The TSI stock outlook has become a major point of interest for investors after TSI Co., Ltd. (티에스아이), a pivotal player in the secondary battery equipment industry, announced a landmark supply contract. The deal, valued at an impressive ₩28.4 billion, centers on their core technology: the 2nd battery mixing system. This development not only underscores the company’s strong market position but also raises critical questions about its future growth trajectory and valuation. In this comprehensive analysis, we will dissect the implications of this contract, evaluate the company’s fundamentals, and provide a detailed forecast for investors considering TSI.

Deconstructing the Landmark ₩28.4 Billion Deal

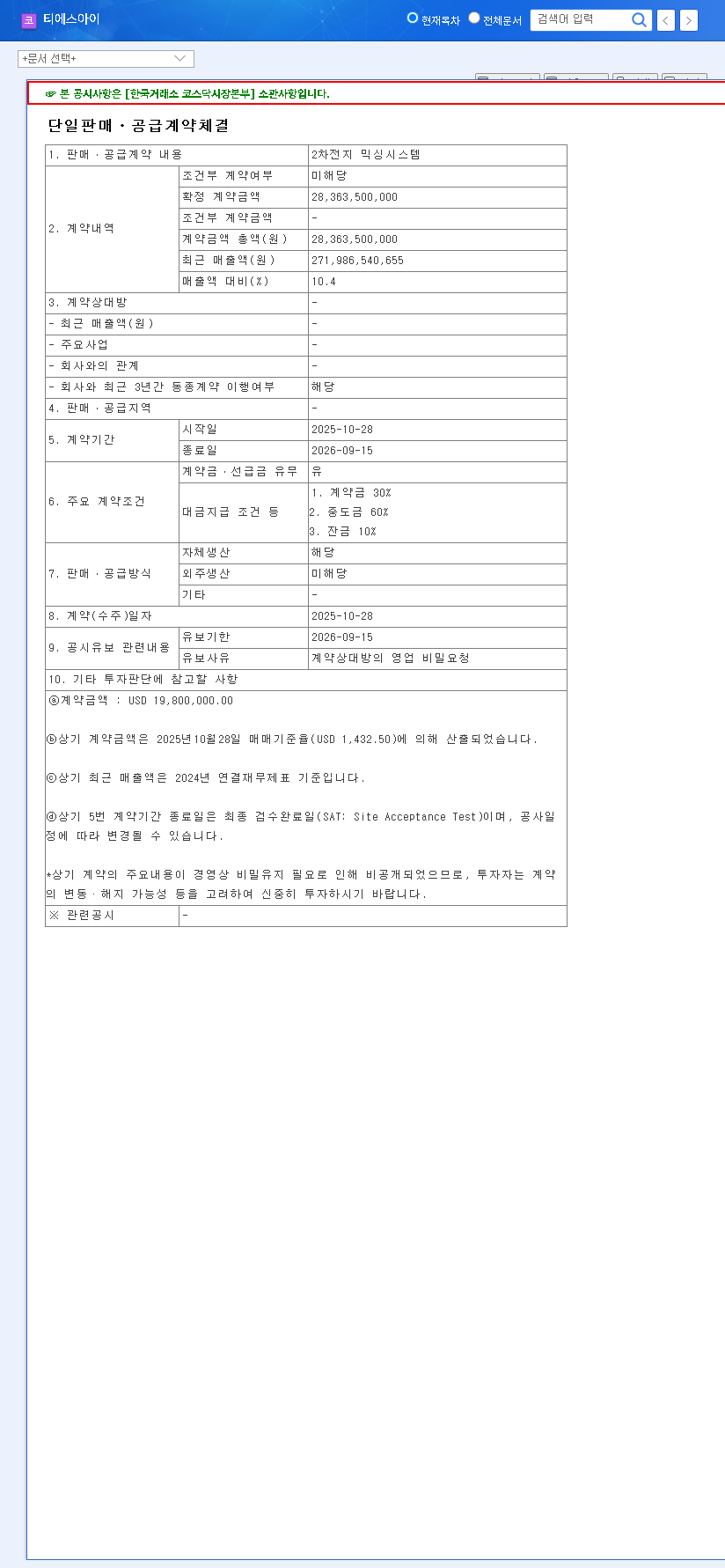

On October 29, 2025, TSI Co., Ltd. formally disclosed the signing of a single sales and supply contract that immediately captured the market’s attention. Let’s break down the key figures and what they mean for the company’s financials.

- •Contract Value: An substantial ₩28.4 billion KRW.

- •Revenue Impact: This single deal represents 10.4% of TSI’s entire revenue from the preceding business year.

- •Product: State-of-the-art 2nd battery mixing system technology.

- •Contract Period: A 10-month timeline from October 28, 2025, to September 15, 2026.

- •Source: The details were confirmed via an Official Disclosure filed with DART.

This contract is more than just a number; it is a powerful validation of TSI’s technological prowess and a clear indicator of secured revenue streams for the upcoming fiscal year. It significantly de-risks future earnings projections and strengthens the overall TSI investment analysis.

Core Growth Catalysts for TSI Co., Ltd.

Beyond this single announcement, several converging factors create a compelling growth story for TSI. Understanding these is key to evaluating the long-term stock outlook.

1. The Critical Role of the 2nd Battery Mixing System

The mixing process is one of the most crucial initial stages in lithium-ion battery production. A 2nd battery mixing system is responsible for creating a homogenous slurry by blending active materials, binders, and solvents. The quality of this slurry directly impacts the battery’s performance, capacity, and lifespan. TSI’s specialization in this niche but vital equipment positions them as an indispensable partner for major battery manufacturers. For more detail on battery components, you can explore resources from authorities like Stanford University’s energy research.

2. Riding the Wave of Global EV and ESS Expansion

The global shift towards electrification is unstoppable. The explosive growth in the Electric Vehicle (EV) and Energy Storage System (ESS) markets provides a powerful tailwind for the entire secondary battery equipment industry. Government policies like the U.S. Inflation Reduction Act (IRA) are further accelerating this trend by incentivizing domestic battery production. As gigafactories are built and expanded worldwide, the demand for core manufacturing equipment, such as TSI’s mixing systems, is set to soar. This secular growth trend is a core pillar of a positive TSI stock outlook. You can read more about this in our analysis of long-term EV market trends.

TSI’s successful turnaround to profitability in 2024, after a net loss in 2023, marks a significant financial inflection point. This new ₩28.4 billion contract is expected to cement this positive trajectory and drive strong earnings growth into 2025 and 2026.

3. Improved Financial Health and Transparency

Recent corporate actions by TSI Co., Ltd. have enhanced investor confidence. By amending business report disclosures to include greater detail on operations and financials, the company has increased its transparency. This, combined with a confirmed return to profitability, signals strengthening fundamentals and a management team focused on sustainable growth and shareholder value.

Comprehensive Risk Assessment

Despite the overwhelmingly positive news, a prudent TSI investment analysis must also consider potential risks. Investors should remain aware of the following factors:

- •Financial Leverage: The company has historically maintained a high debt-to-equity ratio. While manageable during growth phases, this reliance on borrowing could pose a risk if interest rates rise or if revenue growth unexpectedly slows.

- •Intensifying Competition: The lucrative secondary battery equipment market is attracting fierce competition from domestic and international players. TSI must continue to innovate to maintain its technological edge and pricing power.

- •Macroeconomic Headwinds: As an export-oriented company, fluctuations in currency exchange rates can impact profitability. While a high won/dollar rate is currently favorable, a sudden reversal could affect margins. Global economic slowdowns could also delay capital expenditures from battery manufacturers.

Final Verdict: A ‘Buy’ Opinion on TSI Stock Outlook

Considering the powerful combination of a secured, large-scale contract, strong industry tailwinds, and improving financial fundamentals, the TSI stock outlook is decidedly positive. The ₩28.4 billion order for its 2nd battery mixing system provides excellent revenue visibility and reinforces its competitive position.

While investors must monitor the identified risks, particularly financial leverage and market competition, the company’s growth potential appears to significantly outweigh these concerns. We therefore issue a ‘Buy’ opinion for TSI Co., Ltd. This is a compelling opportunity for investors seeking exposure to the core infrastructure of the global electrification revolution.