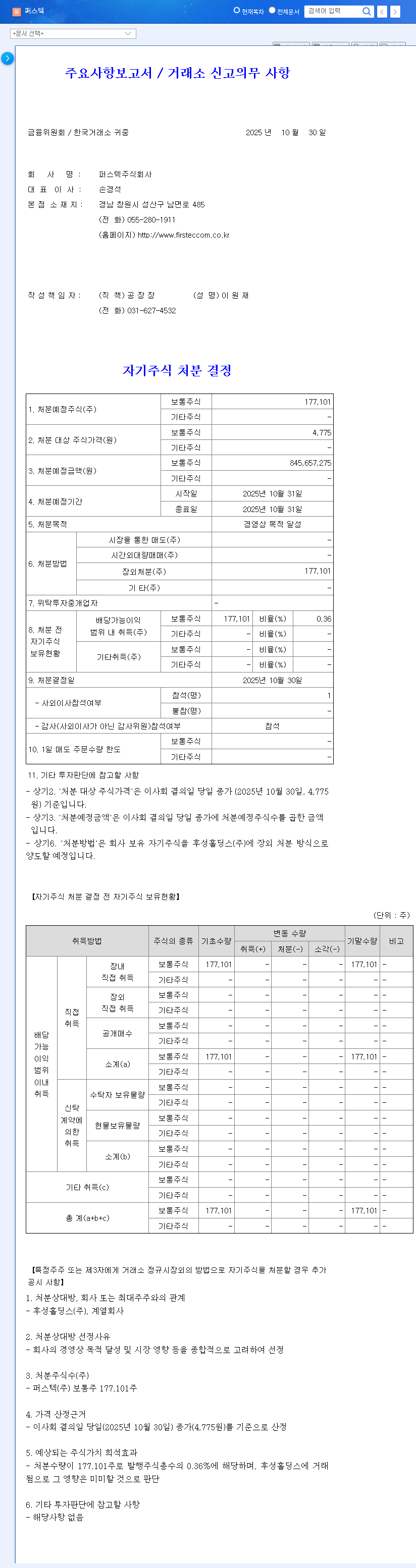

The recent FIRSTEC treasury share disposal has sent ripples through the investment community. On October 30, 2025, the prominent defense company announced its decision to sell 177,101 treasury shares, valued at approximately ₩800 million, for stated “management objectives.” While the amount seems modest, this move warrants a much deeper look. Is this a strategic maneuver to fuel future growth, or a warning sign of underlying financial strain?

This comprehensive analysis goes beyond the headlines to dissect the opportunities and risks facing FIRSTEC investors. We will evaluate the company’s robust position in the booming defense sector against a backdrop of concerning financial indicators and volatile macroeconomic conditions. For anyone considering an investment in FIRSTEC stock, this breakdown is essential reading.

Deconstructing the Treasury Share Disposal Announcement

According to the Official Disclosure filed with DART, FIRSTEC’s disposal represents approximately 0.36% of its total market capitalization of ₩232.9 billion. In isolation, a sale of this size is unlikely to cause significant short-term stock price dilution. However, seasoned investors know that the true story lies not in the amount, but in the motivation. The vague purpose of “achieving management objectives” requires us to analyze the company’s current financial health to infer the likely use of these funds.

The Bull Case: Growth Fueled by a Booming Defense Sector

Record-Breaking Order Backlog

FIRSTEC’s primary strength is its dominant position within the global defense industry. The company reported a staggering order backlog of ₩1.0346 trillion, providing a clear and positive roadmap for future revenue. With sales in the second quarter of its 51st fiscal year already up 24.2% year-over-year to ₩115.4 billion, the growth trajectory is undeniable. Rising geopolitical tensions globally continue to drive defense spending, creating a favorable tailwind for the entire sector, as reported by leading financial outlets like Reuters.

Strategic Use of Capital

From an optimistic perspective, the funds from the treasury share disposal could be a strategic investment in the future. The capital could be allocated towards M&A activities, securing new technologies, or acquiring top-tier talent. If deployed effectively, this ₩800 million could act as a catalyst for securing next-generation growth drivers, ultimately enhancing long-term shareholder value.

The Bear Case: Unpacking FIRSTEC’s Financial Risks

Despite the impressive top-line growth, a closer look at FIRSTEC’s financials reveals several potential red flags that could make the FIRSTEC treasury share disposal seem less strategic and more necessary.

The most alarming metric is the operating cash flow, which registered a negative ₩6.6 billion. This indicates that despite growing sales, the company’s core operations are currently consuming more cash than they generate.

Key Financial Pressures to Monitor:

- •Deteriorating Cash Flow: As noted, the operating cash flow was -₩6.6 billion in the second quarter, a significant deterioration caused by changes in working capital. This can signal issues with collecting receivables or managing payables effectively.

- •Bloating Inventory: Inventory assets surged from ₩71.5 billion to ₩99.7 billion. While some increase is expected with higher sales, a rapid rise can tie up capital and increase the risk of future write-downs, further straining cash flow.

- •Exchange Rate Sensitivity: With significant international business, FIRSTEC is exposed to currency fluctuations. A 10% change in the KRW/USD exchange rate could impact pre-tax profit by approximately ₩1.53 billion, a material risk in a volatile forex market.

- •Profitability Squeeze: Despite higher sales, operating profit fell year-over-year to ₩2.9 billion. This suggests that rising costs, including a 52% increase in R&D spending, are pressuring profit margins.

Investor Action Plan: Navigating Your FIRSTEC Strategy

The FIRSTEC stock analysis presents a duality: a high-growth company in a strong sector facing significant internal financial pressures. The treasury share disposal sits at the crossroads of these two narratives. Prudent investors should take a wait-and-see approach, focusing on the following key areas:

- •Demand Clarity on Fund Usage: Watch for subsequent announcements that specify how the ₩800 million will be used. Transparency is paramount. A clear, strategic plan is a bullish signal; silence or vague justifications are bearish.

- •Monitor Key Financial Metrics: Pay close attention to the next quarterly report. Look for improvements in operating cash flow, a stabilization of inventory levels, and margin recovery.

- •Analyze Broader Sector Trends: Continue to evaluate the health of the global defense market. For more on this, see our complete guide to investing in defense stocks. As long as the sector remains strong, FIRSTEC has a powerful current to swim with.

- •Observe Market Sentiment: Track how institutional investors and analysts react. Their response can provide clues about how the ‘smart money’ is interpreting this disposal.

Frequently Asked Questions (FAQ)

Q1: What is the primary reason for the FIRSTEC treasury share disposal?

A: The company officially stated the reason is to achieve ‘management objectives.’ However, given the negative operating cash flow and rising inventory, it could also be interpreted as a way to bolster its cash position to fund operations and R&D.

Q2: How will this disposal impact FIRSTEC’s stock price?

A: The direct impact from dilution should be minimal due to the small size (0.36% of market cap). The long-term impact depends entirely on how effectively the capital is used and whether the company can resolve its underlying financial challenges.

Q3: What are the biggest financial risks for FIRSTEC right now?

A: The key risks are the negative operating cash flow (-₩6.6 billion), a sharp increase in inventory assets, pressure on operating profit margins, and sensitivity to foreign exchange rate fluctuations.