The recent activity surrounding the SECERN AI stock price has captured significant market attention, spurred by a major equity investment from DaeBo Information & Telecommunication. This development has investors posing a crucial question: Is this strategic move the catalyst SECERN AI Co., Ltd. (KOSDAQ: 340810) needs to navigate its challenging financial landscape and pivot towards sustainable growth? This in-depth analysis unpacks the official disclosure, scrutinizes the company’s fundamentals, and outlines a clear strategic outlook for current and potential investors considering a SECERN AI investment.

Decoding the DaeBo Investment in SECERN AI

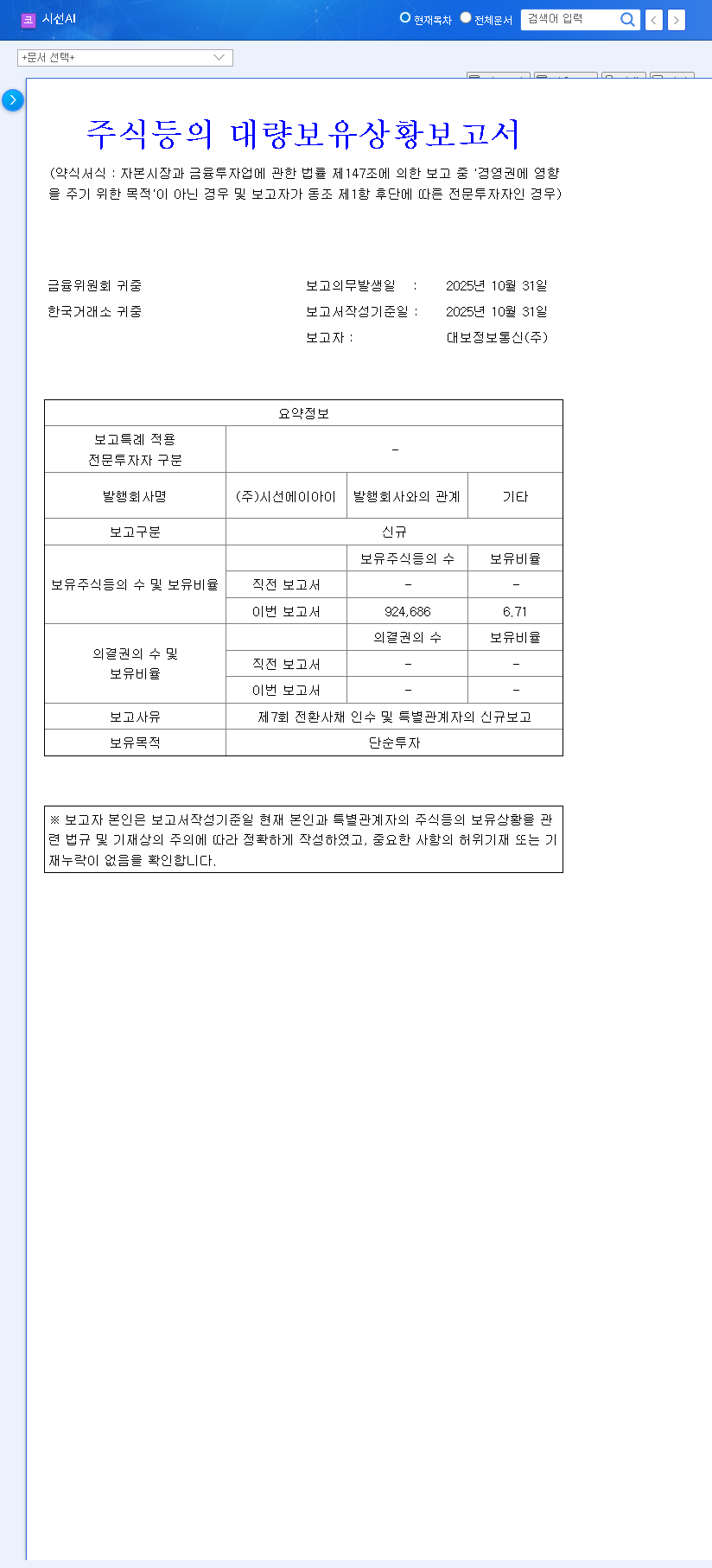

On November 7, 2025, a significant corporate filing revealed a strategic shift in the ownership structure of SECERN AI Co., Ltd. The announcement, detailed in the Report on Large Shareholding, outlines a multi-faceted investment led by DaeBo Information & Telecommunication. You can review the complete filing here: Official Disclosure (DART).

Key Details of the Transaction

The core of this development is the acquisition of SECERN AI’s 7th series of convertible bonds by DaeBo, coupled with open market share purchases by related parties. This coordinated effort has resulted in DaeBo and its affiliates securing a combined 6.71% stake in the company.

- •DaeBo Information & Telecommunication: Acquired 7th Convertible Bonds, equivalent to 822,368 potential shares upon conversion.

- •Kim Sang-wook (Related Party): Purchased 50,000 shares via the open market.

- •Choi Jae-hoon (Related Party): Purchased 52,318 shares via the open market.

The acquisition of convertible bonds is a particularly noteworthy event. It provides DaeBo with a future equity position, signaling a long-term strategic interest beyond a simple financial injection. For a deeper understanding of this financial instrument, you can explore our guide on how convertible bonds impact stock value.

A Hard Look at SECERN AI’s Financial Health

Before assessing the future impact, it is imperative to understand the fundamental ground on which SECERN AI currently stands. An analysis of its H1 2025 report reveals a company in transition, facing significant headwinds but also cultivating new areas of potential growth.

Despite the positive news of the SECERN AI investment, it’s crucial to acknowledge the underlying financial hurdles. The severe capital impairment and declining core revenue are significant risks that this new capital must address directly for long-term success.

Profitability and New Growth Engines

The company reported H1 2025 revenue of KRW 2.225 billion, a sharp 57.8% decrease year-over-year. This was largely driven by an 87% fall in its legacy AI facial recognition system revenue. However, a silver lining appeared in the AI facial authentication solution segment, which saw its revenue skyrocket by 574%, positioning it as a vital new growth driver. Furthermore, an improved order backlog of KRW 5.18 billion, particularly in the AI robot solution segment, suggests a pipeline of future revenue.

Financial Soundness Concerns

While total liabilities have decreased, the company’s balance sheet remains under pressure. A persistent and severe capital impairment, with retained earnings at a negative KRW 58.694 billion, is the most critical issue. This indicates that accumulated losses have eroded the company’s capital base, a situation that requires urgent and effective resolution. The worsening operating cash flow further underscores the need for both strategic redirection and financial stabilization.

Impact Analysis: What This Means for the SECERN AI Stock Price

Short-Term Outlook

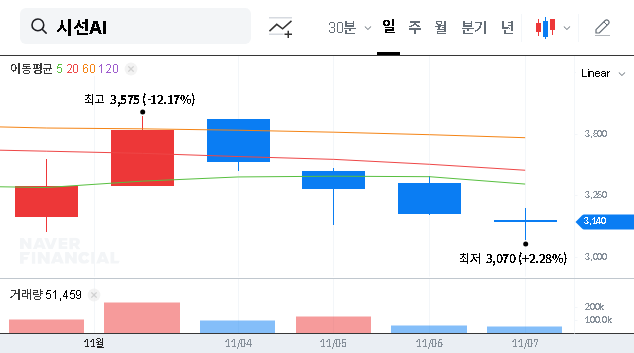

In the short term, the news is unequivocally positive for market sentiment. The involvement of a strategic investor like DaeBo, coupled with insider buying, enhances management confidence and can attract momentum traders. This often leads to increased trading volume and positive pressure on the SECERN AI stock price. However, investors should be wary of the potential for a ‘sell the news’ event if the rally is not supported by fundamental progress. According to market analysis from leading financial sources like Bloomberg, such event-driven rallies can be short-lived without a clear path to profitability.

Mid- to Long-Term Potential

The long-term trajectory depends entirely on execution. The key question is whether DaeBo will act as a passive financial investor or an active strategic partner. The potential for synergy is significant. DaeBo could provide access to new markets, operational expertise, and the stability needed for SECERN AI to focus on its new growth areas, such as AI-based medical solutions and robotics. The ultimate determinant of corporate value will be the tangible success of these new ventures and a concrete plan to resolve the capital impairment.

Investment Strategy and Recommendations

Given the dual nature of the situation—a positive catalyst against a backdrop of financial weakness—a nuanced investment approach is required.

- •For Short-Term Traders: The event provides clear momentum. A strategy based on technical analysis and volume trends could be viable, but it requires strict risk management and an awareness that the rally is speculative.

- •For Long-Term Investors: A ‘wait and see’ approach is prudent. An investment should only be considered after confirming tangible progress on key milestones. These include a visible path to resolving capital impairment, consistent revenue growth from new business segments, and clear evidence of strategic synergy with DaeBo.

Frequently Asked Questions

Q1: How will DaeBo’s investment affect SECERN AI’s stock price immediately?

A1: In the short term, it is likely to provide positive momentum due to increased market interest and the perception of a strategic turnaround. However, long-term valuation will depend on fundamental improvements, not just the initial news.

Q2: What are SECERN AI’s most promising growth drivers?

A2: The most promising areas are the AI facial authentication solution, which has already shown explosive revenue growth, and the emerging AI robot solution segment, which has a growing order backlog. Success in AI-based medical technology also represents a significant long-term opportunity.

Q3: What is the biggest risk for investors considering SECERN AI?

A3: The primary risk is the company’s severe capital impairment and weak underlying financials. Without a clear and successful plan to fix the balance sheet and generate consistent positive cash flow, any stock price gains from this investment may not be sustainable.

Q4: Will the convertible bonds dilute existing shareholders’ value?

A4: There is no immediate dilution. However, if and when DaeBo exercises its right to convert the bonds into stock, the total number of shares outstanding will increase. This would dilute the ownership percentage of existing shareholders. The conversion price and timing are key factors to monitor.