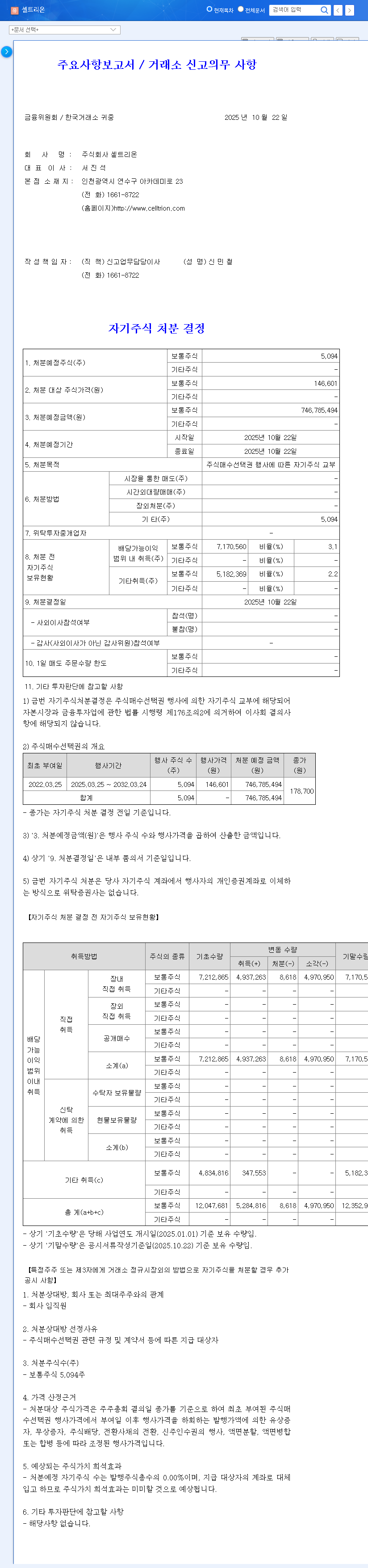

The biopharmaceutical landscape is buzzing as Celltrion, Inc., a global industry leader, advances its pipeline. The company has officially submitted a significant amendment for its Celltrion CT-P55 EU Phase 3 clinical trial. This drug, a proposed Cosentyx biosimilar, targets the multi-billion dollar autoimmune disease market. For investors, this move signals both a monumental opportunity and a period of calculated risk, directly impacting the long-term outlook for Celltrion stock.

This comprehensive guide will dissect the implications of the CT-P55 Phase 3 trial amendment, exploring the potential upside, the considerable hurdles, and the ultimate impact on Celltrion’s corporate value. We’ll provide a clear, data-driven analysis to help you make informed investment decisions.

What is Celltrion CT-P55 and Why Does it Matter?

At its core, Celltrion CT-P55 is a biosimilar candidate for the reference product Cosentyx (secukinumab). A biosimilar is a biological product that is highly similar to and has no clinically meaningful differences from an existing FDA or EMA-approved biologic. To learn more about them, you can review the European Medicines Agency’s overview of biosimilars.

Cosentyx is a blockbuster drug, generating over $4 billion in annual sales, primarily for treating conditions like plaque psoriasis, psoriatic arthritis, and ankylosing spondylitis. By developing a Cosentyx biosimilar, Celltrion aims to capture a significant share of this lucrative market by offering a more cost-effective alternative upon patent expiry, a strategy central to its future growth.

Dissecting the Phase 3 Trial Amendment

On October 27, 2025, Celltrion announced the submission of its amendment for the CT-P55 EU Phase 3 trial. This critical stage of drug development is designed to confirm the efficacy and safety of CT-P55 against the original Cosentyx in a large patient population with moderate to severe plaque psoriasis. According to the Official Disclosure, the simultaneous submission of Part 1 and Part 2 of the amendment suggests a streamlined and confident approach from Celltrion’s R&D team.

The Bull Case: Potential Positives for Investors

- •Strengthened Biosimilar Pipeline: Success with CT-P55 would significantly bolster Celltrion’s product portfolio, adding a high-value asset and securing a future revenue stream.

- •Demonstrated R&D Capability: Efficiently advancing a complex biosimilar to a late-stage trial reinforces market confidence in Celltrion’s scientific expertise and execution capabilities.

- •European Market Dominance: The EU is a key market for biosimilars. A successful launch would solidify Celltrion’s competitive position in the region. For a deeper look, consider reading our analysis of Celltrion’s Full Drug Pipeline and Market Strategy.

The Bear Case: Navigating Potential Risks

It is crucial for investors to remember that the statistical probability of a drug in clinical trials ultimately receiving marketing authorization is historically around 10%. This inherent uncertainty is a fundamental risk.

- •Risk of Clinical Failure: If trial results do not meet the stringent endpoints for efficacy and safety, the entire project could be delayed or terminated, leading to significant financial loss.

- •High Costs and Long Timelines: Phase 3 trials are incredibly expensive and time-consuming. These costs can weigh on short-term profitability before any revenue is generated.

- •Intense Market Competition: Celltrion is not alone. Other major players, like Sandoz, have already secured approval for their own Cosentyx biosimilar. This means Celltrion will enter a competitive market, potentially pressuring prices and market share.

Investment Outlook & Final Verdict

The advancement of the Celltrion CT-P55 Phase 3 trial is a fundamentally positive development for the company’s long-term strategy. However, it does not materially change the company’s short-term financials. The market’s reaction will be muted until concrete data from the trial emerges.

Investment Opinion: Neutral (Watch)

Our current outlook for Celltrion stock based on this event is Neutral. This is an event that requires mid-to-long-term monitoring. Investors should focus on the following key areas:

- •Monitor Trial Milestones: Keep a close watch for announcements regarding trial progress, data readouts, and eventual submission for marketing authorization to the EMA.

- •Assess the Competitive Field: Track the market penetration and pricing strategies of approved Cosentyx biosimilars to understand the environment CT-P55 will enter.

- •Evaluate Overall Financials: Do not invest based on a single pipeline. Continue to assess Celltrion’s overall revenue, profitability, and the performance of its other commercial products.

Frequently Asked Questions (FAQ)

What is the primary goal of the CT-P55 Phase 3 trial?

The primary goal is to demonstrate that CT-P55 has equivalent efficacy and a comparable safety profile to the original drug, Cosentyx, in treating patients with plaque psoriasis. This is a requirement for regulatory approval.

Will this news immediately affect Celltrion’s stock price?

Unlikely. This filing is a procedural step and was largely expected. Significant stock price movement is more likely to occur upon the announcement of positive or negative clinical trial results or regulatory decisions.

What are the biggest risks for the CT-P55 pipeline?

The three biggest risks are: 1) Failure to meet clinical endpoints in the Phase 3 trial, 2) Intense competition from other biosimilar manufacturers who may launch earlier, and 3) Potential regulatory delays from the EMA.