B.V., is far more than a simple asset sale. It represents a calculated move to sharpen focus, bolster financial health, and accelerate investment into high-growth sectors. This analysis will dissect the background of the deal, its strategic implications, and its potential impact on CJ CheilJedang’s future corporate value, providing clear insights for investors and industry observers.

Transaction Overview: The Core Details

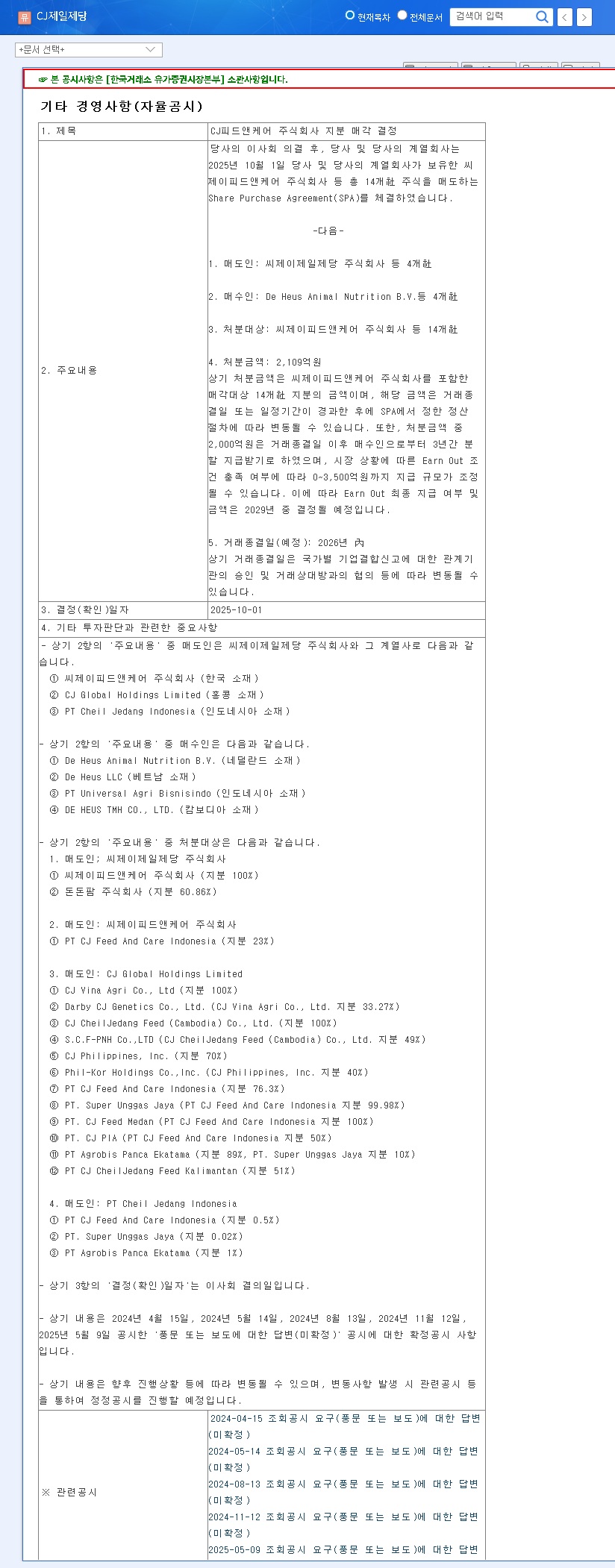

On October 1, 2025, CJ CheilJedang’s board of directors approved the agreement to divest its entire stake in the Feed & Care (F&C) business. This decision was formally announced in a regulatory filing. You can view the Official Disclosure on DART for complete transparency. Here are the key transaction points:

- •Seller: CJ CheilJedang Corporation and 4 affiliated companies.

- •Buyer: De Heus Animal Nutrition B.V. and 4 other entities.

- •Disposal Target: A total of 14 companies, headlined by CJ Feed&Care Co., Ltd.

- •Disposal Amount: Provisional sum of KRW 210.9 billion, with a potential additional KRW 0-350 billion based on Earn-out conditions.

- •Payment Terms: KRW 200 billion paid in installments over 3 years post-closing, with the Earn-out determined by 2029.

- •Expected Closing: Within 2026, contingent upon regulatory approvals.

The ‘Why Now?’: Strategic Rationale Behind the Divestiture

The timing of the CJ CheilJedang CJ Feed&Care sale is not arbitrary. It reflects a proactive strategy to navigate market volatility and double down on core strengths. The rationale can be broken down into three key pillars.

1. Laser Focus on High-Value Core Businesses

The F&C business, while stable, has demonstrated lower profitability and growth potential compared to CJ CheilJedang’s thriving Food and BIO segments. By divesting, the company can redirect capital, talent, and executive attention toward these high-margin, high-growth areas. This move is a classic example of portfolio optimization designed to enhance overall corporate competitiveness and align with long-term growth trends in wellness and biotechnology.

This strategic pivot allows CJ CheilJedang to exit a highly competitive, lower-margin industry to fully capitalize on its innovative strengths in the global Food and BIO markets.

2. Fortifying the Financial Foundation

The infusion of over KRW 210 billion (and potentially more) will significantly de-leverage the balance sheet and enhance financial soundness. The structured payment terms ensure a stable, long-term cash inflow, which can be strategically deployed for debt reduction. This improves key financial metrics and provides a robust buffer against economic headwinds, a prudent move in today’s uncertain global economy. For more on market trends, see this analysis on global M&A activity from Bloomberg.

3. Fueling Future Growth Engines

The proceeds are earmarked for reinvestment. This capital will likely fuel aggressive R&D in areas like alternative proteins, microbiome technology, and advanced bio-fermentation. By funding innovation, CJ CheilJedang is not just optimizing its current portfolio but actively building its next generation of revenue streams. To learn more, read our deep dive into CJ CheilJedang’s BIO Business Strategy.

Impact on Fundamentals & Investor Outlook

This divestiture is poised to have a multi-faceted, largely positive impact on CJ CheilJedang’s fundamentals. While a short-term dip in consolidated revenue is expected due to the exclusion of the F&C segment, the long-term outlook is promising.

Key Investment Positives

- •Improved Profitability: Exiting the lower-margin F&C business is expected to lift the company’s overall operating profit margin, net profit margin, and Return on Equity (ROE).

- •Enhanced Financial Health: Significant cash inflow will reduce debt and strengthen the balance sheet, increasing corporate resilience.

- •Accelerated Growth: Concentrated investment in high-potential Food and BIO sectors can unlock new growth S-curves and enhance long-term shareholder value.

Potential Risks to Monitor

- •Earn-out Uncertainty: The final sale price is variable, introducing uncertainty into cash flow projections until 2029.

- •Execution Risk: The successful reinvestment of capital into new ventures requires flawless execution and market acceptance.

- •Transaction Delays: The closing is subject to antitrust and other regulatory approvals, which could introduce unforeseen delays.

In conclusion, the CJ CheilJedang CJ Feed&Care sale is a decisive strategic action that positions the company for a more profitable and innovative future. While investors should monitor the associated risks, the move is a clear positive signal of management’s commitment to optimizing its portfolio and creating sustainable, long-term value.