The latest Ajin Electronic Components earnings for Q3 2025 have been released, and investors are closely scrutinizing the numbers. As a pivotal supplier in the burgeoning electric vehicle (EV) sector, Ajin Electronic Components (KRX: 009320) has been on a promising turnaround trajectory. But does this quarter’s performance sustain that momentum, or does it signal a need for caution?

This comprehensive analysis offers a deep dive into the company’s financial health, its core growth engine in the EV component market, the macroeconomic headwinds and tailwinds it faces, and a forward-looking investment strategy. We will unpack the key figures and what they mean for the future of Ajin’s stock.

Ajin Electronic Components Q3 2025 Earnings: A Closer Look

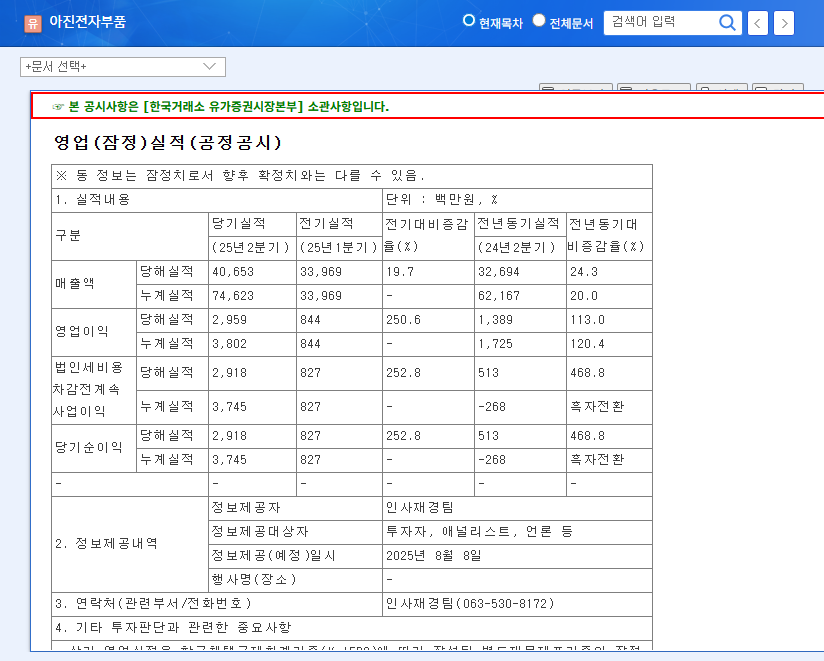

Ajin Electronic Components announced its preliminary Q3 2025 earnings, revealing a mixed but insightful picture of its current standing. The full details can be reviewed in the company’s Official Disclosure (DART). Here are the headline figures:

- •Revenue: KRW 41.7 billion (a slight increase quarter-over-quarter and an improvement year-over-year).

- •Operating Profit: KRW 2.0 billion (a decrease quarter-over-quarter, but an improvement year-over-year).

- •Net Profit: KRW 1.7 billion (a decrease quarter-over-quarter, but an improvement year-over-year).

While the year-over-year growth is a positive sign of long-term recovery, the sequential decline in both operating and net profit raises questions. This suggests that while the company’s top line is stable, cost pressures or a shift in product mix might be impacting profitability.

The Q3 results indicate a temporary pause in the company’s strong turnaround momentum seen in the first half of the year. The core challenge is balancing revenue growth with margin protection.

Unpacking the Performance: Growth vs. Risks

Core Strength: The EV Component Market

The driving force behind Ajin’s long-term potential remains its deep integration into the automotive electronics supply chain, which accounts for over 97% of its revenue. The company has successfully pivoted to capitalize on the global shift to electric vehicles. Its key growth products include:

- •PTC Heaters: Essential for efficiently heating the cabin of an EV without relying on a traditional combustion engine’s waste heat.

- •Battery Warming Heaters: Critical for maintaining optimal battery temperature in cold climates, which improves performance, range, and charging speed.

Its status as a primary supplier to Hyundai and Kia provides a stable revenue base and a direct line into one of the world’s fastest-growing EV manufacturing groups. This foundation is crucial as the global EV market continues its exponential growth, a trend confirmed by major market analysis firms.

Financial Health and Potential Headwinds

Despite the positive market trends, the Q3 profit dip and the company’s balance sheet warrant careful consideration. The most significant risk factor is its financial structure. With a debt-to-equity ratio of 230.87% as of H1 2025, the company is highly leveraged. This high debt level can lead to substantial interest expenses that erode net profit and limit flexibility for future investments or R&D.

Furthermore, external macroeconomic factors present a mixed bag. A rising USD/KRW exchange rate increases the cost of imported raw materials, directly squeezing profit margins. While stable oil prices and potential interest rate cuts offer some relief, currency volatility remains a key variable for investors to monitor in the coming quarters. To learn more, you can read our guide on how to analyze financial statements for tech companies.

Investment Strategy & Future Outlook

The Ajin investment strategy requires a balanced view of its short-term challenges against its long-term growth narrative.

- •Short-Term Outlook: The QoQ profit decline could exert downward pressure on the stock price. Investors may react cautiously until there is clarity on whether this is a one-off event or the beginning of a trend.

- •Mid-to-Long-Term Outlook: The company is undeniably well-positioned in the high-growth EV component market. However, a conservative approach is prudent. Key milestones to watch for are tangible progress in reducing the debt-to-equity ratio and successful commercialization of new products like ambient light controllers.

The upcoming Q4 2025 earnings report will be critical. It will help determine if the Q3 slowdown was an anomaly or if underlying cost pressures are becoming a more persistent issue. Continuous monitoring of the company’s efforts to deleverage its balance sheet is essential for any long-term investment thesis.

Frequently Asked Questions (FAQ)

Q1: What were the key takeaways from Ajin’s Q3 2025 earnings?

A1: Ajin reported stable revenue of KRW 41.7 billion, but operating profit (KRW 2.0B) and net profit (KRW 1.7B) declined compared to the previous quarter. This suggests a potential increase in costs or margin pressure, despite solid year-over-year improvement.

Q2: What is the main growth driver for Ajin Electronic Components?

A2: The primary growth driver is the strong demand for its automotive electronic components for EVs, such as PTC heaters and battery warmers. Its position as a key supplier for Hyundai/Kia solidifies its role in the expanding EV market.

Q3: What are the biggest risks for investors in Ajin stock?

A3: The two main risks are its high financial leverage, indicated by a debt-to-equity ratio over 230%, and its vulnerability to macroeconomic factors like fluctuating currency exchange rates, which can impact the cost of imported materials and overall profitability.