This comprehensive KG Eco Solution stock analysis delves into the company’s (KRX: 151860) pivotal Q3 2025 earnings report and the forward-looking strategies that could reshape its future. While the latest financials revealed mixed results, the real story lies in the bold moves towards enhancing shareholder value and a significant strategic pivot into the high-growth KG Eco Solution bio marine fuel market. We will explore what these changes mean for investors, based on the company’s latest Official Disclosure (DART).

KG Eco Solution Q3 2025 Earnings Snapshot

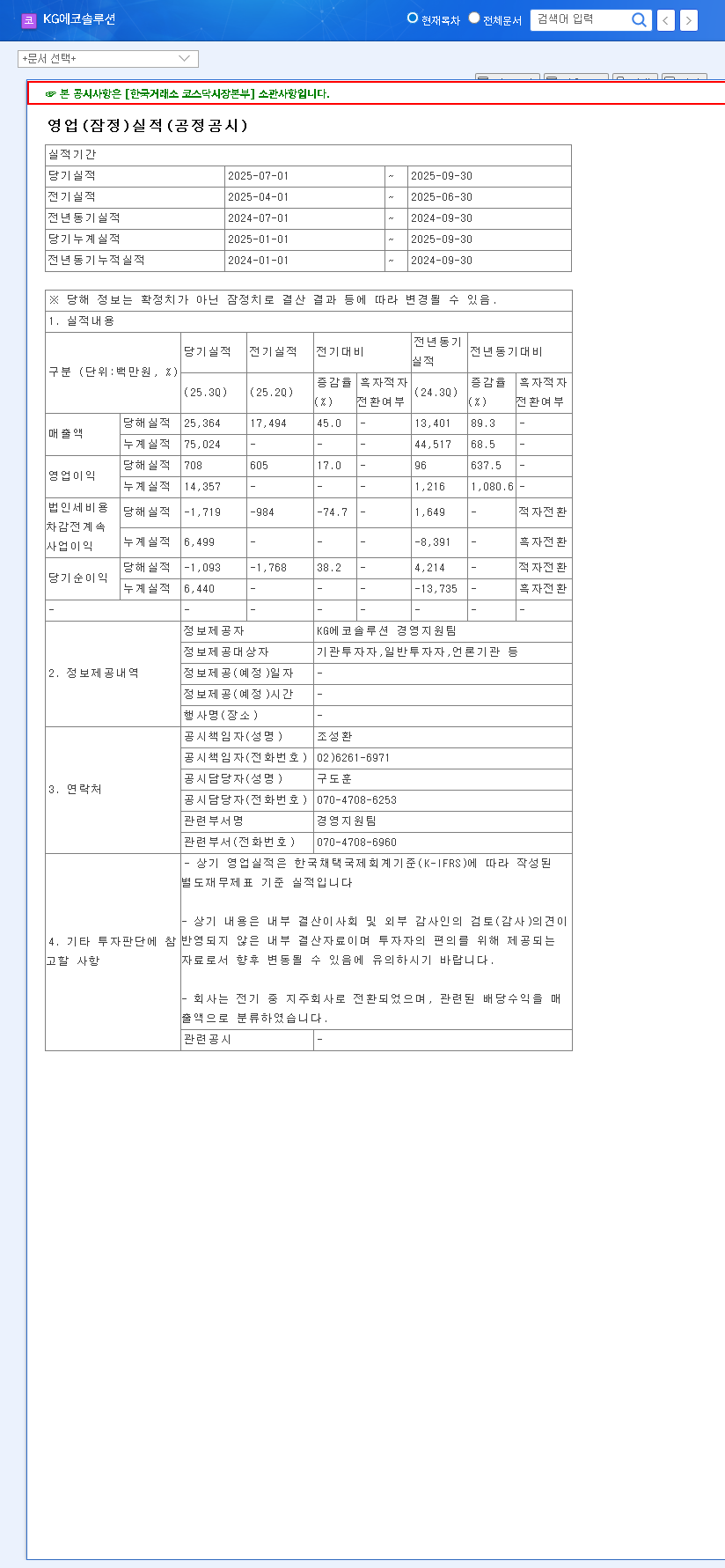

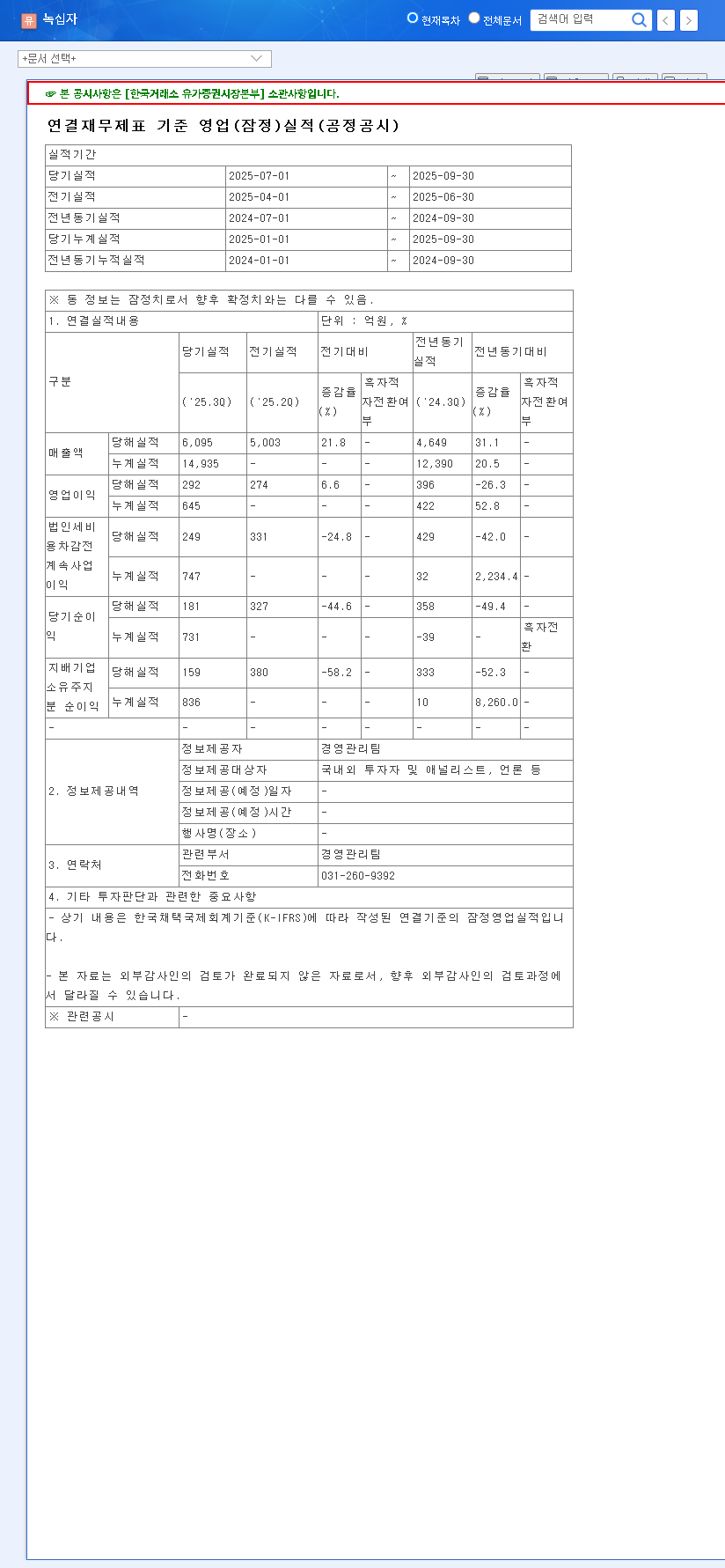

KG Eco Solution announced its preliminary consolidated operating results for the third quarter of 2025, painting a picture of steady top-line growth but underlying volatility in profitability. These figures are the foundation of our current KG Eco Solution stock analysis.

- •Revenue: KRW 207.32 billion, demonstrating a continued upward trend.

- •Operating Profit: KRW 58.8 billion, showing significant fluctuation compared to previous quarters.

- •Net Profit: KRW 14.5 billion, also reflecting market volatility.

The decline in the operating profit margin from its peak in Q1 2025 underscores a critical challenge: managing profitability amidst growth. This volatility is a key factor investors must consider, but it’s the company’s response that truly matters.

Beyond the quarterly numbers, KG Eco Solution is laying the groundwork for a fundamental corporate transformation aimed at sustainable, long-term growth and enhanced shareholder value.

Core Strategic Shifts Defining the Future

The earnings report was accompanied by announcements of several strategic initiatives designed to strengthen the company’s foundation and unlock new avenues for growth.

1. Boosting Shareholder Value Through Treasury Stock Management

KG Eco Solution is implementing a proactive shareholder return policy. By canceling 500,000 treasury shares and planning to cancel another 1.5 million, the company is reducing the number of outstanding shares. This action directly increases earnings per share (EPS), a key metric for investors. Furthermore, the plan to sell over 5.38 million treasury shares is a strategic move to secure substantial capital for funding its ambitious new ventures, including the KG Eco Solution bio marine fuel project.

2. Strategic Pivot: Entering the Bio Marine Fuel Market

Perhaps the most significant development is the amendment to the company’s Articles of Incorporation. KG Eco Solution is divesting from its automotive parts and secondary battery materials businesses to focus on the manufacturing and sales of bio marine fuel. This is a calculated response to tightening global environmental regulations, such as those from the International Maritime Organization (IMO), and the massive corporate push towards carbon neutrality. This venture positions the company directly in the path of the global green energy transition, presenting a massive growth opportunity.

3. Enhancing Governance and ESG Credentials

In a move to increase transparency and appeal to modern investors, the company is improving its corporate governance. By removing hostile M&A defense clauses and adding a holding company business structure, KG Eco Solution is streamlining operations and boosting transparency. These actions are likely to improve its ESG (Environmental, Social, and Governance) rating, which is an increasingly critical factor for institutional investors. You can learn more by reading our guide to ESG investing.

Investment Analysis: Potential vs. Risk

A thorough KG Eco Solution stock analysis must weigh the promising future against the existing challenges.

Positive Catalysts for Growth

- •Future-Proof Business Model: The entry into bio marine fuel aligns with a powerful global megatrend, offering a significant long-term growth engine.

- •Enhanced Shareholder Value: Treasury stock cancellations and improved dividend policies directly benefit shareholders and can attract long-term investment.

- •Increased Investor Confidence: Stronger governance and a commitment to ESG principles boost corporate transparency and build trust.

Key Risks to Monitor

- •Execution Risk: The success of the new bio marine fuel venture is not guaranteed. Investors must watch for tangible results and market penetration.

- •Profitability Concerns: The existing volatility in operating profit needs to be addressed. Sustainable profitability is key to long-term stock performance.

- •Macroeconomic Headwinds: Factors like international oil prices, shipping costs, and currency fluctuations can significantly impact the company’s bottom line.

Conclusion: An Investment for the Long Term

While the KG Eco Solution Q3 2025 earnings were mixed, the strategic initiatives announced are far more significant for a long-term investment thesis. The company is not just navigating the present; it is actively building a more resilient, transparent, and growth-oriented future. For investors, the key is to look beyond the short-term profit fluctuations and focus on the successful execution of its bio marine fuel strategy and its continued commitment to enhancing shareholder value. Continued monitoring of new business performance and macroeconomic factors will be essential in making an informed investment decision.