The recent Exion Group convertible bond exercise (KRX: 069920) has sent ripples through the investment community. The company’s announcement to issue over 4 million new shares is a pivotal moment that warrants a closer look. This isn’t merely a financial transaction; it’s a strategic move that will directly influence Exion Group’s stock valuation, financial stability, and the trajectory of its ambitious growth plans.

For investors, this event presents both potential challenges, such as share dilution, and significant opportunities tied to the company’s future. This comprehensive analysis will unpack the direct and indirect impacts of the CB exercise, providing the critical insights needed to navigate this changing landscape and make informed decisions.

The Mechanics of the Convertible Bond Exercise

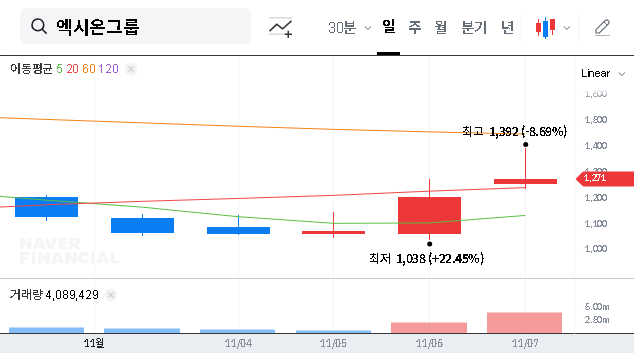

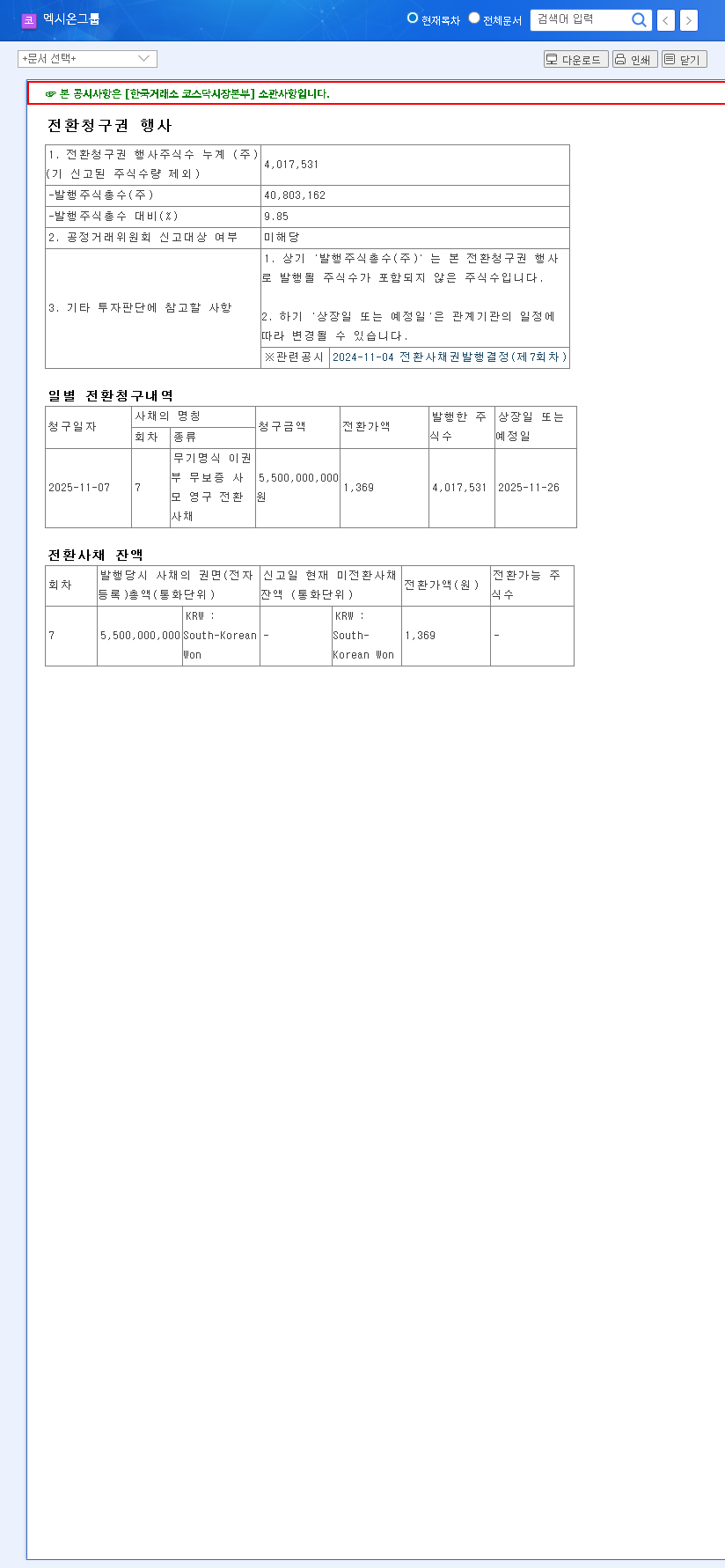

According to the company’s filing on November 7, 2025, a total of 4,017,531 shares will be newly listed, originating from the conversion of outstanding bonds. This represents a substantial 9.85% of the current market capitalization. The key figures to note are a conversion price of 1,369 KRW per share and a scheduled conversion date of November 26, 2025. You can view the Official Disclosure for complete details.

At the heart of this event is the conversion of debt into equity. Understanding this trade-off is crucial. While the market reacts to the influx of new shares, the company is simultaneously strengthening its balance sheet for the long term.

Direct Impact: Navigating Exion Group Share Dilution

1. Share Dilution and Investor Sentiment

The most immediate consequence of issuing nearly 4 million new shares is the dilution of existing stock. This increase in the total number of shares outstanding can lead to a decrease in Earnings Per Share (EPS), a key metric used to value a company. This can create a psychological overhang on the stock, as existing shareholders see their ownership percentage shrink. The current stock price of 1,271 KRW is below the conversion price of 1,369 KRW, which temporarily mitigates immediate selling pressure from converters seeking a quick profit.

2. Increased Market Float and Liquidity

Once converted, these new shares will enter the public market, increasing the stock’s float (the number of shares available for trading). In the short term, this could create selling pressure. However, over the long run, higher liquidity can be a positive factor, making it easier for investors to buy and sell shares and potentially attracting larger institutional investors.

3. From Debt to Equity: A Healthier Balance Sheet

A significant, often overlooked, benefit of an Exion Group convertible bond exercise is the financial restructuring it entails. A convertible bond is essentially debt that can become stock. By converting, the company extinguishes debt from its balance sheet and increases its equity base. This reduces the debt-to-equity ratio, a key indicator of financial health, signaling greater stability to the market and reducing future interest payment burdens.

Indirect Impact: Fueling Future Growth

This capital event doesn’t happen in a vacuum. It is strategically tied to Exion Group’s aggressive diversification and growth initiatives. The capital raised and the improved financial flexibility are likely intended to fund key ventures that could redefine the company’s future revenue streams.

- •MJ Tech Acquisition: Bolstering their core technology and market position.

- •Sports Apparel Expansion: Tapping into new consumer markets with high growth potential.

- •Overseas Resource Development: Securing raw materials and expanding the company’s global footprint.

An Investor’s Strategic Checklist for Exion Group (069920)

Given the complexities of the Exion Group convertible bond exercise, investors should adopt a strategic, forward-looking approach. While short-term volatility is possible, the long-term thesis depends on the successful execution of the company’s strategy. For a deeper understanding, review our guide on how to analyze a company’s financial health. Consider these key factors:

- •Price vs. Conversion Point: Monitor if the stock price can sustainably rise above the 1,369 KRW conversion price, as this will influence the behavior of bondholders.

- •Execution on New Ventures: Look for tangible results and revenue growth from the new business segments. Are they meeting milestones and contributing to the bottom line?

- •Financial Discipline: Track the company’s efforts to manage its debt levels and improve profitability metrics post-conversion.

- •Macro-Economic Headwinds: Keep an eye on interest rates, currency fluctuations, and commodity prices, which can all impact Exion Group’s diverse operations.

In conclusion, this event is a crucial turning point. By balancing an understanding of short-term Exion Group share dilution with an appreciation for the long-term strategic goals, investors can make wiser, more confident decisions.