The latest SAMSUNG SDS Q3 2025 earnings report presents a complex picture for investors. While the company demonstrated impressive resilience in profitability, a noticeable slowdown in top-line revenue has raised important questions about its short-term trajectory. This comprehensive Samsung SDS financial analysis unpacks the key figures, explores the strategic drivers behind the numbers, and provides a forward-looking perspective on the company’s stock outlook amid a challenging global economy.

We’ll move beyond the surface-level data to examine the core factors influencing Samsung SDS performance, from the contraction in IT investments to the strategic pivot towards high-margin AI and Cloud services. Join us as we explore what these results mean for the future of SAMSUNG SDS.

SAMSUNG SDS Q3 2025 Earnings at a Glance

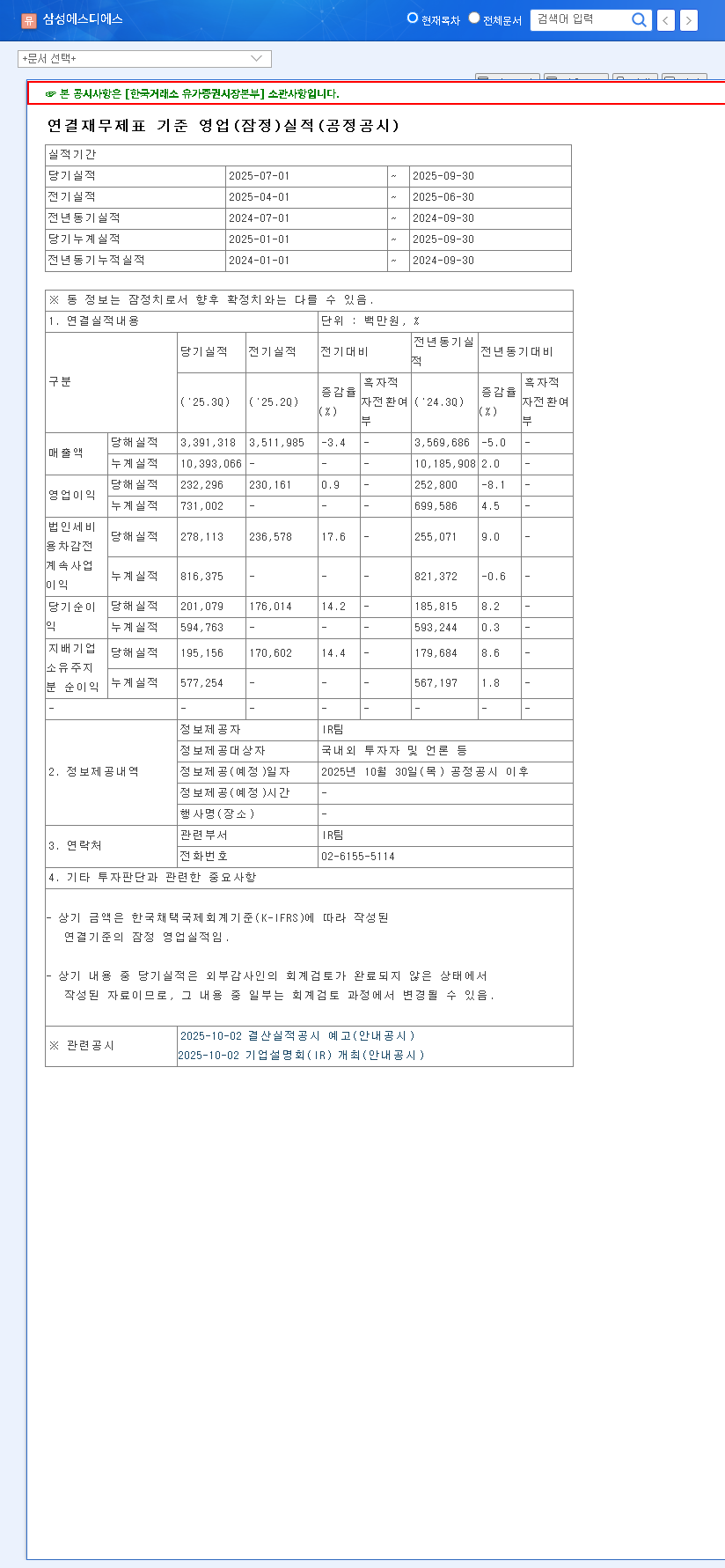

For the third quarter of 2025, SAMSUNG SDS reported consolidated financials that, while solid, slightly missed consensus expectations on the top line. According to the Official Disclosure filed with DART, the results were as follows:

- •Consolidated Revenue: KRW 3.3913 trillion (a 3.7% miss vs. market expectations).

- •Operating Profit: KRW 232.3 billion (a 1.6% miss vs. market expectations).

- •Net Profit: KRW 195.2 billion (largely in line with market expectations).

The key narrative from these figures is one of strategic trade-offs: sacrificing some top-line Samsung SDS revenue growth to protect and enhance profitability through a focus on higher-value services.

Decoding the Performance: Revenue Headwinds vs. Profit Stability

Factors Behind the Revenue Slowdown

The continuation of a revenue decline, marking a 4% year-over-year decrease, can be attributed to a convergence of factors impacting both of the company’s core segments:

- •IT Services Segment: A general contraction in corporate IT spending, influenced by macroeconomic uncertainty, likely led to delays in the execution and acquisition of large-scale projects. While demand for digital transformation remains, budget cycles have lengthened, impacting revenue recognition.

- •Logistics BPO Segment: This segment is highly sensitive to global economic conditions. A worldwide slowdown in trade and reduced freight volumes have directly pressured logistics revenue, a trend seen across the industry.

The Strategy Behind Strong Profitability

Despite the revenue challenges, the company’s ability to nearly meet operating profit expectations is a testament to its effective management and strategic focus. This resilience is built on two pillars:

- •High-Value Service Mix: SAMSUNG SDS is successfully increasing the proportion of revenue from high-margin areas. The growth of its Cloud services and AI-powered solutions, like the ‘FabriX’ platform, commands better pricing and contributes more significantly to the bottom line.

- •Disciplined Cost Management: Proactive cost-efficiency measures across the organization have helped offset the impact of lower revenues, ensuring that profitability remains robust and stable.

SAMSUNG SDS’s Q3 performance showcases a deliberate strategy: navigating market headwinds by prioritizing profitable growth in next-generation AI and Cloud services over sheer revenue volume.

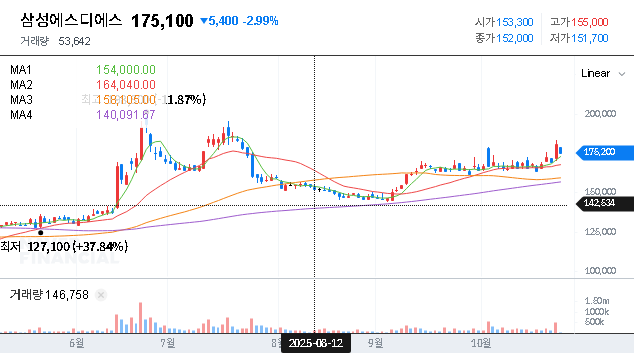

Investment Thesis: A Neutral Samsung SDS Stock Outlook

Considering the mixed signals from the SAMSUNG SDS Q3 2025 earnings, a neutral investment stance is prudent. The analysis reveals both compelling long-term drivers and significant short-term risks that investors must weigh.

The Bull Case: Long-Term Growth Engines

- •AI & Cloud Dominance: The structural shift towards cloud computing and AI integration is a powerful tailwind. Platforms like ‘FabriX’ position the company to capture high-value enterprise AI demand. You can read more in our deep dive into the AI industry.

- •Financial Fortress: A low debt-to-equity ratio and strong cash flow provide exceptional stability, allowing the company to invest in growth and weather economic downturns better than less-capitalized peers.

- •Samsung Group Synergy: Access to a steady stream of large-scale projects from Samsung affiliates provides a stable revenue base and a testing ground for new technologies.

The Bear Case: Short-Term Headwinds

- •Macroeconomic Pressure: Persistent inflation and high interest rates continue to suppress corporate IT budgets globally. As noted by sources like Reuters, economic uncertainty is a primary concern for enterprise spending.

- •Intensifying Competition: The markets for Cloud, SaaS, and AI services are fiercely competitive. Sustaining an edge requires continuous, heavy investment in R&D and innovation.

- •Logistics Market Volatility: The logistics segment’s performance is tied to global trade flows, which remain unpredictable due to geopolitical tensions and shifting supply chains.

Key Monitoring Points for Investors

Moving forward, investors should keep a close watch on several key indicators to gauge the Samsung SDS stock outlook. The company’s ability to re-accelerate revenue growth while maintaining its strong profit margins will be critical. Pay close attention to the pipeline for new IT projects, the adoption rate of its AI and Cloud services, and any signs of stabilization or recovery in the global logistics market. These factors will ultimately determine if the current headwinds are temporary or indicative of a more prolonged challenge.

Disclaimer: This report is for informational purposes only and is based on the preliminary earnings information provided. Investment decisions should be made based on your own research and consultation with a financial professional. The final responsibility for investment decisions rests solely with the investor.