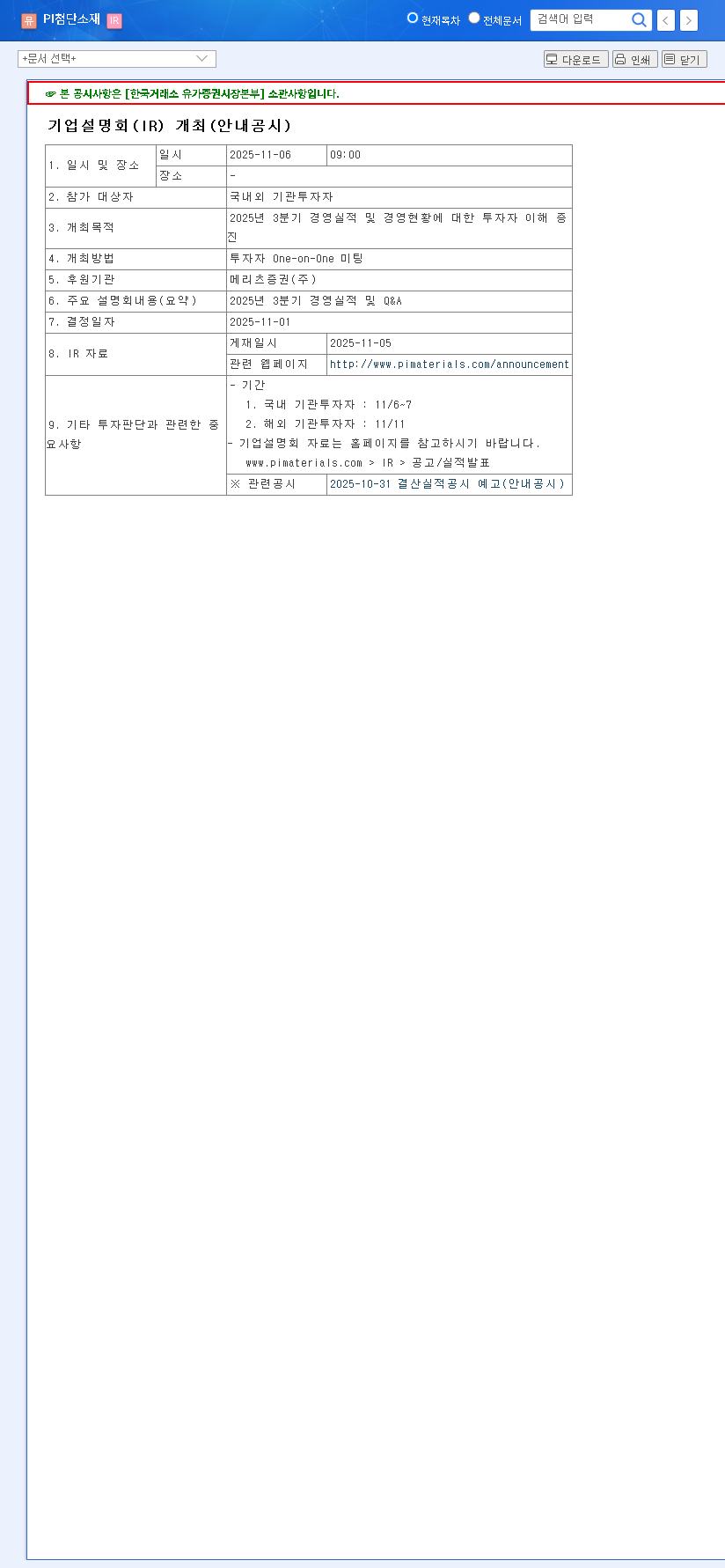

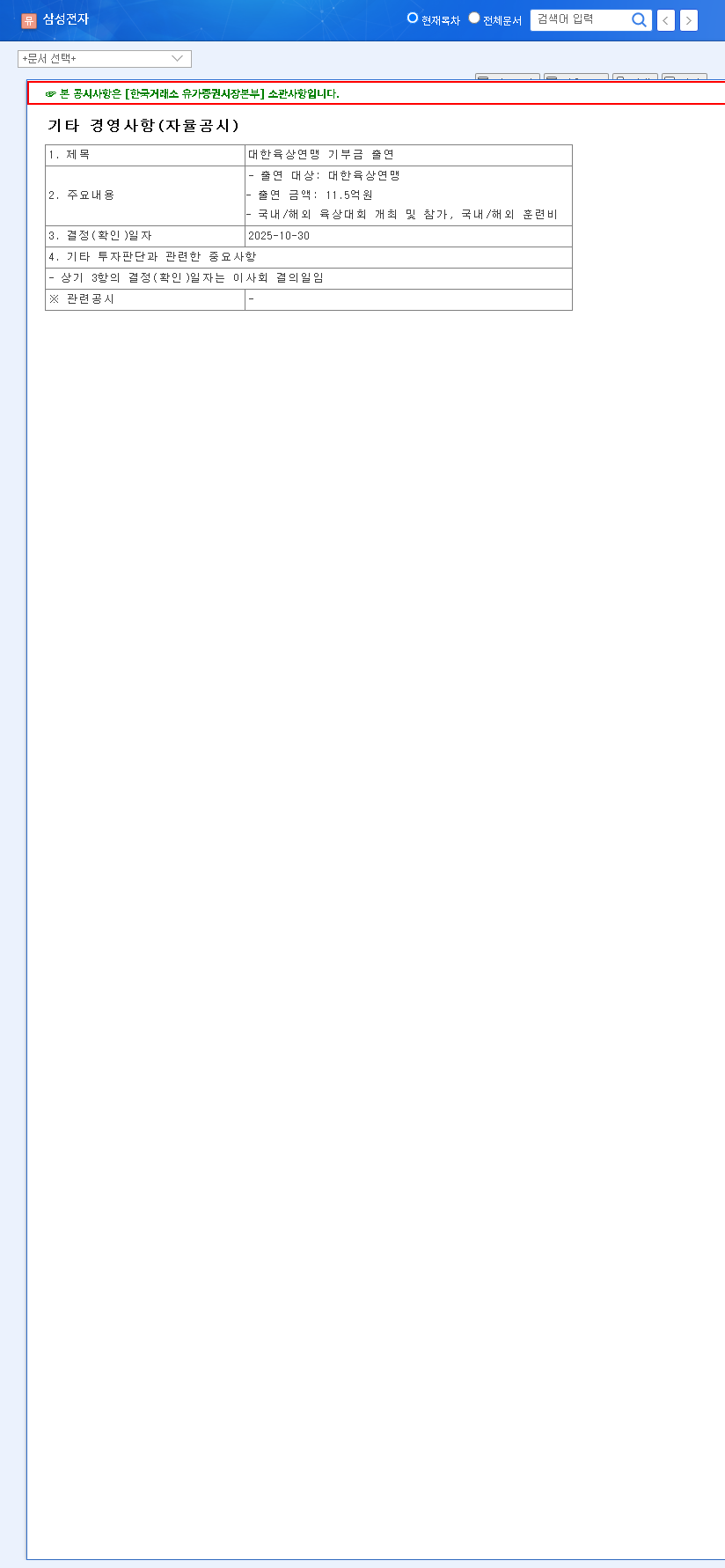

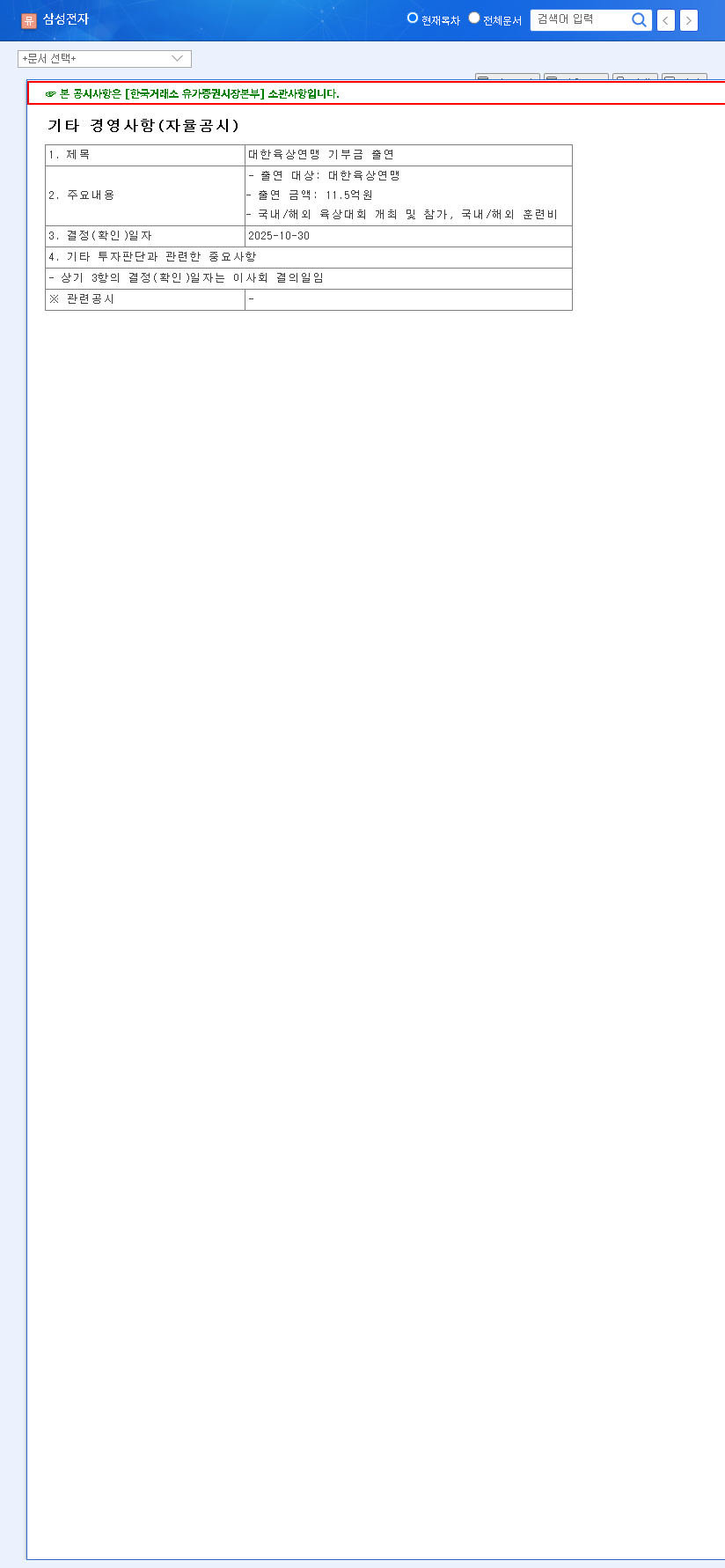

On November 6, 2025, the investment community will turn its attention to PI Advanced Materials Co., Ltd., the global leader in the polyimide (PI) film market. The company is hosting its highly anticipated Q3 2025 Earnings and Business Update Investor Relations (IR) conference. This pivotal PI Advanced Materials IR is far more than a simple financial report; it’s a strategic deep dive into the company’s performance, future growth trajectory, and response to a dynamic global landscape. For savvy investors, this event is a critical opportunity to gauge the health and potential of a key player in the high-tech materials sector.

This comprehensive analysis will dissect the company’s fundamentals, evaluate the current market environment, and outline what investors should watch for during the Q3 2025 earnings call. We will explore the strengths and potential risks facing the company to provide a clear framework for making informed PI Advanced Materials investment decisions.

Decoding the PI Advanced Materials IR: What’s at Stake?

The upcoming conference, scheduled for 9:00 AM KST on November 6, 2025, is a vital communication channel. It allows PI Advanced Materials to present its performance transparently and engage directly with stakeholders through a Q&A session. The market is particularly focused on the growth momentum of its core polyimide film business, which is essential for next-generation technologies. For complete transparency, investors can review the company’s official filing directly. Source: Official DART Disclosure.

In-Depth Fundamental Analysis: Strengths and Headwinds

A thorough review of the company’s position reveals several key factors that will shape its future. These are based on recent performance and market trends leading up to the Q3 2025 report.

Core Strengths & Positive Factors

- •Dominant Market Position: As the global leader in PI film sales, the company enjoys significant economies of scale and bargaining power with suppliers.

- •High-Growth End Markets: Demand for polyimide film is propelled by the expansion of Flexible Displays (OLEDs), Electric Vehicle (EV) batteries, and 5G telecommunications infrastructure, a trend confirmed by industry analysts at major financial publications.

- •Technological Leadership: A proprietary manufacturing process and a diverse portfolio of specialized PI films and varnishes create a strong competitive moat.

- •Improving Financial Health: While facing challenges, financial estimates for 2024 point towards a recovery in revenue and profitability, with an expected improvement in the debt-to-equity ratio.

Potential Risks & Investor Cautions

- •Macroeconomic Volatility: Fluctuations in the KRW/USD exchange rate can impact raw material costs, while a global economic slowdown could soften demand in key markets.

- •Intense Competition: The PI film market is competitive. Investors should monitor the strategies of key rivals and any potential for price pressure. You can read our deep dive on the global polyimide film market here.

- •Capital Expenditure Delays: Any further delays in the expansion of the PI Varnish production line could hinder the company’s ability to fully capitalize on the booming EV market.

- •R&D Investment Levels: A recent trend of decreasing R&D expenditure as a percentage of revenue may raise questions about the long-term innovation pipeline.

“The upcoming PI Advanced Materials IR is a moment of truth. While the company holds a formidable position in the PI film market, investors will be looking for concrete evidence of margin recovery and a clear strategy to navigate macroeconomic headwinds and accelerate growth in the EV sector.”

Key Questions for the IR & Investment Strategy

The impact of this IR on PI Advanced Materials’ stock will depend entirely on the substance of the presentation. Positive Q3 results that beat expectations, coupled with a confident outlook, could significantly boost investor sentiment. Conversely, missed targets or a cautious forecast could apply downward pressure.

Investors should adopt a proactive approach:

- •Analyze Profitability Metrics: Look beyond top-line revenue. Focus on operating profit margins and net profit trends to understand the company’s core profitability.

- •Question Future Growth Plans: Listen carefully for updates on the PI Varnish facility and strategies for penetrating deeper into the EV and 5G markets.

- •Evaluate Risk Management: What are the company’s strategies for mitigating currency risks and managing volatile raw material prices?

- •Maintain a Long-Term View: Base your PI Advanced Materials investment thesis on the long-term structural demand for polyimide film and the company’s enduring competitive advantages.

By preparing thoroughly and maintaining a critical, long-term perspective, investors can leverage the insights from the Q3 2025 IR to make strategic and successful investment decisions.

Frequently Asked Questions (FAQ)

When is the PI Advanced Materials Q3 2025 IR?

The Q3 2025 Earnings and Business Update IR conference will be held on November 6, 2025, at 9:00 AM KST.

What are the primary growth drivers for the company?

The main growth drivers are sustained demand for its core product, polyimide film, from rapidly expanding markets like Flexible Displays (OLED), Electric Vehicle (EV) batteries, and 5G technology.

What are the key risks for a PI Advanced Materials investment?

Investors should be aware of risks including foreign exchange rate volatility, fluctuations in raw material costs, intense market competition, and potential delays in strategic capital investments for new facilities.