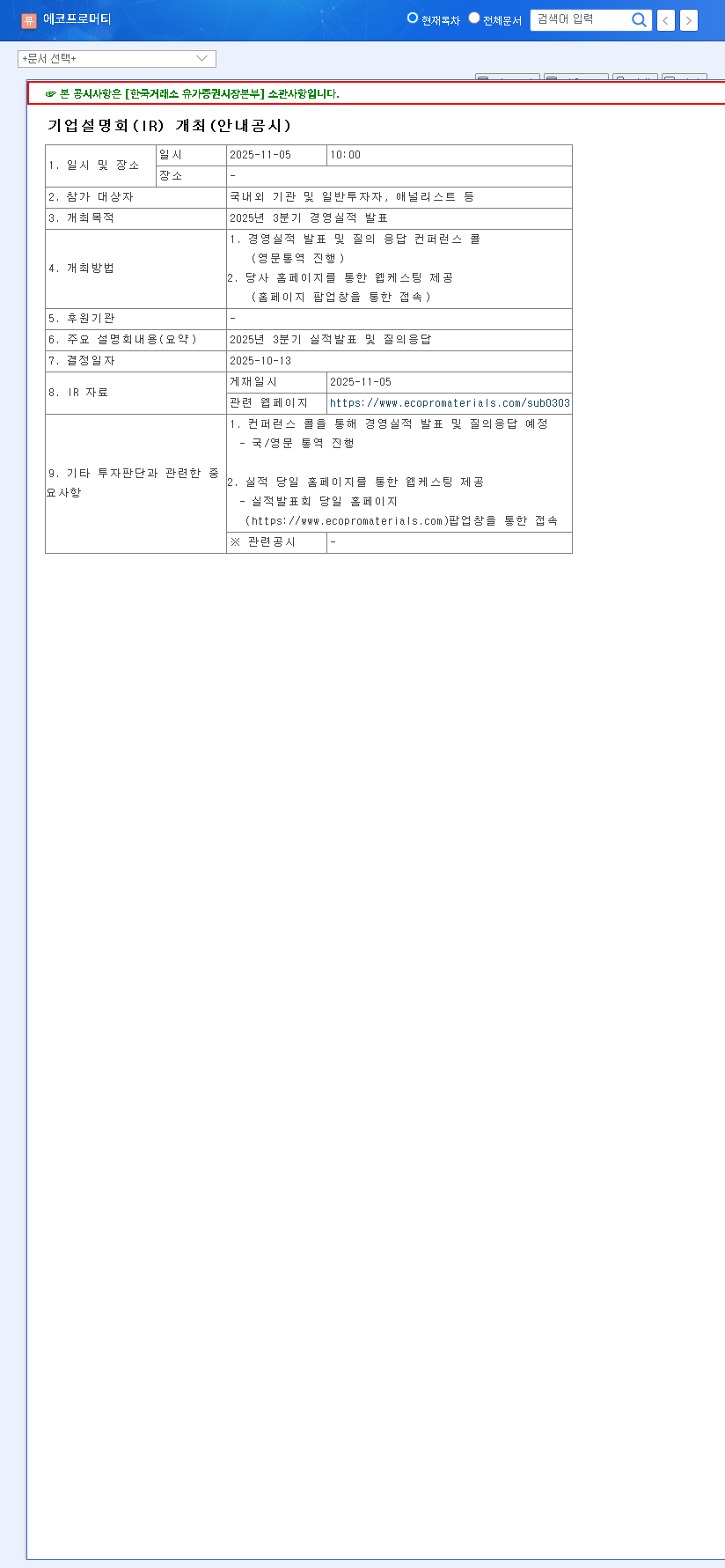

The upcoming ECOPRO MATERIALS IR for Q3 2025 represents a critical moment for investors. Scheduled for November 10, 2025, this investor relations conference is poised to address mounting concerns following a challenging first half of the year. For stakeholders in ECOPRO MATERIALS CO., LTD., a key player in the competitive secondary battery materials market, this event will be a pivotal indicator of the company’s future trajectory and its ability to navigate market headwinds.

This comprehensive analysis will dissect the company’s recent performance, explore the key questions investors should be asking, and outline the potential outcomes of the Q3 2025 IR. We will provide a deep dive into the financial landscape, competitive pressures, and strategic initiatives that will define ECOPRO MATERIALS’ path forward.

Will the Q3 2025 IR reveal a concrete path back to profitability and restore market confidence, or will it confirm deeper underlying challenges for ECOPRO MATERIALS CO., LTD.? This is the central question on every investor’s mind.

The Current Landscape: H1 2025 Performance Review

To understand the significance of the upcoming IR, we must first analyze the company’s performance in the first half of 2025. While top-line growth was impressive, profitability issues have cast a shadow over its prospects.

Financial Health: A Mixed Picture

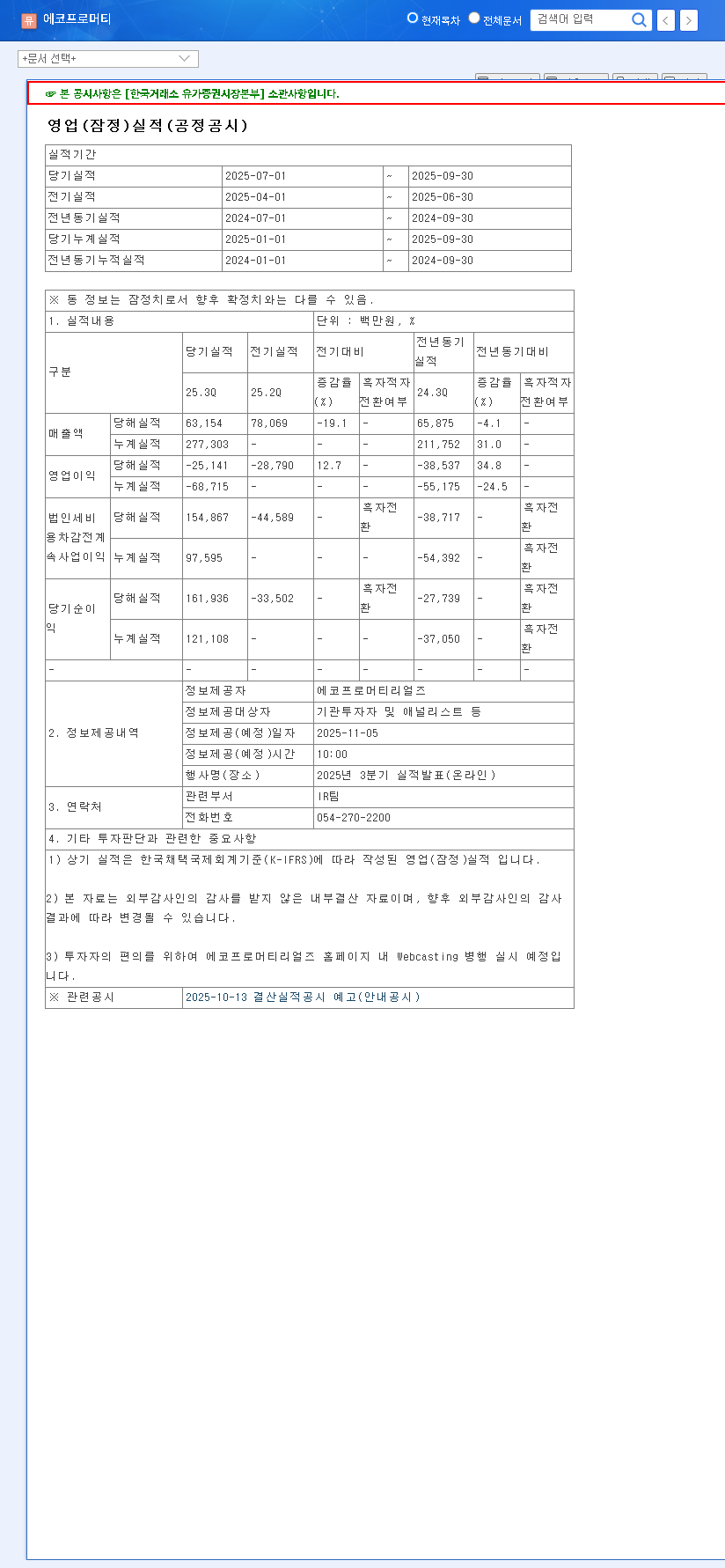

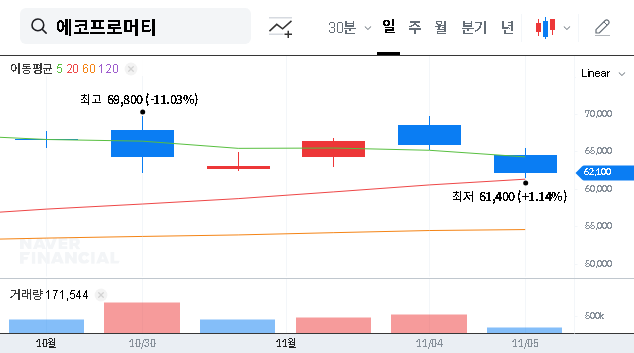

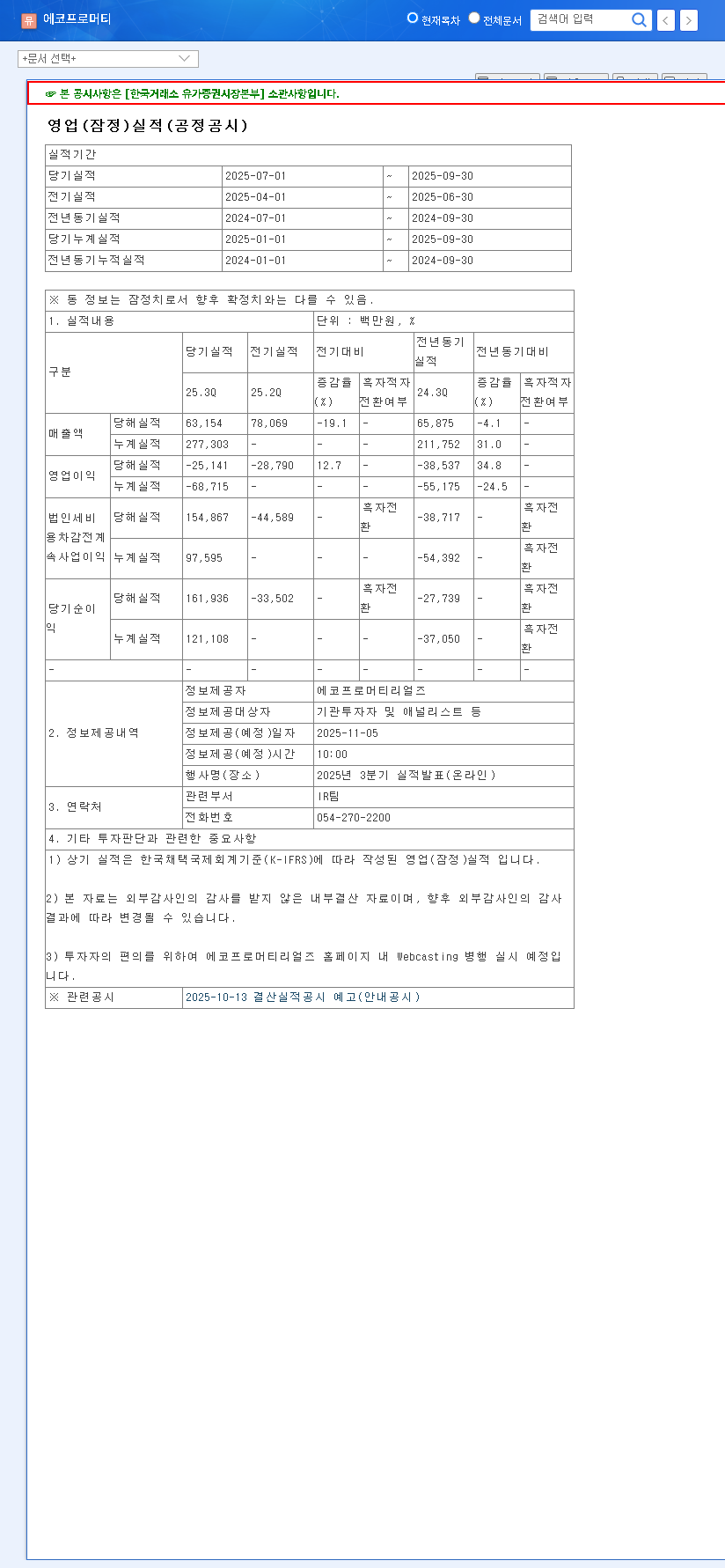

- •Impressive Revenue Growth: Revenue surged to KRW 214.15 billion, a 46.8% increase year-over-year, largely fueled by strong precursor material sales.

- •Profitability Under Pressure: Despite revenue growth, the company posted an operating loss of KRW 43.57 billion. This troubling shift was attributed to a higher cost of sales, increased SG&A expenses, and rising financial costs.

- •Capital Infusion: ECOPRO MATERIALS successfully raised approximately KRW 515 billion via preferred stock issuance to bolster its financial structure. However, increased borrowings mean that managing debt and financial stability remains a key priority.

Key Focus Points for the ECOPRO MATERIALS IR

Investors should scrutinize the details provided during the Q3 2025 IR. The management’s clarity and strategic vision on the following points will be crucial for rebuilding trust and outlining a sustainable growth model.

1. The Path to Profitability

The most pressing issue is the plan to reverse the operating losses. Investors will expect more than just assurances. Look for concrete, actionable strategies, including:

- •Cost Management: Detailed plans for reducing the cost of sales, which may involve more efficient raw material sourcing or process optimization.

- •Pricing Strategy: How the company plans to adjust its pricing in a competitive market to protect margins.

- •Operational Efficiency: Initiatives to streamline selling and administrative expenses without hampering growth.

2. Strategic Growth and Competitive Positioning

The global EV and secondary battery materials landscape is evolving rapidly, as documented by industry leaders like BloombergNEF. ECOPRO MATERIALS must articulate a clear strategy to maintain its edge. This includes updates on its core competencies such as high-nickel precursor technology and its internalized RMP process. For more information, you can read our guide on understanding precursor materials in EV batteries.

3. Risk Mitigation and Financial Stability

Volatility in raw material prices (nickel, cobalt) and currency exchange rates pose significant threats. The company’s presentation must address its hedging strategies and plans for managing its debt load. A clear roadmap to improving the debt-to-equity ratio will be a strong positive signal.

Potential Outcomes and Investor Takeaways

The market’s reaction to the ECOPRO MATERIALS IR will hinge on the quality and credibility of the information presented. A positive scenario involves a clear turnaround strategy that restores confidence, potentially leading to a stock price recovery. Conversely, a lack of concrete plans or results that miss expectations could lead to further selling pressure.

Ultimately, the success of this investor relations event depends on transparency. Management’s ability to frankly address challenges while presenting a believable and robust strategy for future growth will determine whether this IR marks a positive turning point for ECOPRO MATERIALS CO., LTD. and its shareholders.

Frequently Asked Questions (FAQ)

When will the ECOPRO MATERIALS Q3 2025 IR take place?

The investor relations conference is scheduled for November 10, 2025, at 4:00 PM KST. For official details, you can view the Official Disclosure on DART.

What is the main concern for investors?

The primary concern is the company’s profitability. After reporting an operating loss of KRW 43.57 billion in H1 2025 despite revenue growth, investors are looking for a clear strategy to improve margins and return to profitability.

What are the key risk factors for ECOPRO MATERIALS?

Key risks include continued profitability issues, high cost of sales, volatility in raw material prices like nickel and cobalt, currency exchange rate fluctuations, and intensifying competition within the secondary battery materials market.