This comprehensive Corentec Q3 2025 earnings analysis provides a deep dive into the company’s latest financial report. Corentec Co., Ltd. (KRX: 104540) has captured significant investor attention following its provisional Q3 2025 results, which showcased a dramatic turnaround in profitability. With a remarkable 157% surge in operating profit and a return to net positive income, the market is buzzing with questions. Does this signal a sustainable growth trajectory, or should investors remain cautious? We will dissect the numbers, explore the underlying growth drivers, and evaluate the potential risks to provide a clear outlook on the Corentec stock analysis.

Corentec’s Q3 2025 Performance: A Stunning Turnaround

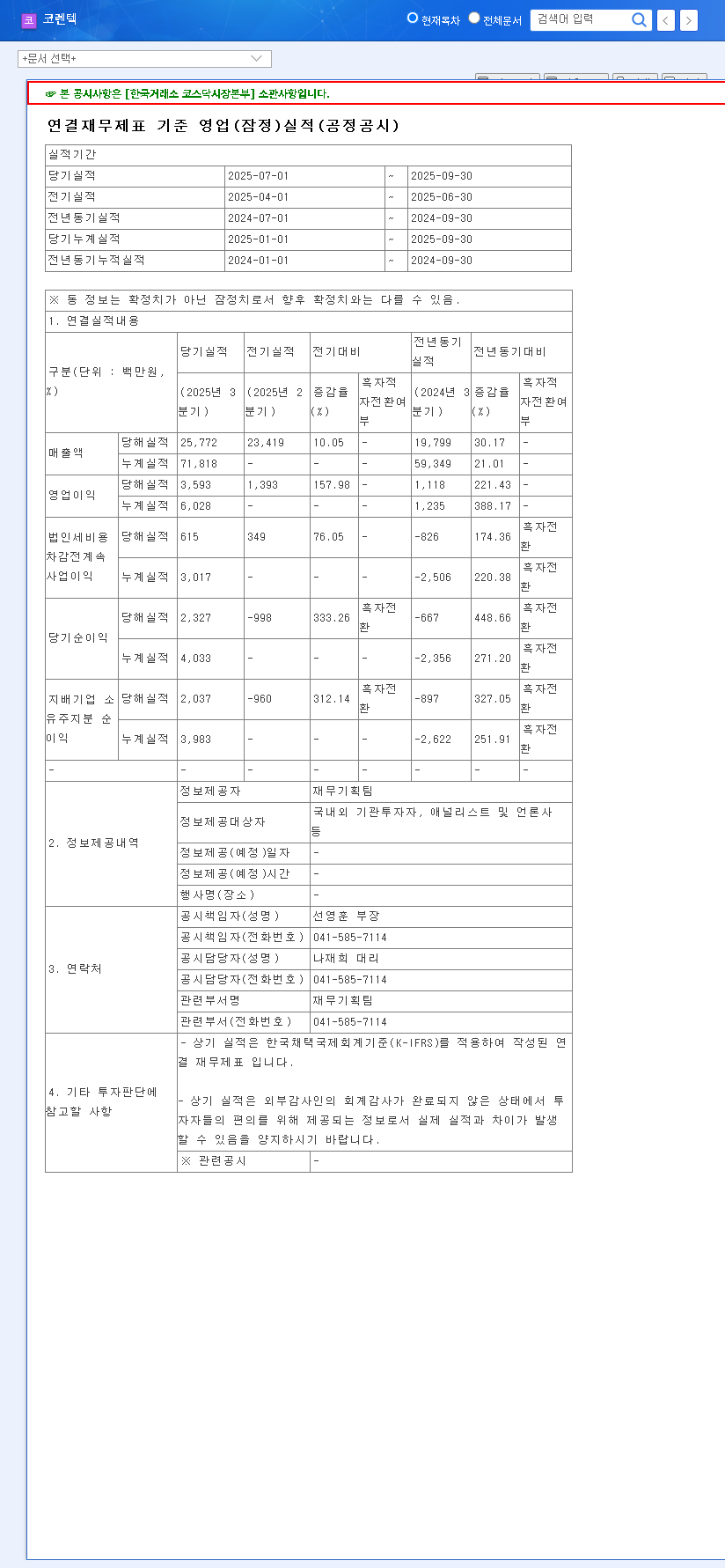

On November 3, 2025, Corentec released its provisional consolidated Q3 earnings, sending a wave of optimism through the market. The Corentec financial report revealed significant improvements across all key metrics compared to the previous quarter. For more details, see the Official Disclosure (Source).

- •Revenue: KRW 25.8 billion (a 10% increase quarter-over-quarter)

- •Operating Profit: KRW 3.6 billion (a staggering 157% increase quarter-over-quarter)

- •Net Profit: KRW 2.0 billion (a significant reversal to black from Q2’s KRW 1.0 billion loss)

This robust performance not only reverses the losses seen in previous quarters but also suggests a fundamental strengthening of the company’s operational efficiency and market position, raising expectations for sustained profitability.

What’s Fueling Corentec’s Growth Engine?

This impressive turnaround isn’t attributable to a single event but rather a combination of strategic initiatives and favorable market conditions. The Corentec earnings analysis points to three core pillars supporting this growth.

1. Strengthened Financial Health and Efficiency

Corentec has actively worked to streamline its financial structure. By strategically selling and liquidating non-core subsidiaries, the company has reduced overhead and sharpened its focus on its primary artificial joint business. This has enhanced operational efficiency and contributed directly to the improved bottom line.

2. Aggressive Overseas Market Expansion

A crucial milestone was achieved with the U.S. FDA approval for its UCR type tibial insert for artificial knee joints. This approval is more than just a regulatory hurdle; it’s a gateway to the lucrative North American market, one of the largest for orthopedic devices globally. This opens up a significant new revenue stream and is a key factor in any long-term Corentec stock analysis.

3. Unique Technological Competitiveness

Corentec’s market leadership is underpinned by its proprietary technologies. Innovations like 3D printing for custom implants and advanced Z-coating for enhanced biocompatibility give it a distinct edge. These technologies have solidified its #1 position in the domestic hip joint market and a strong 13.8% share in the knee joint market. The macro-trend of an aging global population ensures a steadily growing demand for these advanced artificial joints, as reported by industry analysts like Grand View Research.

Despite the strong Q3 2025 results, a comprehensive Corentec earnings analysis must also weigh the significant financial risks. A ‘Neutral’ investment opinion remains prudent until sustained profitability and debt management are demonstrated.

Navigating the Risks: What Investors Must Watch

While the Corentec Q3 2025 earnings are promising, investors should not overlook several persistent risk factors that could impact future performance.

- •High Financial Burden: The company’s balance sheet still carries a high debt ratio, including variable interest rate borrowings, derivative liabilities, and convertible bonds. This makes Corentec vulnerable to interest rate hikes, which could significantly increase interest expenses and erode profitability.

- •Historical Profit Volatility: A single strong quarter does not erase a history of fluctuating profits, including recent net losses in Q3 2024 and Q2 2025. Consistent performance over several quarters is needed to build investor confidence.

- •Currency Exchange Rate Risk: As a company with growing international exposure, Corentec is susceptible to volatility in KRW/USD and KRW/EUR exchange rates, which can impact both revenue and cost of goods sold.

Investment Outlook & Key Monitoring Points

Corentec’s strong Q3 2025 earnings report clearly signals a potential turning point. The combination of FDA approval, technological leadership, and a growing market provides powerful long-term growth momentum. However, due to the financial risks and past volatility, a cautious ‘Neutral’ stance is advisable for now. Investors should closely monitor the following points in upcoming Corentec financial reports:

- •Overseas Sales Traction: Monitor the actual sales figures from the U.S. market and their contribution to overall revenue.

- •Debt Reduction Efforts: Look for concrete steps to improve the debt ratio and manage risks associated with variable interest borrowings.

- •Profitability Consistency: Check if the strong performance of Q3 can be maintained or improved upon in subsequent quarters.

Continued diligence and a careful review of Corentec’s next quarterly earnings are essential for making an informed investment decision.