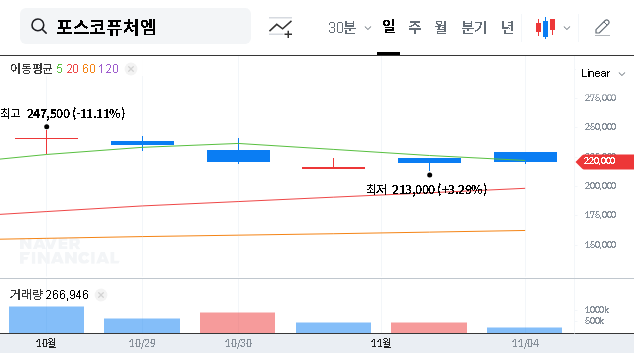

The sudden rights offering withdrawal by EV ADVANCED MATERIAL CO., LTD. (이브이첨단소재) on November 13, 2025, has sent shockwaves through the investment community. This move, far from a routine corporate decision, signals potential underlying financial distress and raises critical questions about the company’s stability and future prospects. Compounded by the looming threat of being designated an ‘unfaithful disclosure corporation,’ investors are left navigating a storm of uncertainty. This comprehensive financial analysis will dissect the reasons behind this decision, evaluate the company’s Q3 2025 performance, and provide a clear, data-driven investment outlook.

The company formally announced this decision, citing prolonged reviews by the Financial Supervisory Service (FSS), which could disrupt funding timelines. You can view the Official Disclosure (Source: DART) for complete details.

A Look Under the Hood: Q3 2025 Financial Red Flags

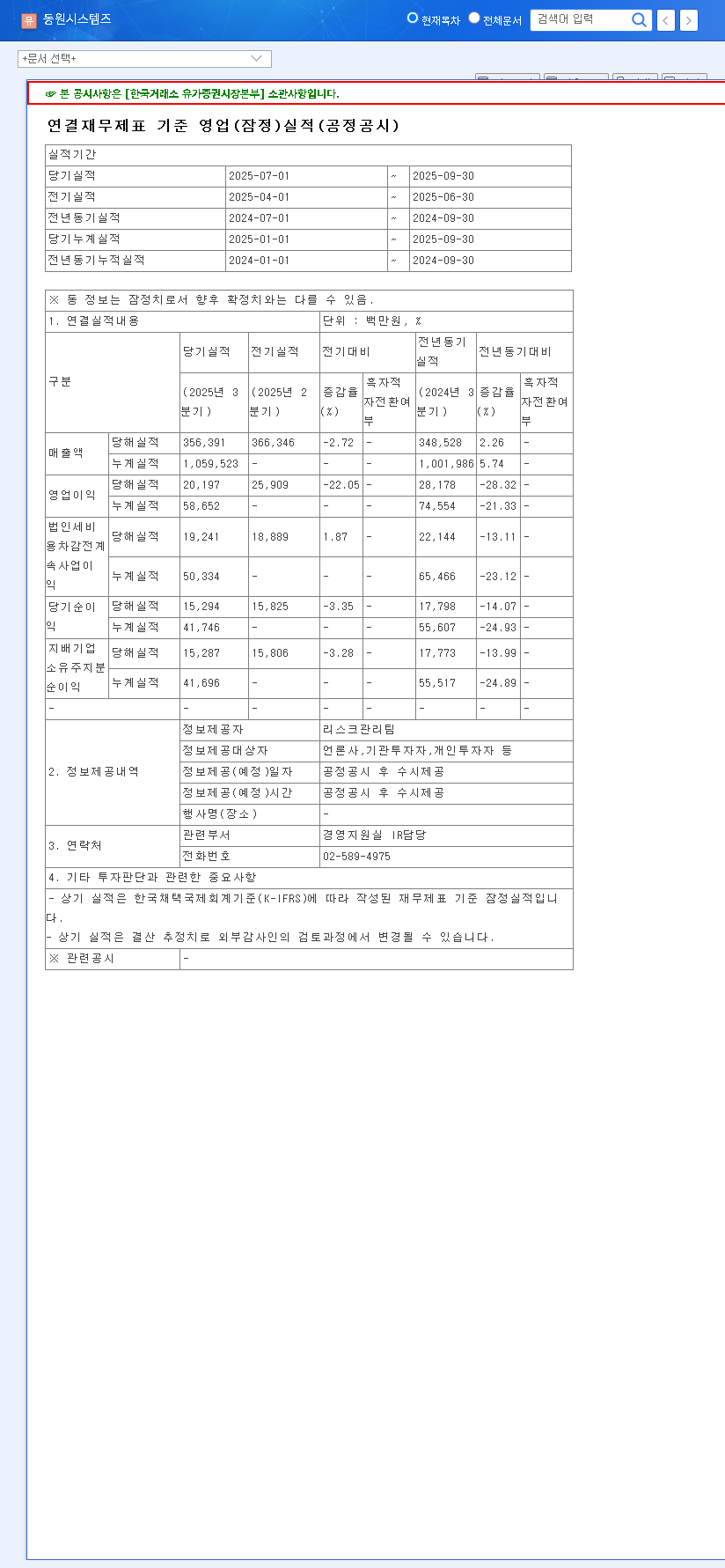

While procedural delays were the official reason, a deep dive into the Q3 2025 quarterly report for EV ADVANCED MATERIAL CO., LTD. reveals a much more troubling picture. The company’s fundamentals are flashing several warning signs that likely contributed to the difficulty in securing capital.

Deteriorating Core Financials

- •Revenue Decline & Profitability Collapse: Consolidated revenue fell year-over-year, while both operating profit and net income plunged into significant losses. This isn’t just a slowdown; it’s a severe erosion of the company’s core earning power.

- •Soaring Debt-to-Equity Ratio: Financial stability is a major concern. The company’s debt-to-equity ratio has climbed, indicating increased leverage and vulnerability to interest rate hikes and economic downturns. This high ratio makes securing new debt or equity financing significantly more challenging.

- •Underperformance in Key Segments: The FPCB (Flexible Printed Circuit Board) business, a primary revenue driver, experienced a notable decline in sales, suggesting a struggle to maintain market share or broader industry headwinds.

- •Costly Affiliate Investments: A substantial impairment loss related to its investment in Dynamic Design Co., Ltd. has placed an additional, heavy burden on the company’s already strained financial position.

While potential growth in the EV battery and transparent display markets exists, these future opportunities seem insufficient to counterbalance the immediate financial crisis and the severe damage to corporate credibility.

The Domino Effect: Repercussions of the Withdrawal

The cancellation of the rights offering is not an isolated event. It triggers a cascade of negative consequences that will impact EV ADVANCED MATERIAL CO., LTD. in both the short and long term, creating a challenging environment for recovery.

Funding Uncertainty and Eroding Trust

The most immediate impact is a critical disruption to funding. The capital was earmarked for facility investments, strategic acquisitions, and operational needs—all vital for growth. The failure to secure these funds puts future projects in jeopardy. This, combined with the ‘unfaithful disclosure’ designation, severely damages credibility. Investor trust is paramount, and once lost, it is incredibly difficult to regain, leading to sustained downward pressure on the stock price. For more on this topic, see our guide on How to Analyze High-Risk Tech Stocks.

Navigating Macroeconomic Headwinds

The company’s internal struggles are amplified by a challenging external environment. Rising interest rates in key markets increase the cost of borrowing, making alternative financing more expensive. Furthermore, volatility in currency exchange rates (EUR/KRW, USD/KRW) can negatively affect overseas operations and the cost of imported materials, squeezing already thin profit margins.

Investment Thesis: A Time for Extreme Caution

Considering the totality of the circumstances—the abrupt rights offering withdrawal, alarming Q3 financials, loss of investor confidence, and macroeconomic pressures—the outlook for EV ADVANCED MATERIAL CO., LTD. is precarious.

Investment Opinion: Highly Negative. Investment is not recommended at this time.

The risks associated with investing in the company currently are exceptionally high. A prudent strategy would be to remain on the sidelines and observe. Before any investment can be considered, the company must demonstrate tangible improvements in its financial health, provide a transparent and viable plan for future funding, and take concrete steps to rebuild its credibility with the market. Until these fundamental issues are resolved, the potential for further downside in the stock price remains significant.

Frequently Asked Questions

Why did EV ADVANCED MATERIAL CO., LTD. withdraw its rights offering?

The officially stated reason was potential disruptions in funding timelines due to a prolonged review process by the Financial Supervisory Service. However, our analysis suggests that the company’s poor Q3 2025 financial performance was a significant contributing factor.

What is the likely impact on the company’s stock price?

A rights offering withdrawal is a strong negative market signal. This, combined with the anticipated ‘unfaithful disclosure corporation’ designation, is highly likely to erode investor confidence and lead to sustained downward pressure on the stock price.

Should I invest in EV ADVANCED MATERIAL CO., LTD. now?

Our expert analysis concludes that investing at this time carries extremely high risk. It is advisable to refrain from new investments and observe the company’s progress in improving its financial health and restoring credibility before reassessing.