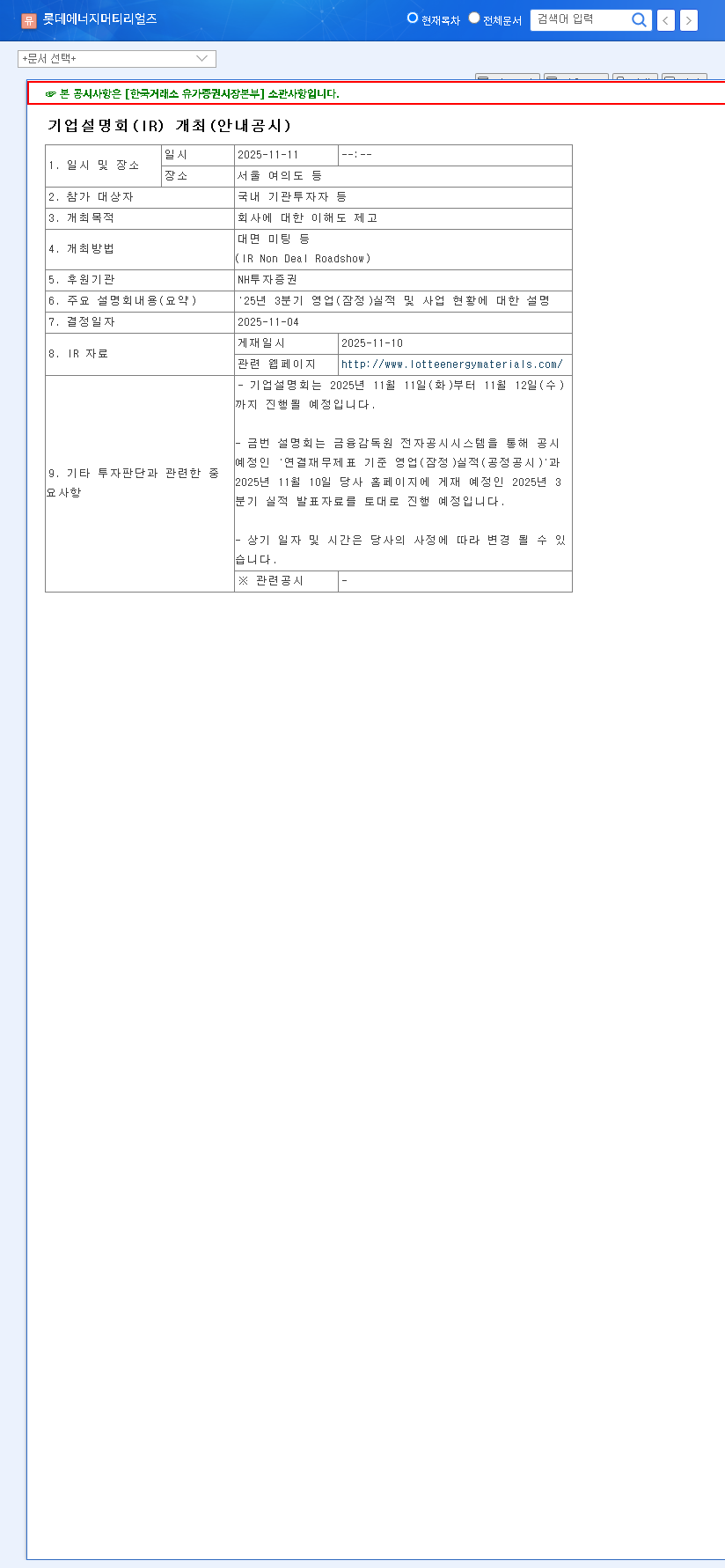

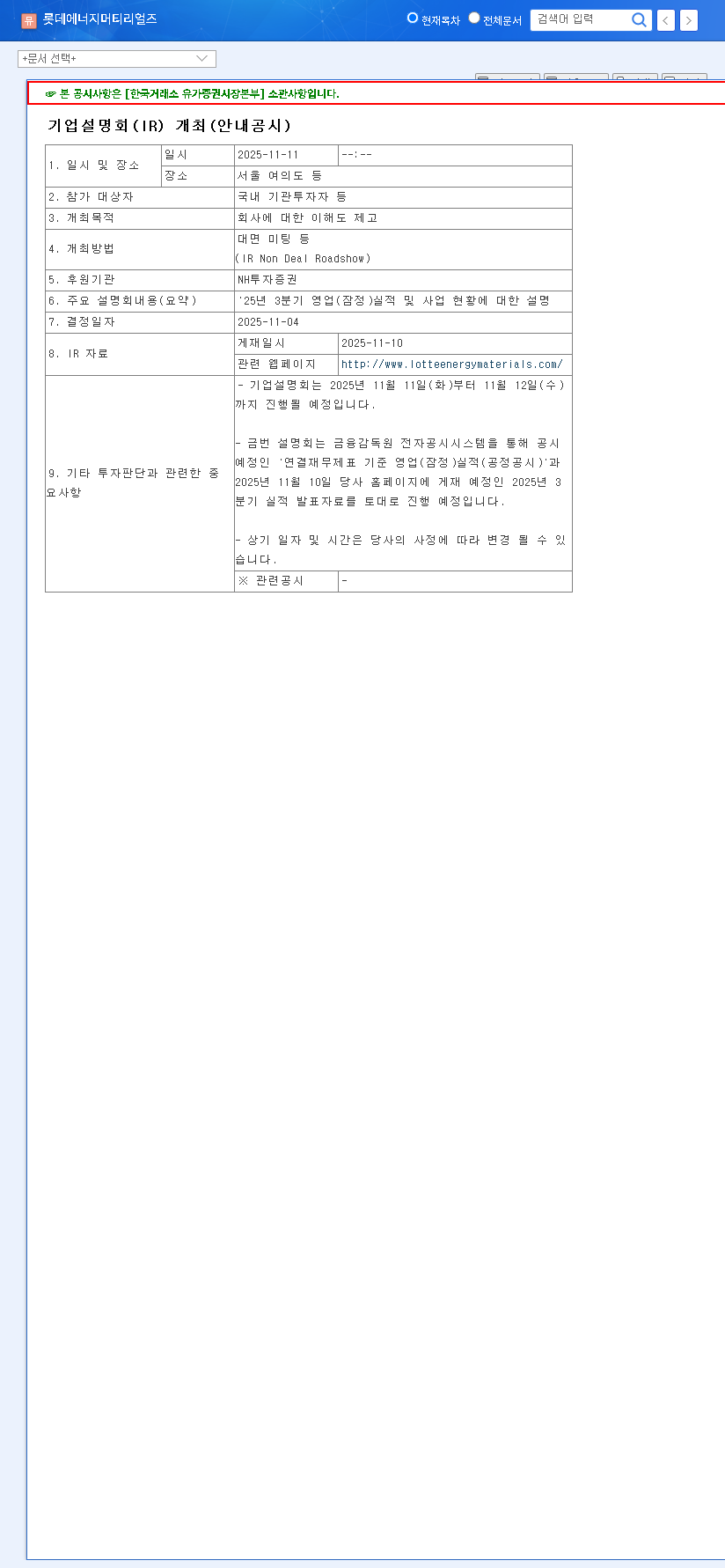

The latest financial report from LOTTE ENERGY MATERIALS has sent a wave of concern through the investment community. The company’s preliminary Q3 2025 earnings, announced on November 10, 2025, revealed a significant shortfall against market expectations, particularly in revenue and net profit. This performance raises critical questions about the company’s short-term stability and long-term growth trajectory in a competitive global market.

This comprehensive analysis will dissect the Q3 2025 results, explore the underlying causes of the underperformance, and provide a forward-looking perspective for investors. We will examine the macroeconomic headwinds, internal financial pressures, and the potential of future growth drivers like high-end Elecfoil for the AI sector to determine what lies ahead for LOTTE ENERGY MATERIALS stock.

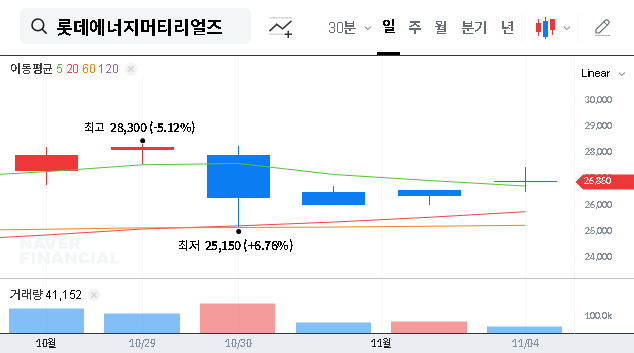

Q3 2025 Earnings Shock: The Numbers Don’t Lie

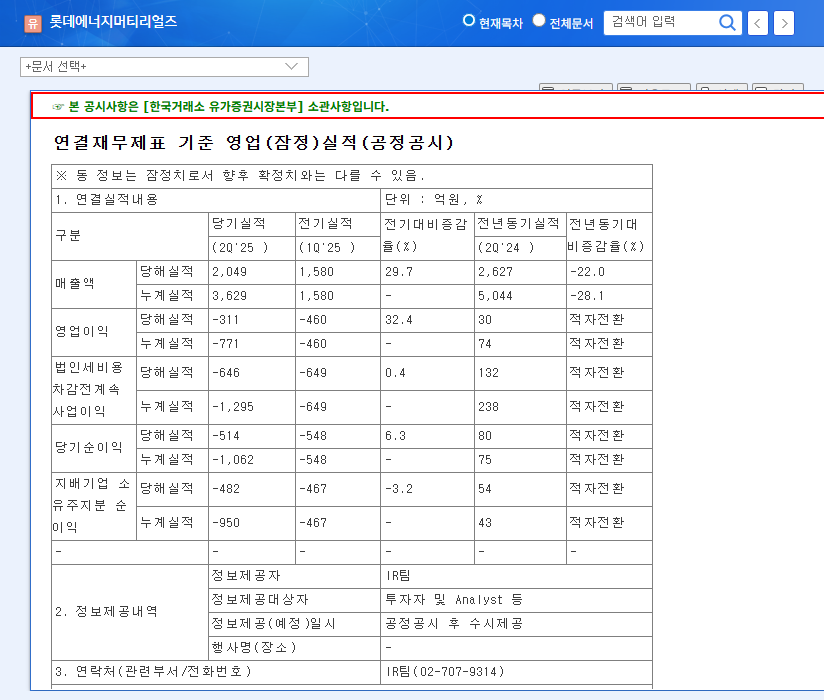

The preliminary Q3 2025 earnings for LOTTE ENERGY MATERIALS painted a challenging picture, missing analyst consensus on multiple fronts. The deviation from expectations, especially in net profit, has amplified concerns regarding the company’s financial resilience.

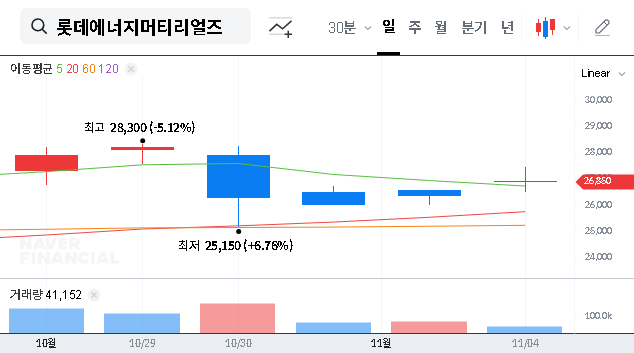

The most alarming figure was the net profit, which came in at just a fraction of the forecast, signaling deeper financial strains than the market had anticipated and putting immediate downward pressure on LOTTE ENERGY MATERIALS stock.

Key Financial Figures vs. Expectations

- •Revenue: KRW 143.7 billion, a significant 15.3% below the market expectation of KRW 169.6 billion.

- •Operating Profit: KRW -34.3 billion, largely in line with expectations but representing a continued and widening loss.

- •Net Profit: KRW -25.4 billion, a staggering 263% below the consensus estimate of KRW -7.0 billion.

These figures are based on the company’s official filing. You can review the complete data in the Official Disclosure on DART.

Dissecting the Underperformance: A Multifaceted Challenge

The disappointing results for LOTTE ENERGY MATERIALS are not due to a single issue but rather a convergence of external market pressures and internal cost challenges.

Revenue Slump: Global Headwinds and Fierce Competition

A primary driver of the revenue miss was the underperformance of the materials division, particularly in Elecfoil (copper foil) exports. The global economic slowdown has softened demand for electric vehicles (EVs), while the secondary battery market has become increasingly saturated with competitors. According to market analysis from sources like BloombergNEF, this intense competition is squeezing profit margins industry-wide. Simultaneously, while the domestic construction arm remained stable, its growth was not enough to offset the sharp decline in the core materials business.

Profitability Squeeze: Rising Costs and Investment Burdens

The persistent operating loss reflects a difficult cost environment. Key factors include the rising price of copper, a critical raw material, and increased logistics costs. Furthermore, significant capital expenditures related to expanding overseas production facilities have yet to yield returns, contributing to the financial drag. The sharp decline in net profit was exacerbated by rising Selling, General & Administrative (SG&A) expenses and foreign exchange-related losses, intensifying the financial burden on the company. For a deeper understanding of these metrics, you can learn more about how to analyze a company’s financial health.

Investor Outlook: Navigating the Path Forward

Given the current circumstances, investors are justifiably cautious. The short-term outlook for LOTTE ENERGY MATERIALS is clouded by uncertainty, but long-term potential remains if the company can navigate its challenges effectively.

Short-Term Pain vs. Long-Term Gain

In the immediate future, negative investor sentiment is likely to exert downward pressure on the stock price. The key challenge is a crisis of confidence. However, the long-term thesis is not entirely broken. LOTTE ENERGY MATERIALS possesses significant technological advantages in high-end products. The growing demand for specialized circuit foil for AI accelerators presents a vital opportunity to pivot toward higher-margin markets and away from the commoditized EV battery space.

Key Points for Investors to Monitor

A ‘Neutral’ or ‘Underweight’ stance appears prudent until there are clear signs of a turnaround. Aggressive buying is not recommended. Instead, investors should closely monitor the following key indicators:

- •Q4 2025 Earnings Report: The single most important upcoming catalyst. Any sign of revenue stabilization or cost control will be crucial.

- •High-Value Product Sales: Watch for specific company announcements on sales growth for circuit foil targeted at the AI industry.

- •Operational Efficiency: Progress on optimizing new overseas facilities to reduce the cash burn rate.

- •Financial Structure Improvement: How the company manages its debt and interest expenses, especially following the recent hybrid bond issuance.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All investment decisions should be made based on your own research and judgment.