What Happened?

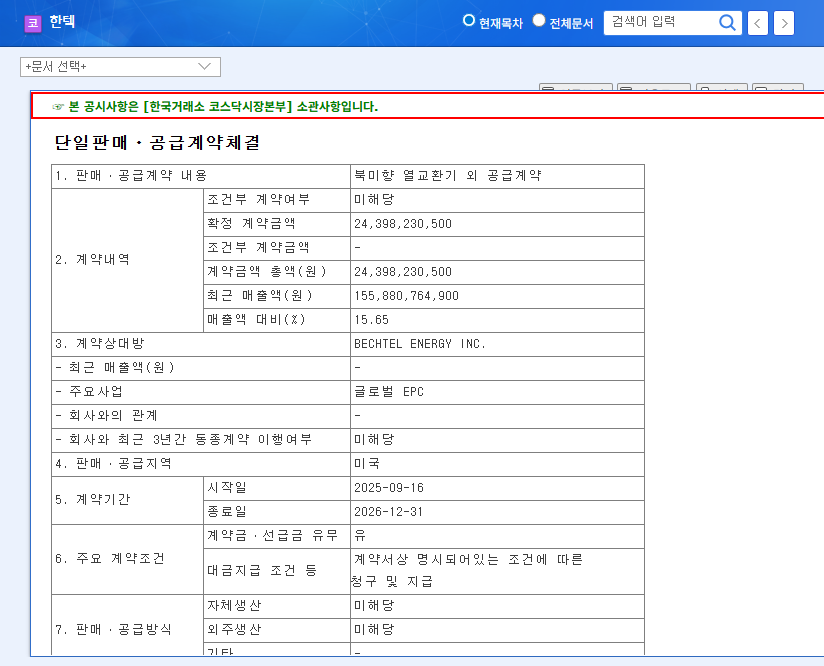

On September 17, 2025, Hantec signed a contract with Bechtel Energy Inc. to supply heat exchangers to North America, valued at $17.4 million. This represents a substantial 15.65% of Hantec’s projected 2025 annual revenue.

Why is it Important?

This contract signifies more than just increased revenue; it marks a significant step towards expanding Hantec’s presence in the overseas market, diversifying its business, and enhancing its corporate image. The partnership with a leading North American EPC company is expected to open doors for future large-scale contracts. Furthermore, it strengthens Hantec’s already robust fundamentals, with the company reporting strong growth in the first half of 2025, with revenue of KRW 83.055 billion (+5.5% YoY) and operating profit of KRW 20.306 billion (+21.1% YoY).

What’s Next?

This contract will directly contribute to revenue growth in the second half of 2025 and the first half of 2026, and is expected to improve profitability through the supply of high-value-added products. In the long term, expanding into overseas markets and diversifying its business will allow Hantec to establish a stable growth foundation. It is also expected to positively impact the growth of new business areas such as ammonia storage tanks and CCUS.

What Should Investors Do?

This contract is a significant indicator of Hantec’s growth potential. However, before making any investment decisions, investors should carefully consider potential risk factors such as fluctuations in exchange rates and raw material prices, as well as project execution risks. It is crucial to make informed investment decisions based on a comprehensive analysis of the company’s financials, market conditions, and competitive landscape.

FAQ

What is the value of this contract?

$17.4 million, representing 15.65% of Hantec’s projected 2025 annual revenue.

Who is the counterparty to the contract?

Bechtel Energy Inc., one of North America’s largest EPC companies.

Why is this contract important for Hantec?

It signifies not only revenue growth but also expansion into overseas markets, business diversification, and enhancement of the corporate image. It is also expected to positively impact future large-scale contract opportunities.

What should investors consider?

Investors should consider potential risks such as exchange rate and raw material price fluctuations, and project execution risks. A thorough analysis of the company’s financials, market conditions, and competitive landscape is crucial before making investment decisions.