The latest DL Holdings Q3 2025 earnings announcement has sent ripples through the investment community, revealing a provisional net profit that dramatically undershot market consensus. This report provides a comprehensive DL Holdings investor analysis, breaking down the financial results, exploring the underlying causes for the underperformance, and outlining a strategic outlook for current and potential shareholders. As market volatility persists, understanding the intricacies of DL’s diverse business portfolio—from petrochemicals to construction—is more critical than ever for making informed decisions about DL Holdings stock.

Dissecting the DL Holdings Q3 2025 Earnings Report

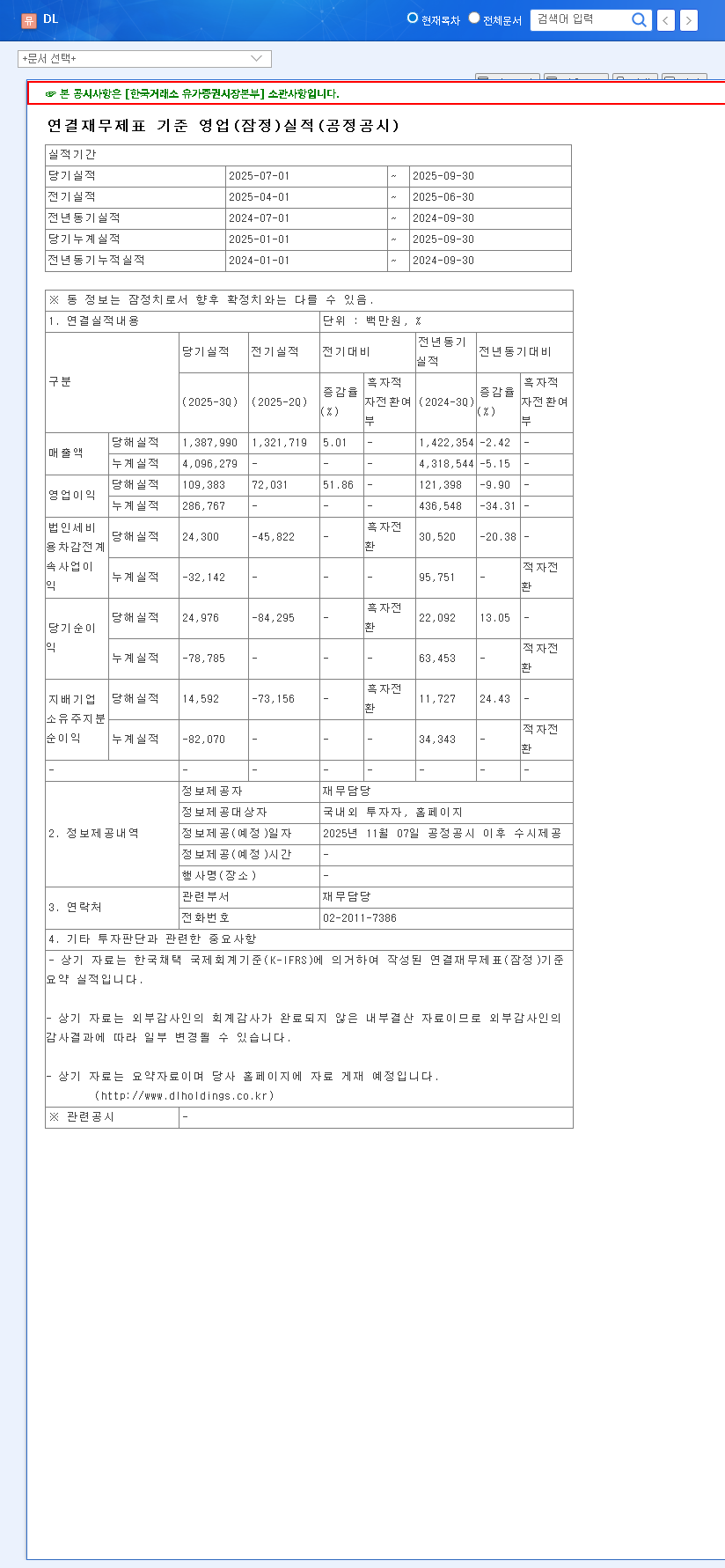

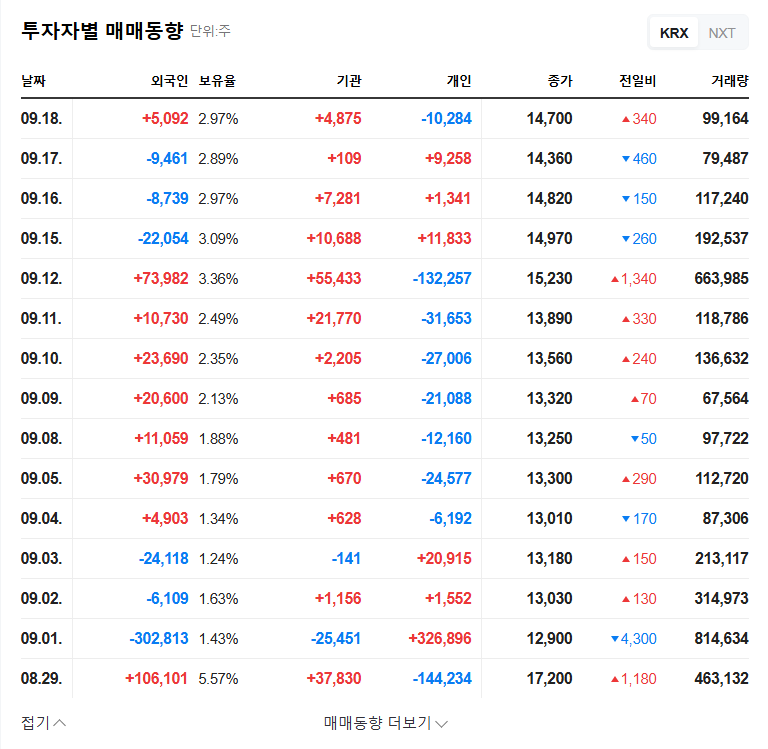

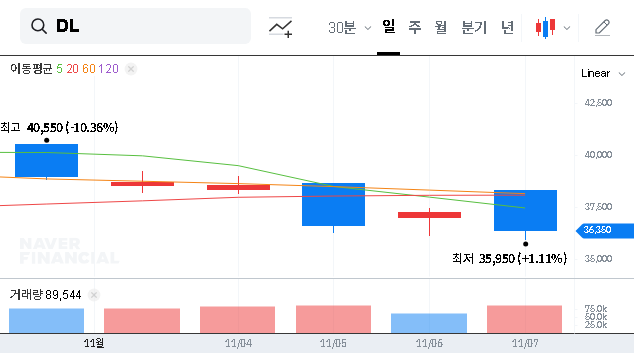

On November 7, 2025, DL Holdings CO.,LTD released its consolidated provisional operating results, which immediately drew market scrutiny. While top-line numbers were close to estimates, the bottom line told a very different story. The official figures can be reviewed in the company’s Official Disclosure on DART.

Key Financials vs. Market Expectations

Here’s a clear breakdown of the performance against market forecasts:

- •Revenue: KRW 1,388 billion, falling just 1.3% below the market estimate of KRW 1,407.4 billion.

- •Operating Profit: KRW 109.4 billion, a marginal 2.3% below the estimate of KRW 112 billion.

- •Net Profit: KRW 14.6 billion, a staggering 59.1% below the market estimate of KRW 35.7 billion.

The severe 59.1% miss on net profit is the central concern for investors, signaling potential margin pressures and increased financial costs that are eroding the company’s profitability more than anticipated.

Behind the Numbers: A Sector-by-Sector Breakdown

The underperformance wasn’t uniform across the conglomerate. A deeper dive reveals a story of resilience in some areas being overshadowed by significant headwinds in others.

Manufacturing (Petrochemicals, Automotive Parts): Facing Headwinds

The manufacturing division continues to struggle amidst a global economic slowdown. The persistent slump in global demand, exacerbated by China’s aggressive petrochemical capacity expansion, has squeezed margins. Furthermore, a cooling in the electric vehicle (EV) market growth has put pressure on the automotive parts segment. While DL is strategically pivoting towards high-value-added products, these macro trends, as analyzed by sources like Bloomberg Economics, present a formidable challenge.

Energy Sector: A Period of Transition

The energy sector is in a phase of strategic transition. Efforts to build future growth engines through the expansion of its renewable energy portfolio are underway. However, this quarter’s revenue saw a year-on-year decrease, largely due to base effects from the sale of certain power generation assets in the previous year. The long-term success of this segment hinges on the global pace of green energy adoption and evolving regulatory landscapes.

Construction (DL E&C): The Group’s Resilient Backbone

The standout performer is the construction sector, anchored by DL E&C performance. This division demonstrated robust results across its civil engineering, plant, and housing segments, reaffirming its status as the core growth engine for the group. Its strong order backlog and consistent execution provide a crucial buffer against the volatility in other sectors, contributing significantly to the group’s overall stability. Investors can learn more about its projects on our page covering DL E&C’s project portfolio.

Future Outlook and Investor Strategy

The significant DL Holdings net profit shortfall will likely trigger negative investor sentiment and could place short-term downward pressure on the stock price. Investors should brace for volatility. However, a purely bearish outlook may be premature.

What to Watch Moving Forward

A prudent mid-to-long-term investment strategy for DL Holdings stock requires monitoring several key indicators:

- •Manufacturing Recovery: Watch for signs of a global economic rebound and stabilization in the petrochemical market.

- •Renewable Energy Milestones: Look for tangible progress and profitability in the company’s green energy ventures.

- •Construction Sector Momentum: Continued strong order intake and execution by DL E&C are vital for group stability.

- •Cost Management: Scrutinize future earnings reports for effective control over financial costs and improvements in operating margins.

In conclusion, while the DL Holdings Q3 2025 earnings are disappointing, the company’s fate is not sealed. The resilience of its construction arm provides a foundation for recovery, but a turnaround in the manufacturing sector is essential for a meaningful rebound in profitability and stock performance.