The latest GHOST STUDIO earnings report for Q3 2025 has captured the attention of the market, revealing a pivotal moment for the entertainment and content powerhouse. After a challenging first half of the year, the company has posted encouraging preliminary results that suggest a strategic turnaround is gaining traction. This deep-dive GHOST STUDIO investment analysis will dissect the numbers, explore the growth drivers fueling its media division, assess the persistent challenges in its gaming segment, and provide a clear outlook for current and prospective investors.

With ambitious ventures like Netflix original series and a strategic expansion into the K-beauty market, GHOST STUDIO is actively reshaping its business structure. We will examine whether these new growth engines are powerful enough to offset financial pressures and propel the GHOST STUDIO stock to new heights.

Decoding the GHOST STUDIO Q3 2025 Earnings Report

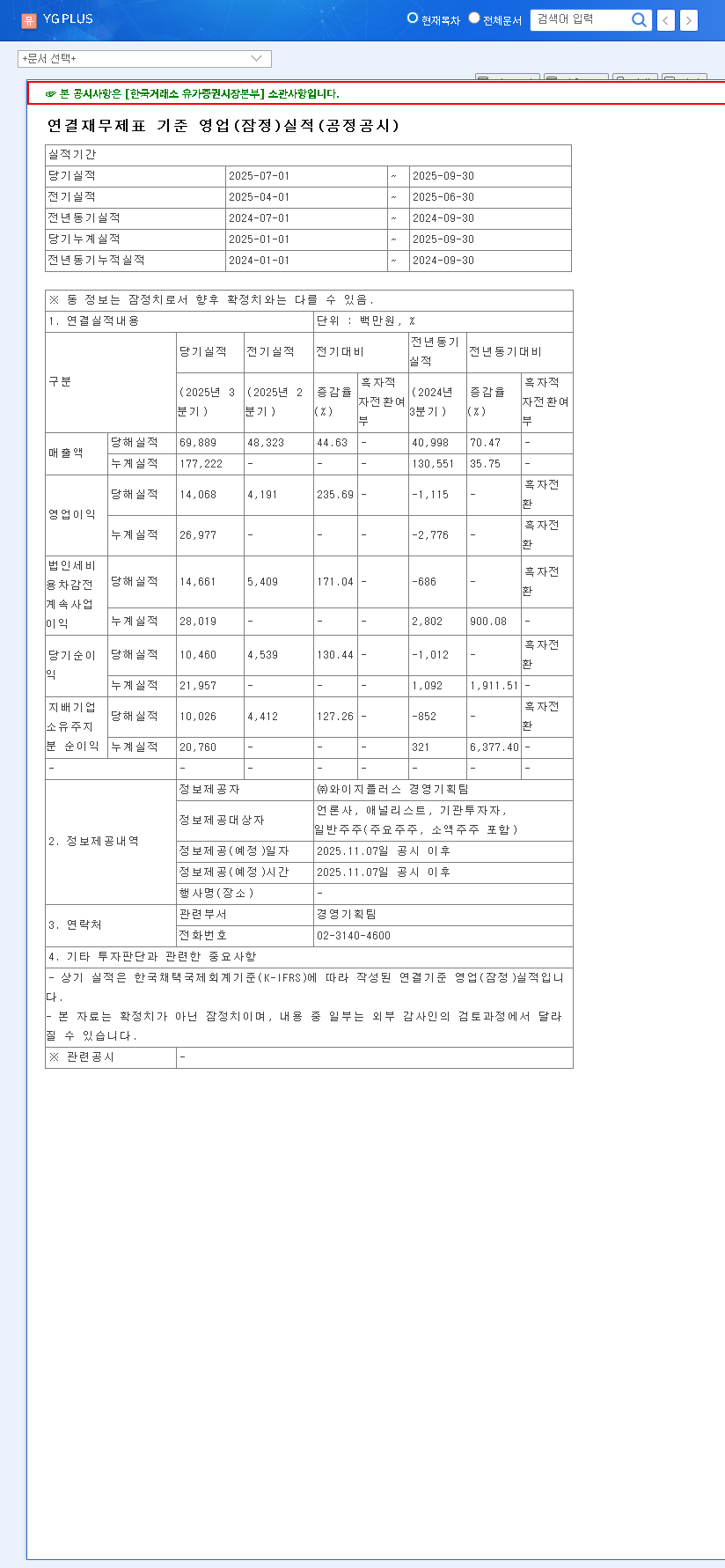

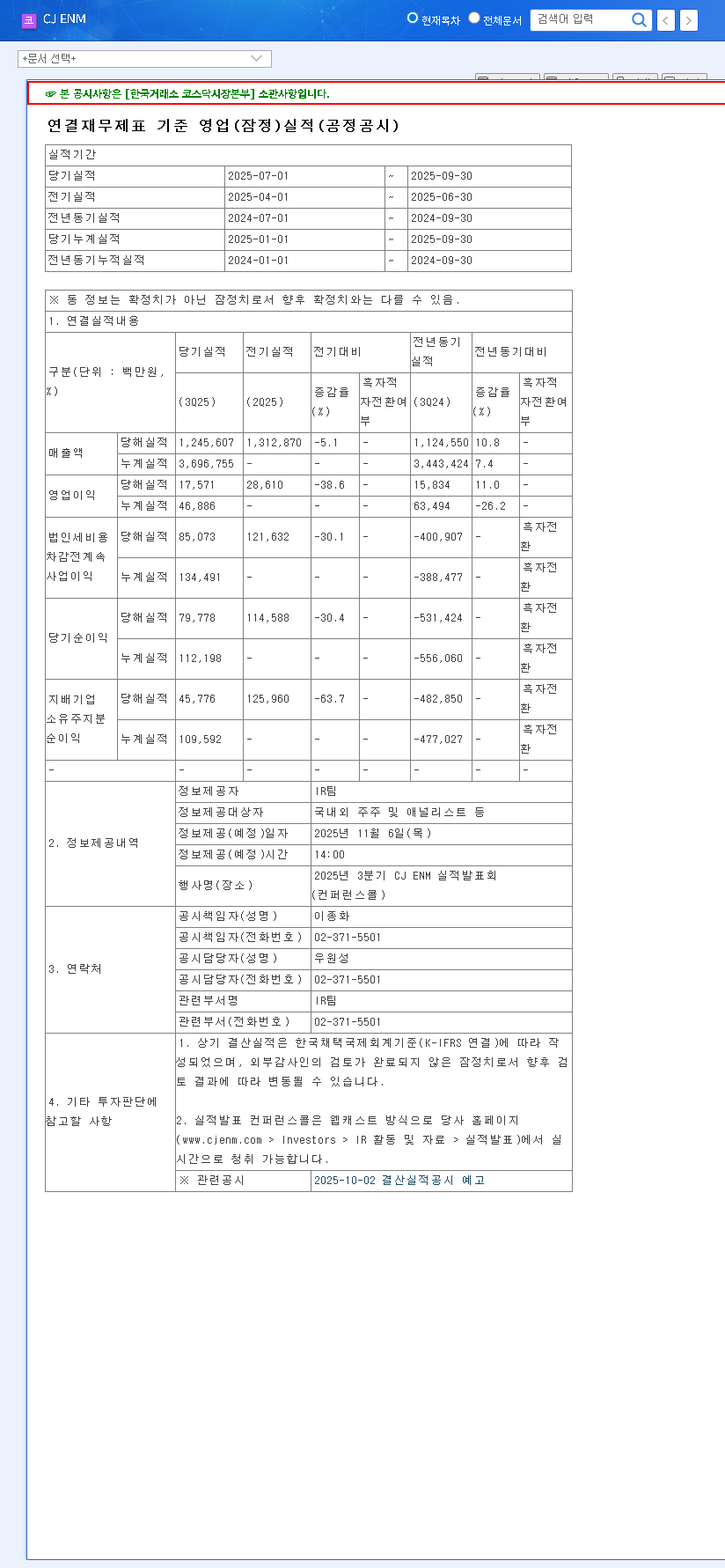

On November 12, 2025, GHOST STUDIO CO., LTD. released its preliminary operating results, signaling a significant positive shift. These figures, available in the Official Disclosure (DART), stand in stark contrast to the declining trends seen earlier in the year.

The Q3 turnaround is more than a rebound; it’s a testament to the company’s strategic pivot towards high-growth media content and business diversification, marking a critical inflection point for investors.

- •Revenue: KRW 20.9 billion

- •Operating Profit: KRW 4.3 billion (a significant turnaround to profitability)

- •Net Income: KRW 4.4 billion

These numbers show impressive growth not only quarter-over-quarter but also year-over-year. The 8.95% revenue surge compared to Q4 2024 and an operating profit that multiplied over three times highlight a robust operational improvement that the market has been waiting for.

Business Segment Analysis: A Tale of Two Trajectories

The story of GHOST STUDIO in 2025 is one of divergence. While its legacy gaming division faces headwinds, the burgeoning media and new business segments are emerging as powerful growth catalysts.

Media Content: The New Growth Engine

The media content business is unequivocally the star of the show. Building upon a stable webtoon and web novel foundation, the acquisition of GHOST STUDIO Co., Ltd. has supercharged its entry into high-stakes video production. The production of Netflix original series like “You Killed Me” and “Bloodhounds 2” positions the company to capitalize on the insatiable global demand for K-content. This strategic move provides a predictable, high-margin revenue stream that is less volatile than the hit-driven gaming market.

Gaming Business: Navigating a Competitive Landscape

The gaming division continues to face difficulties. Revenue from established casual titles like Solitaire and TriPeaks has declined due to intense market competition and shifting player preferences. The company is actively trying to right the ship by diversifying its portfolio with new releases such as ‘Match Miracle’ and exploring Web3 with ‘Pocket Battles NFT War.’ However, the success of these new ventures is not yet guaranteed and remains a key area for investors to monitor.

New Business: K-Beauty and Beyond

In a bold diversification play, GHOST STUDIO launched the cosmetic brand ‘PixelPure’ in May 2025. This expansion into the lucrative K-beauty market aims to create powerful synergies by leveraging the company’s roster of artists and media influence. For more on this trend, see our analysis of the global K-beauty industry. While still in its early stages, this venture represents an exciting new revenue stream with significant potential.

Financial Health: Signs of Strain Amidst Growth

While the Q3 profit numbers are encouraging, a look at the half-year report reveals underlying financial pressures. The aggressive expansion has led to a significant increase in total liabilities, rising from KRW 10.1 billion in 2023 to KRW 30.5 billion in H1 2025. Furthermore, operating cash flow turned negative, a metric that signals the company spent more on operations than it generated. These are classic ‘growing pains’, but they necessitate careful management of debt and liquidity to ensure long-term stability.

Investor Outlook: What to Watch for GHOST STUDIO Stock

The GHOST STUDIO Q3 2025 results paint a picture of a company in successful transition. The positive momentum from media and new ventures appears to be starting to outweigh the slump in gaming. For long-term investors, the key is to monitor whether this trend can be sustained. For context on market dynamics, sources like Reuters’ market analysis provide valuable macroeconomic insights.

Key Monitoring Points for Investors:

- •Media Momentum: Track the performance and critical reception of upcoming Netflix series. Consistent hits are crucial for sustained growth.

- •Gaming Turnaround: Watch for signs of life in the gaming division. Can new titles gain traction and contribute positively to the bottom line?

- •Financial Discipline: Monitor future earnings reports for debt reduction plans and a return to positive operating cash flow.

- •K-Beauty Traction: Look for updates on the market penetration and revenue contribution from the ‘PixelPure’ brand.

In conclusion, GHOST STUDIO presents a compelling, albeit complex, investment case. The company’s strategic shift is bearing fruit, but the journey is not without financial risks. Cautious optimism is warranted, and close monitoring of the factors above will be essential for making an informed decision on GHOST STUDIO stock.