Our comprehensive analysis of the ECOPRO MATERIALS Q3 2025 earnings report reveals a complex and challenging landscape for investors. While a surprising net profit turnaround has captured headlines, persistent underlying issues like declining revenue and significant operating losses paint a more cautionary tale. This deep dive will dissect the official figures, explore the fundamental pressures on the business, and provide a clear, neutral investment thesis for ECOPRO MATERIALS going forward.

For those tracking ECOPRO MATERIALS stock, understanding these conflicting signals is critical. We’ll explore whether this quarter’s profit is a sustainable trend or a temporary anomaly in the volatile secondary battery market.

Unpacking the ECOPRO MATERIALS Q3 2025 Earnings Report

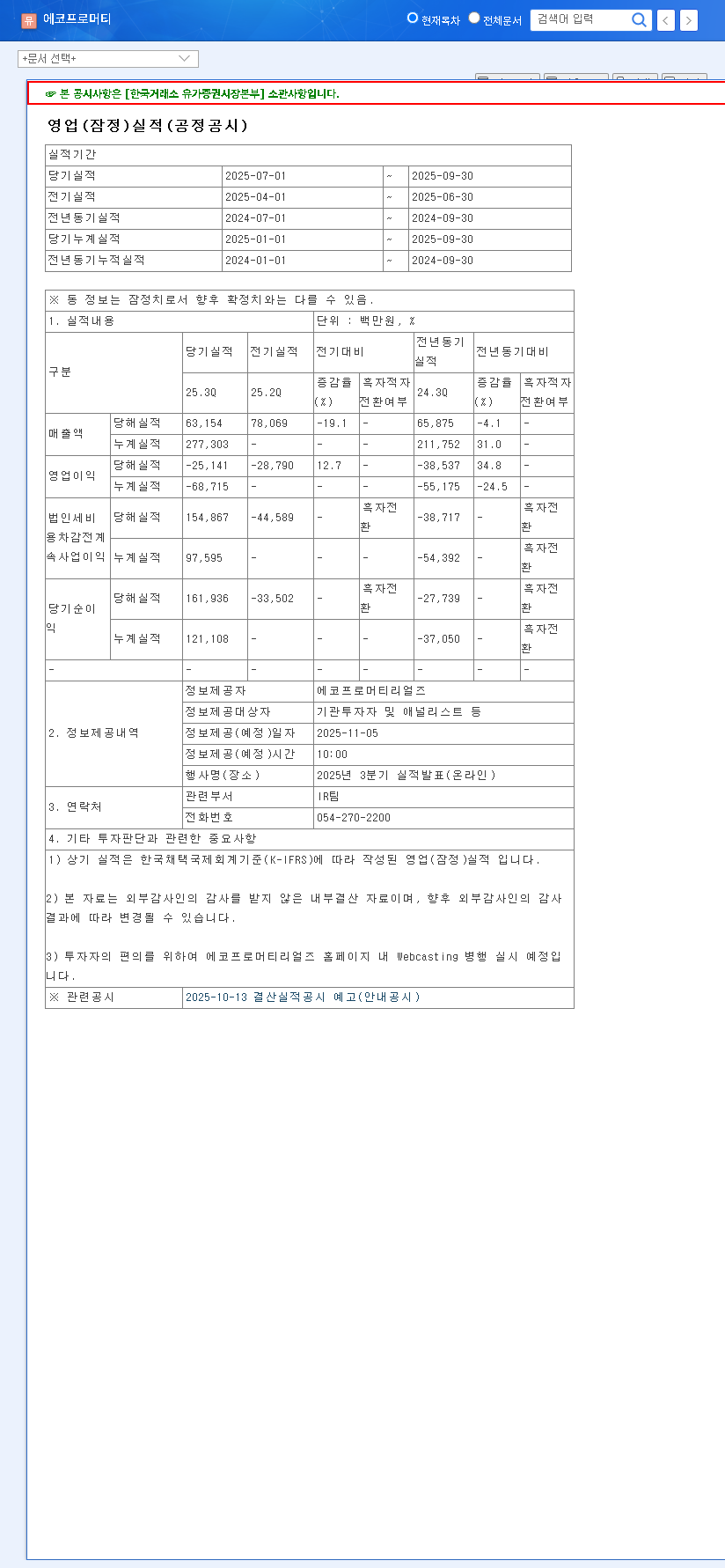

On November 5, 2025, ECOPRO MATERIALS released its preliminary third-quarter earnings, presenting a classic mixed bag of results that requires careful interpretation. The headline figure was undoubtedly the impressive shift to a net profit of 161.9 billion KRW. However, the details beneath the surface reveal ongoing struggles.

- •Revenue: 63.2 billion KRW, marking an estimated year-over-year decrease.

- •Operating Profit: -25.1 billion KRW, an operating loss that is estimated to have widened compared to the previous year.

- •Net Profit: 161.9 billion KRW, a significant turnaround to profitability year-over-year.

This divergence between operating performance and net profit is a major red flag. It suggests that non-operating factors, such as foreign exchange gains, asset sales, or other one-time events, may have driven the net profit figure. A detailed analysis of the company’s official disclosure is necessary to confirm the sustainability of this profit. (Official Disclosure: DART)

While the net profit turnaround is a positive headline, the core operational health, indicated by declining revenue and widening operating losses, remains a primary concern for long-term investors.

Fundamental Headwinds: Growth vs. Profitability

To understand the Q3 results, we must look at the company’s performance in the first half of 2025. While revenue grew an impressive 46.8% YoY to 214.1 billion KRW, the operating loss deepened to 43.57 billion KRW. This highlights a critical dilemma: the company is aggressively pursuing growth in the precursor market at the expense of profitability.

Raw Material Volatility and Market Pressures

The secondary battery sector is heavily influenced by commodity prices. ECOPRO MATERIALS faces significant exposure to:

- •Nickel Prices: A multi-year decline in nickel prices, driven by oversupply, has a dual effect. It lowers raw material costs but also puts downward pressure on final product pricing, squeezing margins. Future price movements will depend heavily on Indonesian export policies and global EV demand, as reported by leading commodity analysts (Reuters).

- •Cobalt Supply: Short-term supply instability, especially due to export restrictions from the Democratic Republic of Congo, creates price volatility and adds uncertainty to production costs.

- •Macroeconomic Factors: Global interest rates, currency fluctuations (especially the KRW/USD exchange rate), and geopolitical risks add further layers of complexity to the business environment.

Financial Health and Investment Burden

Aggressive expansion requires significant capital. The company’s continuous investment in production capacity has increased its debt burden and fixed costs. While a capital infusion of 407.7 billion KRW in April 2025 provided a welcome boost to the balance sheet, overall cash flow has deteriorated due to these large-scale investment activities. This financial strain is a key risk factor that investors must monitor closely.

Investment Analysis and Future Stock Outlook

Given the conflicting data points from the ECOPRO MATERIALS Q3 2025 earnings, our investment opinion remains a cautious ‘Neutral’. The potential for a short-term stock price rebound exists based on the net profit news, but sustainable, long-term growth hinges on the company’s ability to solve its core operational issues.

Key Factors to Watch

- •Sustainability of Net Profit: Investors must scrutinize the full financial statements once released to determine if the Q3 profit was from core operations or a one-off event.

- •Revenue Growth Trajectory: A reversal of the revenue decline in Q4 and beyond is critical to validating the company’s growth story.

- •Path to Operating Profitability: The most important metric will be a clear and credible plan to reduce and eventually eliminate operating losses. This requires significant cost structure improvements.

- •Market Conditions: Continuously monitor the broader EV market, competitive pressures, and raw material trends. To learn more, see our full guide on investing in the secondary battery supply chain.

In conclusion, while the Q3 net profit offers a glimmer of hope, it is overshadowed by fundamental operational challenges. A prudent approach involves waiting for more clarity on the source of this profit and concrete evidence of a turnaround in revenue and operating margins before committing significant capital to ECOPRO MATERIALS stock.