The recent announcement of the Execure Hydron (019490) rights issue, coupled with a significant change in its major shareholder, has sent ripples through the investment community. This isn’t merely a financial maneuver; it represents a pivotal moment that could redefine the company’s future. For investors, this raises a critical question: is this a turnaround opportunity or a signal of deeper instability? This comprehensive guide will dissect the situation, providing a clear-eyed analysis to help you navigate this complex landscape.

We’ll explore the background of this strategic shift, weigh the potential upsides against the considerable risks, and offer an actionable plan for investors considering their position in Execure Hydron stock.

The Catalyst: Shareholder Change and Capital Injection

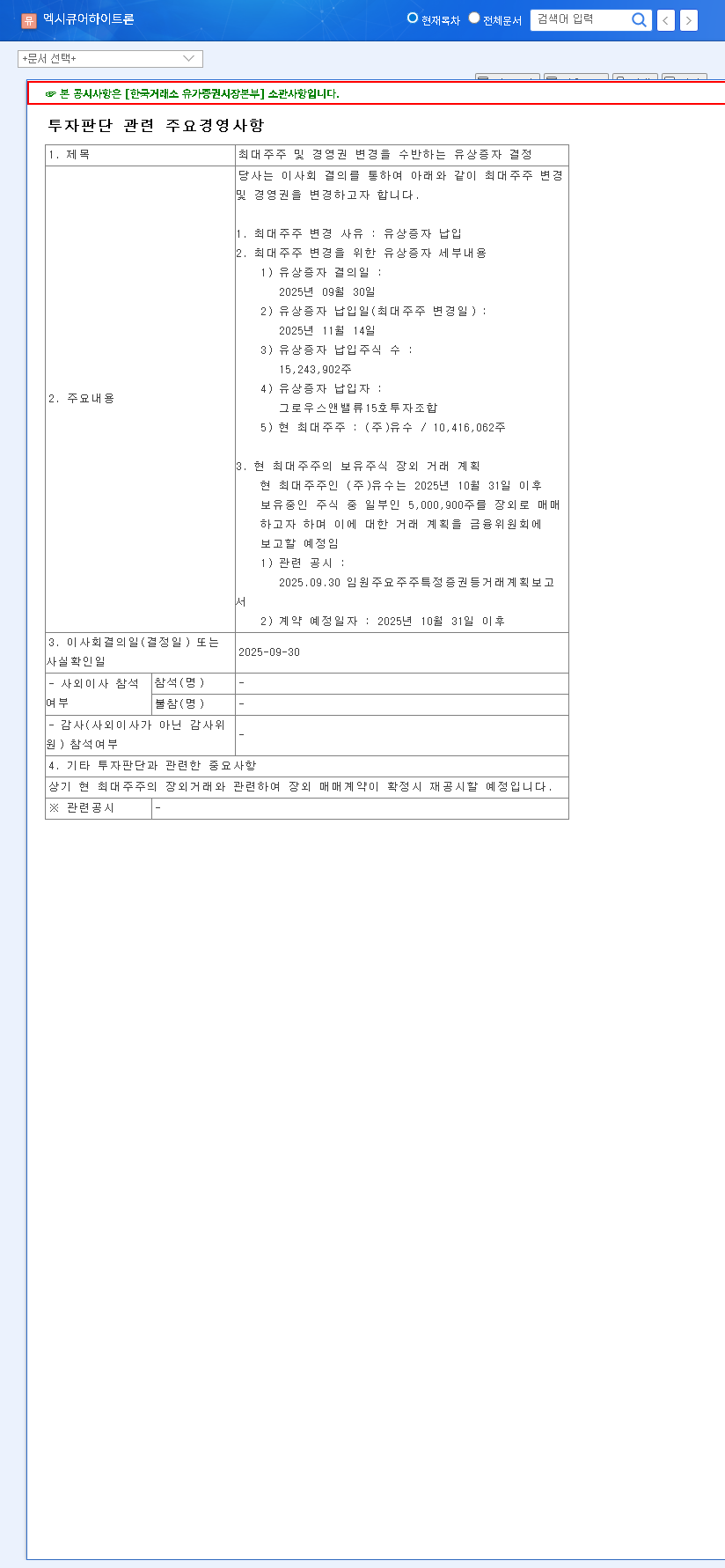

Understanding the Execure Hydron 019490 Rights Issue

On September 30, 2025, Execure Hydron’s board made a decisive move, resolving to undertake a large-scale rights issue. This process, scheduled for payment on November 14, 2025, will see the issuance of 15,243,902 new shares. The core purpose of this action is to facilitate the entry of a new major shareholder, the ‘Growth & Value No. 15 Investment Association’, effectively transferring management control from the incumbent, Yusu Co., Ltd. For official details on this resolution, investors can refer to the Official Disclosure on DART. This is a critical development for anyone conducting an 019490 analysis, as it signals a complete strategic overhaul.

A rights issue is a corporate action where a company offers existing shareholders the right to buy additional new shares, often at a discount to the market price. It’s a method to raise capital without diluting the ownership stake of shareholders who choose to participate. For a deeper understanding, you can read more about the mechanics on high-authority sites like Investopedia.

The Bull Case: Potential for a New Beginning

Proponents of this change point to several potential positive outcomes that could steer the company toward recovery and growth.

- •Drastically Improved Financial Structure: The capital injection is a direct antidote to the company’s financial woes. It’s expected to pay down debt, reduce a dangerously high debt-to-equity ratio, and clean up a balance sheet burdened by accumulated deficits. This financial stabilization is the first step toward sustainable operations.

- •New Leadership, New Vision: The Execure Hydron shareholder change brings in a fresh management team. This could finally resolve the long-standing operational inefficiencies and lack of strategic direction that plagued the previous leadership. A new, accountable management system could unlock significant value.

- •Fuel for Future Growth: The newly raised funds are not just for debt service. They are earmarked for strategic investments, potentially in high-growth areas like the biotech sector, expanded R&D initiatives, and securing working capital to ensure smooth day-to-day operations.

The Bear Case: Unignorable Risks and Uncertainties

However, a cautious investor must scrutinize the significant risks that loom over this transition. Past performance and current financial fragility cannot be overlooked.

- •Execution Risk and Management Uncertainty: The new management team is an unknown quantity. Their vision, strategy, and ability to execute are unproven. This introduces a period of short-term uncertainty that could lead to strategic missteps.

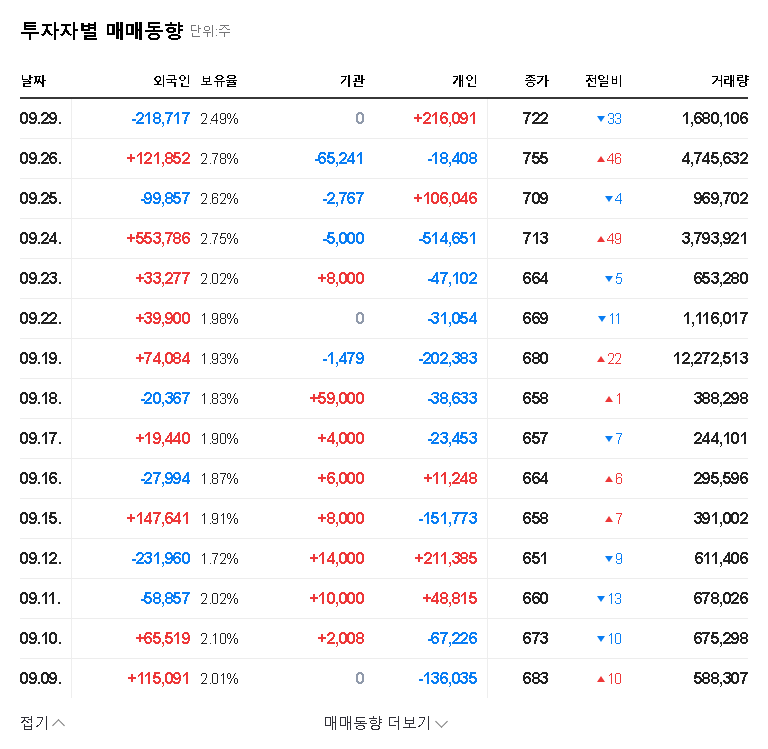

- •Stock Overhang and Price Pressure: The outgoing major shareholder, Yusu Co., Ltd., has signaled its intent to sell a portion of its holdings. This ‘stock overhang’ could create significant downward pressure on the Execure Hydron stock price in the near term.

- •Persistent Financial Weakness: Despite some revenue growth, the company’s core financial health is precarious. An operating loss exceeding KRW 10 billion in H1 2025, coupled with rising administrative and financial costs, shows that the path to profitability is steep.

- •Ongoing Legal Battles: The company is entangled in multiple lawsuits and faces asset seizures. These legal risks represent potential financial liabilities and operational disruptions that are difficult to quantify.

Investor Guide: A Strategy of Cautious Observation

Given the balance of potential and peril, the current investment thesis for Execure Hydron is one of ‘Cautious Observation.’ A premature investment could be speculative and risky. Instead, a prudent approach involves monitoring key developments over the next one to three months. For more on this strategy, see our guide to analyzing corporate turnarounds.

Key Milestones to Watch:

- •New Management’s 100-Day Plan: Look for a clear, concrete business plan from the ‘Growth & Value No. 15 Investment Association’. Vague promises are a red flag.

- •Successful Rights Issue Completion: Verify that the payment for the rights issue is completed on schedule, confirming the capital injection.

- •Q4 2025 Financial Report: Scrutinize the next quarterly report for tangible improvements in key financial indicators—specifically, debt reduction, margin improvement, and cash flow stabilization.

- •Legal Risk Resolution: Monitor news for any progress or resolution in the company’s outstanding lawsuits.

In conclusion, the Execure Hydron (019490) rights issue and leadership change have placed the company at a critical crossroads. While the potential for a successful turnaround exists, the path is fraught with significant risks. The coming months will be telling, and only by observing these key milestones can investors make a truly informed decision.