The latest YG Entertainment Q3 2025 earnings report has sent ripples through the investment community. The K-Pop giant, home to global superstars, released figures that fell short of market consensus, sparking crucial conversations about its trajectory. This comprehensive analysis will dissect the report, explore the underlying causes for the performance miss, evaluate the company’s enduring strengths, and provide a forward-looking perspective for investors monitoring the dynamic K-Pop entertainment industry.

A Deep Dive into YG’s Q3 2025 Financials

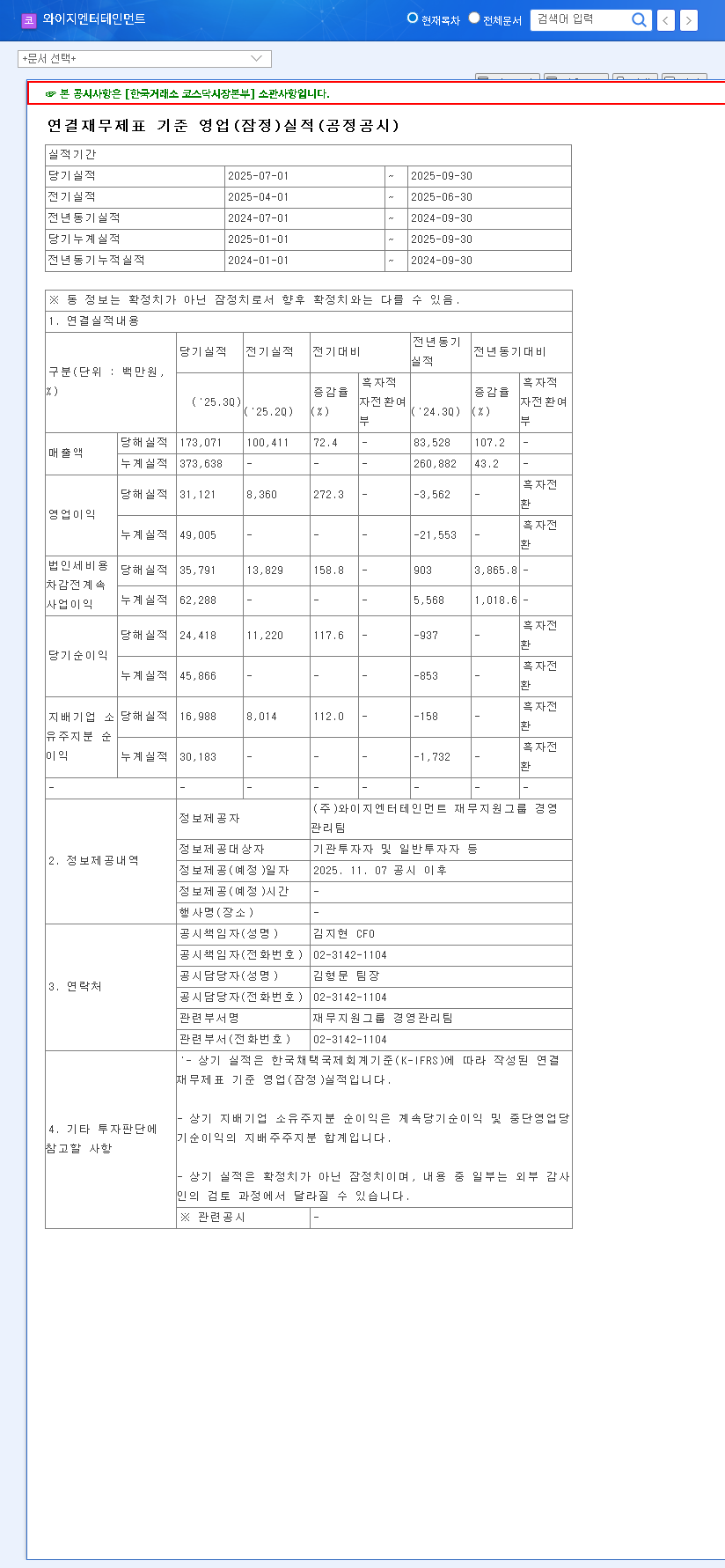

The Q3 2025 results revealed a notable deviation from analyst predictions, particularly on the bottom line. While top-line growth compared to the previous year was impressive, the failure to meet current-quarter expectations has raised concerns about YG Entertainment profitability and operational efficiency.

- •Revenue: Reported at ₩173.1 billion, missing the market expectation of ₩199.3 billion by 13.15%.

- •Operating Profit: Came in at ₩31.1 billion, an 8.26% shortfall against the forecasted ₩33.9 billion.

- •Net Income: The most significant miss, plummeting to ₩17.0 billion—a staggering 43.71% below the consensus of ₩30.2 billion.

This sharp drop in net income, far outpacing the revenue and operating profit misses, signals potential pressures from non-operating expenses or higher-than-expected costs, a critical area for our ongoing YG stock analysis.

What Caused the Underperformance?

Several convergent factors contributed to the Q3 earnings miss. Understanding these challenges is key to assessing the company’s future strategy.

Intensifying K-Pop Competition

The global K-Pop market is more crowded than ever. Increased investment from competitors in debuting new artists, aggressive global marketing campaigns, and securing brand partnerships means that the cost of maintaining market leadership is rising. These industry-wide pressures directly impact selling, general, and administrative (SG&A) expenses, squeezing profit margins.

Macroeconomic Headwinds

Global economic conditions are playing a significant role. A high exchange rate regime can unfavorably impact YG’s profitability, as a substantial portion of its revenue from global tours and merchandise is earned in foreign currencies. When converted back to Korean Won, this revenue is worth less. Concurrently, rising interest rates can increase borrowing costs for future projects and capital expenditures, adding further financial strain.

“While the headline numbers are disappointing, the year-over-year revenue growth proves the core product—YG’s artist IP—is still in high demand. The challenge now is not in generating sales, but in converting those sales to profit more efficiently in a tougher economic climate.”

Beyond the Headlines: YG’s Underlying Strengths

Despite the Q3 stumble, a holistic YG investor outlook must account for the company’s formidable assets and positive underlying trends.

- •Explosive Year-Over-Year Growth: The Q3 2025 revenue of ₩173.1 billion marks a massive leap from ₩83.5 billion in Q3 2024, showcasing the sustained external growth and global appeal of its artists.

- •Powerful Artist IP: Supergroups like BLACKPINK and TREASURE command immense global fandoms, providing a stable and diversified revenue engine through world tours, album sales, high-margin merchandise, and lucrative brand endorsements. This IP is the company’s crown jewel.

- •Sound Financial Health: A stable debt-to-equity ratio (84.85% as of year-end 2024) indicates that the company is not over-leveraged, mitigating immediate financial risks and providing flexibility for future investments.

Investor Outlook & Strategic Direction

The YG Entertainment Q3 2025 earnings report serves as a critical inflection point. Future stock performance will depend on the company’s ability to execute on key strategic initiatives. For a detailed breakdown of the financials, investors can review the Official Disclosure filed with DART (Source).

Maximizing Core Artist Activities

The most direct path to an earnings rebound lies with its established artists. The scale and frequency of BLACKPINK’s upcoming projects and the successful execution of TREASURE’s global tours are paramount. Furthermore, the successful growth of rookie group BABYMONSTER is essential for securing the company’s mid-to-long-term pipeline.

Diversification and Cost Efficiency

To improve margins, YG must aggressively diversify its IP business beyond traditional music sales. This includes expanding into digital content, character licensing, and Web3 initiatives. Simultaneously, a rigorous focus on cost control—from tour logistics to marketing spend—is necessary to weather macroeconomic pressures and protect the bottom line. As noted by sources like Bloomberg, managing operational costs is a key focus for the entire entertainment sector this year.

Investors should adopt a long-term perspective, focusing on these strategic pillars rather than short-term stock volatility. The company’s ability to leverage its powerful IP while navigating a complex market will ultimately define its success.