The latest SHINSEGAE INTERNATIONAL Inc. (031430) earnings report for Q3 2025 has sent a seismic shock through the investment community. The preliminary results reveal a startling plunge into a significant operating and net loss, starkly contrasting with market expectations and raising urgent questions about the company’s trajectory. For investors, this moment demands a critical re-evaluation of their strategy.

This comprehensive analysis dissects the official preliminary earnings disclosure, explores the fundamental weaknesses and macroeconomic pressures driving this downturn, and forecasts the potential impact on the SHINSEGAE INTERNATIONAL stock price. We will provide a clear, actionable framework for navigating the current uncertainty surrounding this fashion and lifestyle giant.

The Alarming Numbers: Q3 2025 Preliminary Earnings Breakdown

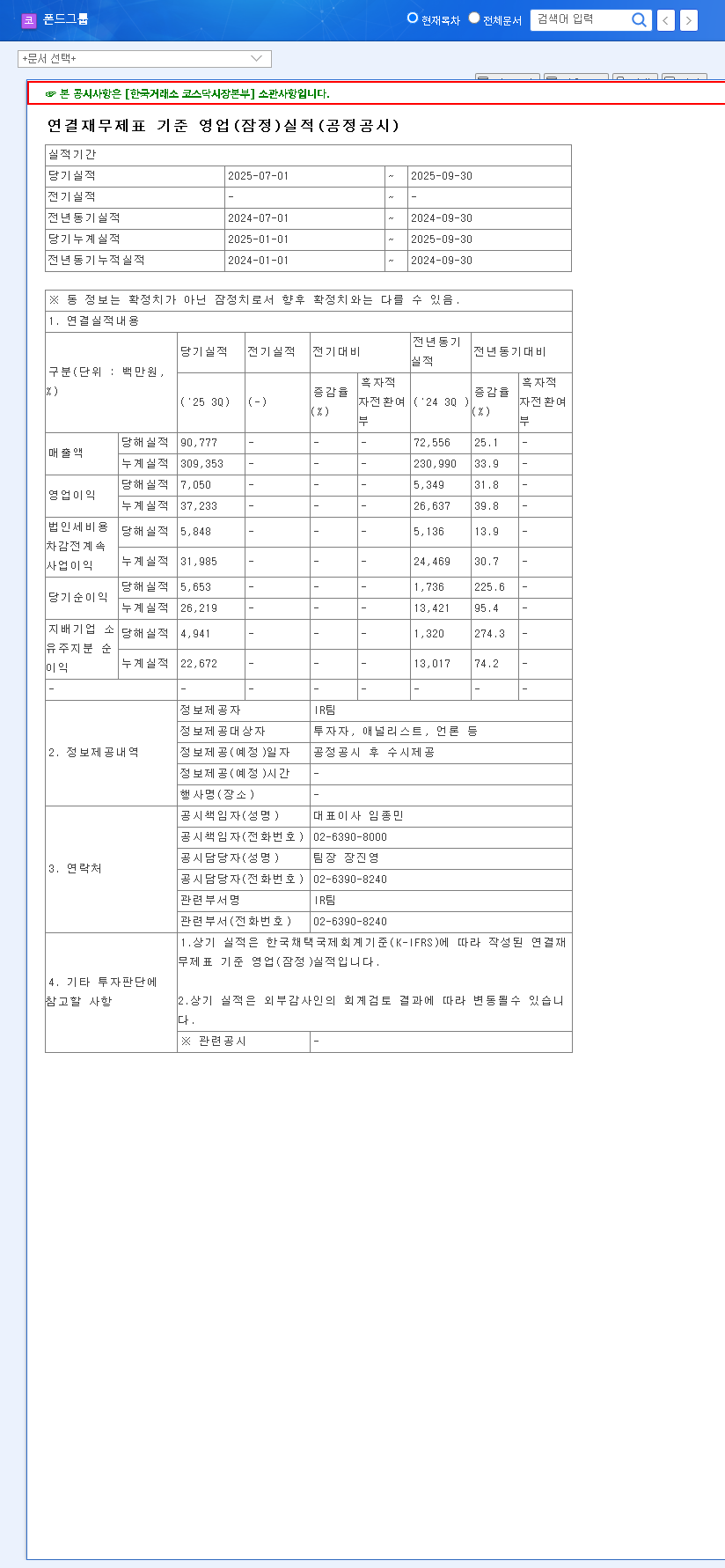

On November 7, 2025, SHINSEGAE INTERNATIONAL Inc. released its preliminary operating results, which you can view in the Official Disclosure (DART). While revenue held steady, profitability fell off a cliff.

- •Revenue: KRW 310.4 billion (Only 1% below the estimate of KRW 312.3 billion).

- •Operating Profit: KRW -2.0 billion (A staggering 218% below the estimate of KRW 1.7 billion).

- •Net Profit: KRW -1.9 billion (An incredible 480% below the estimate of KRW 0.5 billion).

The transition from an expected profit to a substantial deficit represents a critical failure in operational efficiency and cost management, signaling deep-seated issues that go beyond a simple market downturn.

Core Risk Factors: Why Did Performance Collapse?

While the company has positive attributes like its ‘A1’ credit rating and brand strength in ‘JAJU’, several severe risk factors have converged to create this perfect storm. Understanding these is key to a sound investor strategy.

The Subsidiary Drag: Shinsegae Tomboy Co.’s Devastating Impact

A primary contributor to the parent company’s loss is the catastrophic performance of its key subsidiary, Shinsegae Tomboy Co., Ltd. With a reported 96.3% decline in profitability, this subsidiary has acted as a significant anchor on the consolidated results. This isn’t just a minor issue; it points to a potential crisis within a core part of the business portfolio that requires immediate and drastic intervention.

Macroeconomic Headwinds and Currency Exposure

The company’s business model, heavily reliant on importing foreign brands, is acutely vulnerable to exchange rate fluctuations. The recent depreciation of the Korean Won against the US Dollar and Euro directly inflates costs of goods sold, squeezing margins. This external pressure, combined with weakening domestic consumer sentiment as reported by sources like Reuters, creates a hostile operating environment for a company in the premium fashion and lifestyle sector.

Internal Financial Health Concerns

An existing debt ratio of 60.57%, considered high, becomes more perilous in a climate of rising interest rates and falling profits. This leverage increases the burden of interest expenses, further eroding the bottom line and raising valid concerns about the company’s long-term financial stability if profitability cannot be swiftly restored.

The Q3 2025 earnings shock is more than a single bad quarter; it is a clear warning sign of fundamental and macroeconomic challenges converging, demanding a deeply conservative and watchful investor approach.

Forecast: Market Impact & Stock Price Outlook

The fallout from this report is expected to be swift and significant. The market abhors negative surprises, and this is a substantial one. We anticipate the following impacts:

- •Immediate Stock Price Pressure: Expect significant downward pressure on the SHINSEGAE INTERNATIONAL stock price as the market digests the news. A re-rating based on lowered future earnings expectations is likely.

- •Erosion of Investor Confidence: The company’s credibility in forecasting and managing its operations will be damaged. Efforts like treasury stock cancellation will be overshadowed by this operational failure.

- •Credit Rating Scrutiny: While currently stable at ‘A1’, continued losses could put this rating under review by credit agencies, which would increase future borrowing costs.

Investor Action Plan & Strategic Outlook

Given the severity of the 031430 Q3 2025 analysis, a defensive and cautious investor strategy is paramount. A rapid turnaround seems unlikely without a clear and decisive strategic shift from management.

Recommendations for Investors:

- •Adopt a ‘Wait and See’ Stance: Avoid trying to catch a falling knife. It is prudent to wait for the company’s official response and detailed turnaround plan before considering any new positions.

- •Monitor Key Metrics: Closely watch for management’s strategy to revive Shinsegae Tomboy Co., announcements on cost-cutting measures, and plans to mitigate currency risk.

- •Re-evaluate Risk Tolerance: For those already invested, this event necessitates a re-evaluation of the stock’s role in your portfolio. Investment opinions should shift from ‘Neutral’ towards ‘Underweight’ or ‘Sell’ until a clear path to profitability emerges. For more on this, you can review our guide to corporate earnings analysis.

In conclusion, the SHINSEGAE INTERNATIONAL Inc. (031430) earnings for Q3 2025 are a significant negative development. The company faces a severe profitability crisis that requires a comprehensive overhaul of its operational and financial strategies. Investors should proceed with extreme caution, prioritizing capital preservation until there is concrete evidence of a sustainable recovery.