The recent announcement of the KYUNG DONG NAVIEN capital increase has sent ripples through the investment community. The company, a dominant force in the living environment and energy sector, plans to inject ₩119.7 billion into its subsidiary, Kyung Dong Polium Co., Ltd. This move presents a classic investor dilemma: is it a strategic investment paving the way for future dominance, or will the resulting share dilution negatively impact current shareholder value? This in-depth KD Navien stock analysis will dissect the details, explore the potential outcomes, and provide investors with a clear framework for making informed decisions.

We will examine the fundamentals driving this decision, the immediate financial implications, and the broader market context to understand whether this capital raise is a masterstroke for long-term growth or a necessary but painful short-term measure.

Dissecting the KYUNG DONG NAVIEN Capital Increase

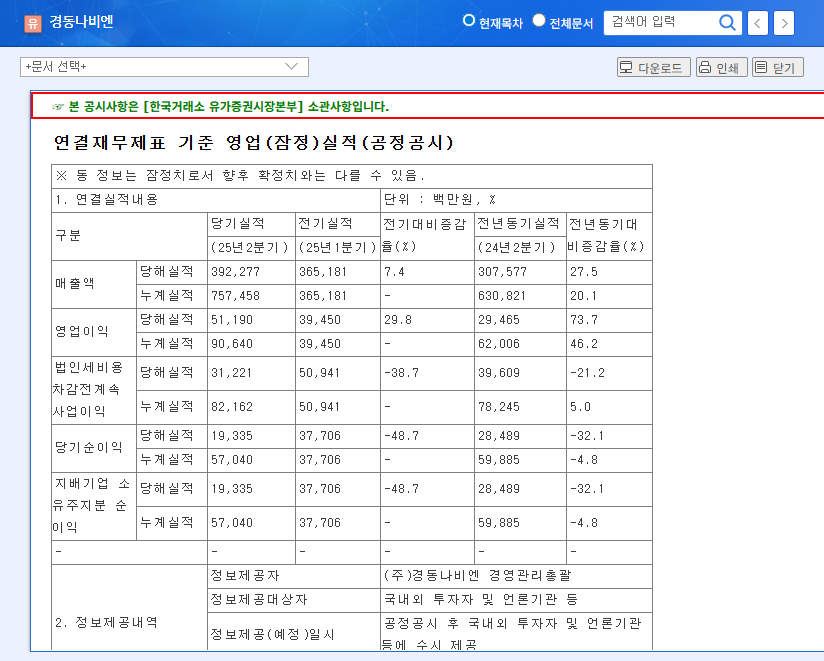

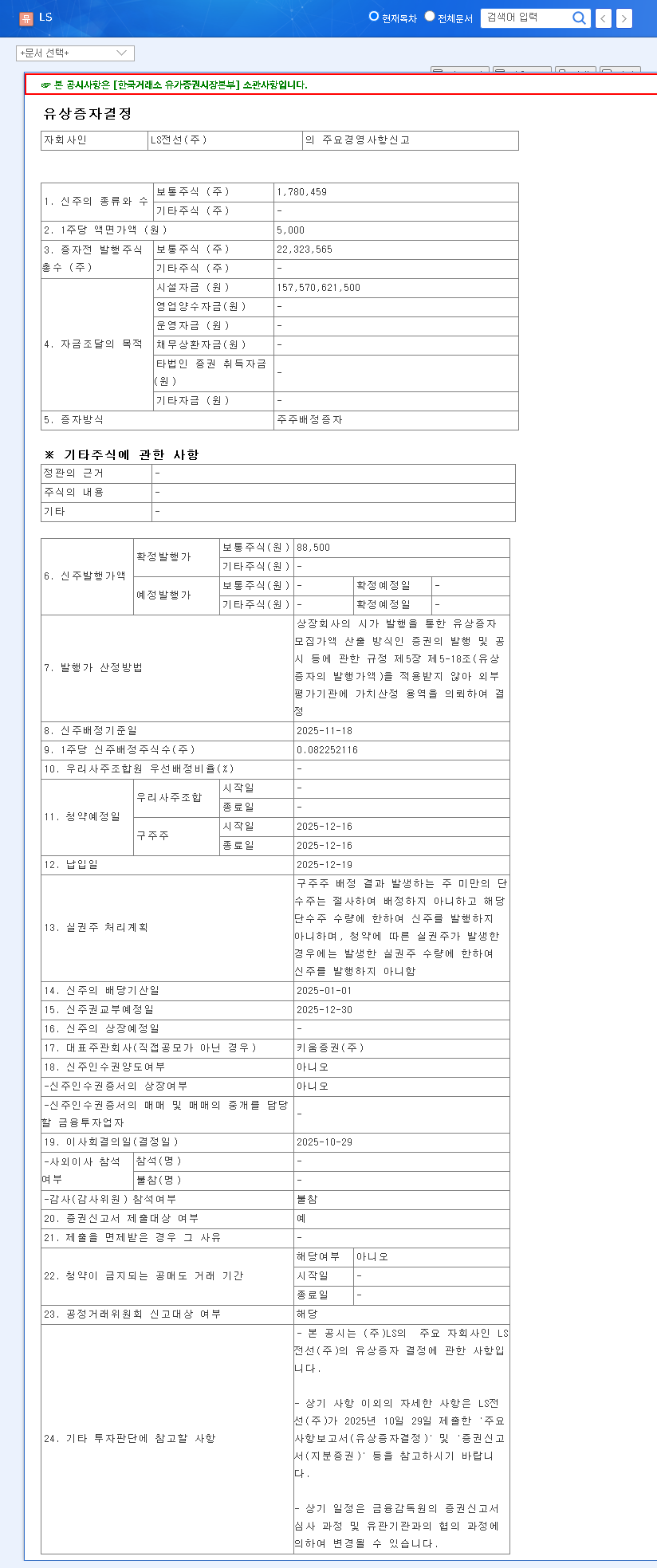

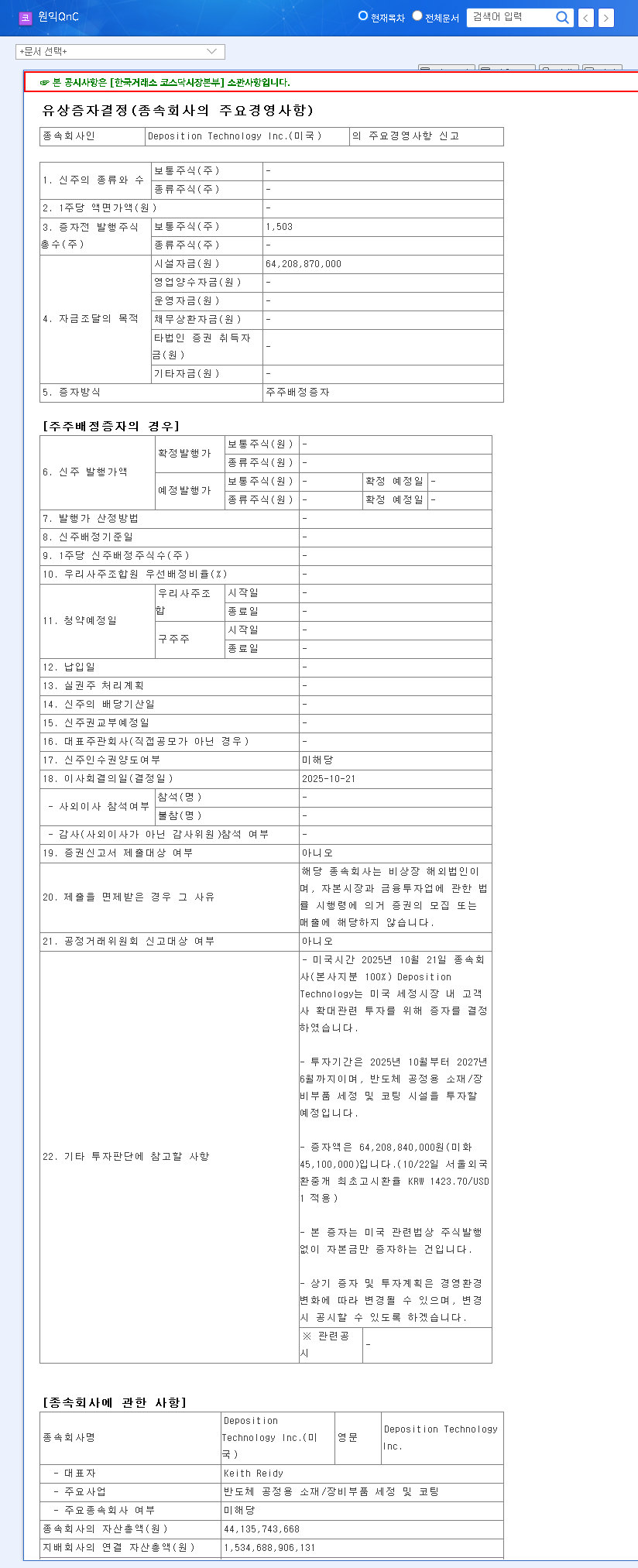

On November 12, 2025, KYUNG DONG NAVIEN formally announced its decision to execute a significant capital increase valued at ₩119.7 billion. According to the Official Disclosure filed with DART, this transaction is structured as a shareholder-allocated rights offering. This means existing shareholders will have the right to purchase new shares, specifically at a ratio of 1.33 new shares for every existing share they hold. The explicitly stated purpose for this substantial fundraising effort is to secure crucial facility investment capital for its subsidiary, Kyung Dong Polium.

This isn’t merely a financial transaction; it’s a strategic pivot. The allocation of funds to Kyung Dong Polium suggests a deliberate strategy to bolster a key part of their supply chain or venture into higher-margin, specialized materials, thereby fortifying their competitive moat.

Company Fundamentals: The ‘Why’ Behind the Move

A Story of Growth and Profitability Pressures

KYUNG DONG NAVIEN’s recent performance paints a complex picture. The first half of 2025 saw impressive top-line growth, with consolidated sales reaching ₩757.45 billion—a 20.1% increase year-over-year. This surge was driven by strong overseas sales and the strategic acquisition of the SK Magic business unit. However, this growth came at a cost. Operating profit plummeted by 46.2% to ₩90.64 billion. This squeeze on profitability is a critical concern, stemming from a combination of rising raw material costs, higher administrative expenses, and the initial costs of new business investments. While the company’s debt ratio saw a slight improvement, an increasing net borrowing ratio signals a growing financial burden that this capital increase aims to address.

Balancing Positives and Negatives

- •Strengths: The company maintains a dominant position in the domestic boiler market, is successfully expanding globally, and holds advanced technology in eco-friendly products. Its acquisition of SK Magic and strong credit rating are significant assets.

- •Weaknesses: The sharp decline in operating profit is the most pressing issue. The company is also vulnerable to volatile raw material prices and foreign exchange rates. A potential slowdown in the construction sector and fierce competition represent external threats. For more on market dynamics, you can read our guide on navigating volatile industrial markets.

Potential Impacts on Investors and the Market

The Double-Edged Sword: Financial Health vs. Share Dilution

The infusion of ₩119.7 billion will undoubtedly strengthen KYUNG DONG NAVIEN’s balance sheet, likely lowering its debt-to-equity ratio and enhancing long-term financial stability. However, the high offering ratio of 1.33 new shares per existing one introduces the significant risk of share dilution. This means each existing share will represent a smaller percentage of ownership in the company, potentially decreasing earnings per share (EPS) in the short term. The ultimate impact will heavily depend on the final issue price of the new shares and the market’s reception.

Market Reaction and Long-Term Outlook

Historically, news of a capital increase can exert downward pressure on a company’s stock price. As noted by financial analysts at sources like Bloomberg, markets often react nervously to potential dilution. However, this initial pessimism can be overcome. If the funds from the KYUNG DONG NAVIEN capital increase are used efficiently and transparently, leading to tangible growth at Kyung Dong Polium and a subsequent boost in overall profitability, the long-term outlook for the stock could be very positive. The market will be watching closely to see if this facility investment translates into a sustainable competitive advantage.

Investor Action Plan & Key Monitoring Points

Given the conflicting factors, a ‘Neutral’ stance on KD Navien stock is prudent. The potential for long-term growth is balanced by short-term risks of dilution and ongoing profitability challenges. Investors should transition from a passive to an active monitoring mode.

Investors should closely monitor the following key metrics:

- •New Share Issuance Details: The final issue price and the subscription rate will be the first indicators of market sentiment.

- •Kyung Dong Polium Performance: Track quarterly reports for updates on the facility investment’s progress and its impact on revenue and margins.

- •Macroeconomic Factors: Keep an eye on raw material prices (especially steel and copper) and currency exchange rates (KRW/USD), as these directly affect the company’s cost structure.

- •Profitability Metrics: Most importantly, watch for a turnaround in operating profit margins. A sustained improvement will signal that the growth strategy is succeeding.

Disclaimer: This analysis is for informational purposes only and is based on publicly available data. Investment decisions should be made based on individual research and financial advice.