When a major global institution like Norges Bank adjusts its position in a company, it inevitably makes headlines. For investors in Hansol Chemical Co., Ltd., the recent news of a stake reduction has raised questions. Does this signal a problem, or is it merely market noise distracting from a powerful growth story? This analysis unpacks the situation, providing a comprehensive look at Hansol Chemical‘s exceptional performance, its strategic position in booming industries, and what the Norges Bank move truly signifies for your investment strategy.

We will explore how the company’s fundamentals, particularly in the EV battery materials sector, paint a picture of robust health and future potential that stands in stark contrast to the short-term interpretation of an institutional sale.

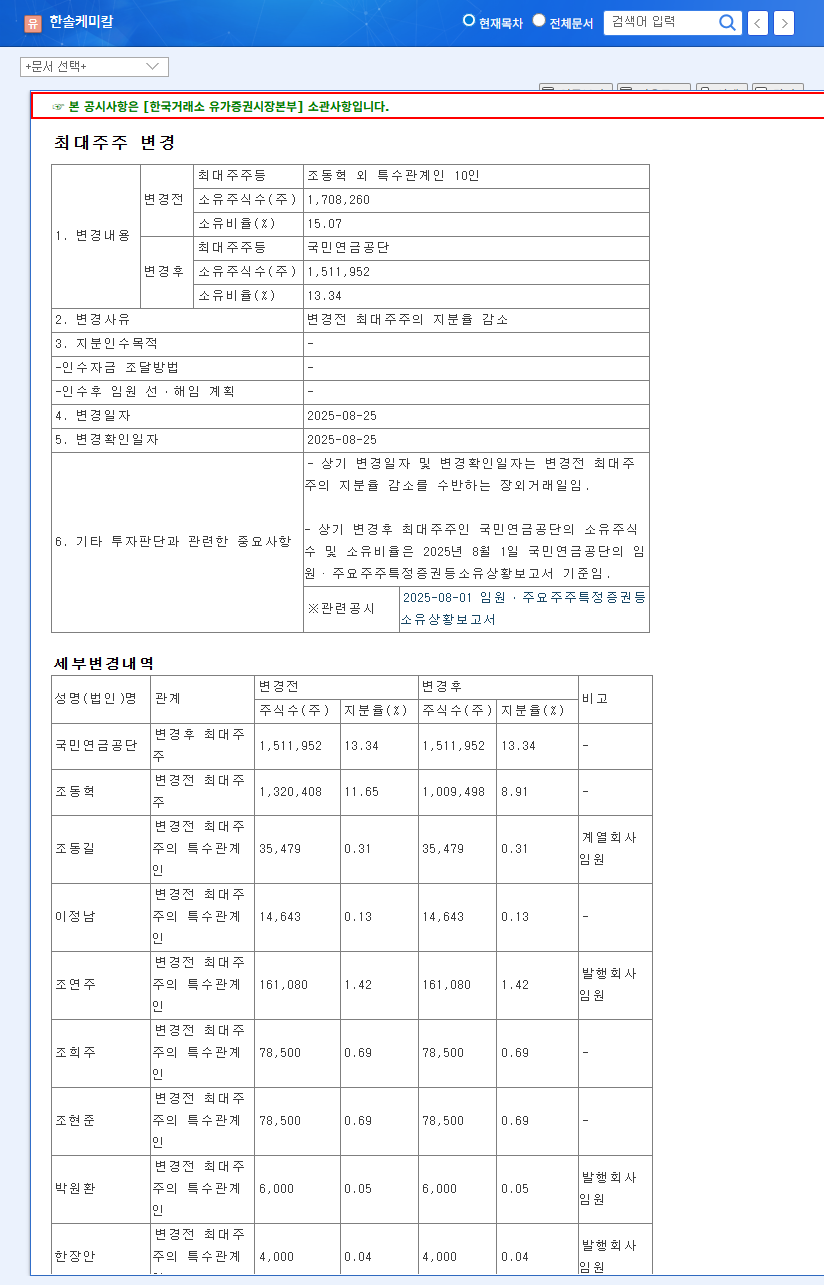

The Disclosure: Norges Bank’s Position Adjustment

According to the official disclosure filed, between October 22 and October 30, 2025, Norges Bank, Norway’s sovereign wealth fund, reduced its shareholding in Hansol Chemical from 6.05% to 4.93%. This 1.12 percentage point decrease was attributed to a ‘change in holdings for simple investment purposes.’ During this period, the fund’s net activity was skewed towards selling, with 36,775 shares sold versus 1,849 shares purchased. For complete transparency, you can view the Official Disclosure (DART Report) here. Movements from sovereign wealth funds like Norges Bank are closely monitored, but it’s crucial to analyze the context rather than react to the headline.

Beyond the Headlines: A Deep Dive into Hansol Chemical’s Fundamentals

While the market digests the news of the stake sale, Hansol Chemical‘s performance tells a different story. The first half of 2025 showcased remarkable financial strength and growth, underscoring the company’s solid operational execution.

An institution’s portfolio rebalancing is often a reflection of its own strategy, not necessarily a negative verdict on the underlying company’s value or future prospects.

Explosive Growth Driven by High-Tech Sectors

The company’s H1 2025 results were nothing short of impressive, with significant year-over-year gains:

- •Revenue: Increased by a solid 8.68%.

- •Operating Profit: Soared by an outstanding 31.24%.

- •Net Profit: Climbed by a healthy 23.28%.

The primary engine for this Hansol Chemical growth is the Electronic & EV Battery Materials division, which posted a remarkable 28.0% growth rate. This surge is directly tied to the global transition to electric vehicles (EVs) and the expanding need for advanced Energy Storage Systems (ESS). As a key supplier of next-generation lithium-ion battery materials, Hansol Chemical is perfectly positioned to capitalize on this multi-decade megatrend. For more on this sector, read our detailed analysis of the EV battery market.

A Fortress Balance Sheet and Shareholder-Friendly Policies

Financial stability is paramount, and Hansol Chemical excels here. The company maintains a very low debt-to-equity ratio of just 35.64%, indicating a stable financial structure that is resilient to economic shocks and rising interest rates. This financial prudence gives management the flexibility to invest in future growth and return value to shareholders. The recent initiation of share repurchases is a strong signal of confidence from the company’s leadership in its own stock and a clear commitment to enhancing shareholder value.

Investment Thesis: Why Hansol Chemical’s Story Remains Compelling

Considering all factors, the Norges Bank investment adjustment should be viewed as short-term market noise. The core investment thesis for Hansol Chemical stock is not only intact but strengthened by its recent performance. The company’s fundamentals are likely to easily offset the temporary supply-demand pressure from this event.

Our overall investment opinion remains Positive. Investors should focus on the mid-to-long-term picture, which is defined by fundamental improvements and powerful growth drivers.

Key Strengths to Consider:

- •Market Leadership: A critical supplier in the rapidly expanding EV battery and semiconductor supply chains.

- •Financial Excellence: Proven earnings power with soaring profits and a rock-solid balance sheet.

- •Shareholder Alignment: Proactive measures like share buybacks demonstrate a commitment to shareholder returns.

Potential Risk Factors:

- •Global Economy: A continued global economic slowdown or geopolitical risks could temper demand.

- •Cost Pressures: Volatility in raw material prices and logistics costs remains a factor to watch.

- •Competition: The EV battery and semiconductor material markets are competitive, requiring continuous innovation.

Frequently Asked Questions

Why did Norges Bank reduce its stake in Hansol Chemical?

The officially stated reason was for ‘simple investment purposes.’ This typically points to internal portfolio management decisions, such as rebalancing asset allocation or taking profits, rather than a negative view on Hansol Chemical‘s fundamentals.

How strong were Hansol Chemical’s recent earnings?

In the first half of 2025, the company reported exceptional results: revenue grew 8.68%, operating profit soared 31.24%, and net profit rose 23.28%, largely driven by a 28.0% growth in the EV battery materials division.

What is the likely impact on the Hansol Chemical stock price?

Short-term, the news could create minor selling pressure or negative sentiment. However, in the medium to long term, the company’s powerful earnings growth and positive outlook are expected to be the primary drivers of the Hansol Chemical stock value.