The market is buzzing with anticipation for ECOPRO BM CO.,LTD., a global leader in the secondary battery cathode material market. Following a significant profit turnaround in the first half of 2025, all eyes are on the company’s upcoming Investor Relations (IR) conference. This event is more than just a presentation; it’s a critical moment that could define the trajectory of the ECOPRO BM stock for the foreseeable future. This comprehensive ECOPRO BM analysis will provide an in-depth look at the company’s fundamentals, the immense potential of the IR event, and the key factors investors must monitor to make informed decisions.

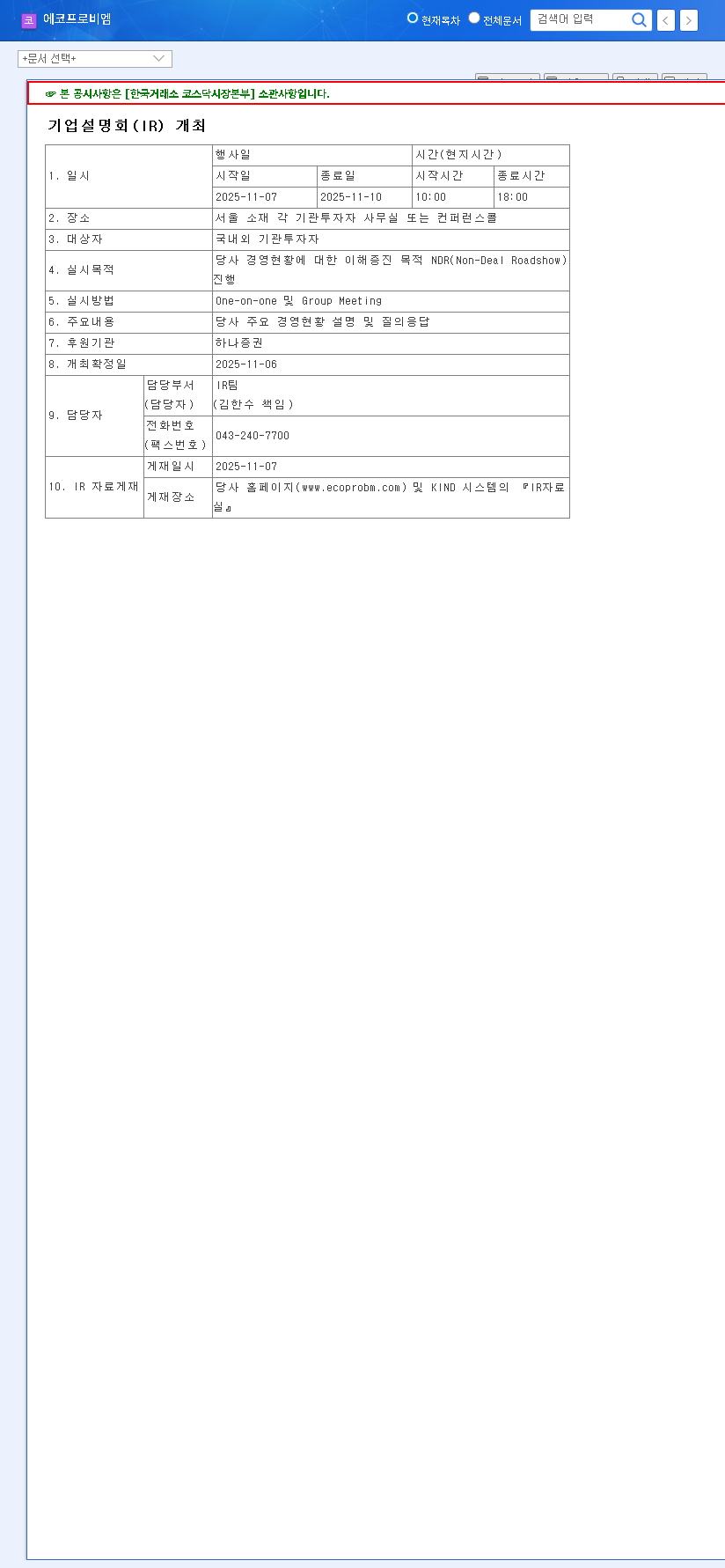

The Main Event: The November 7th, 2025 IR Conference

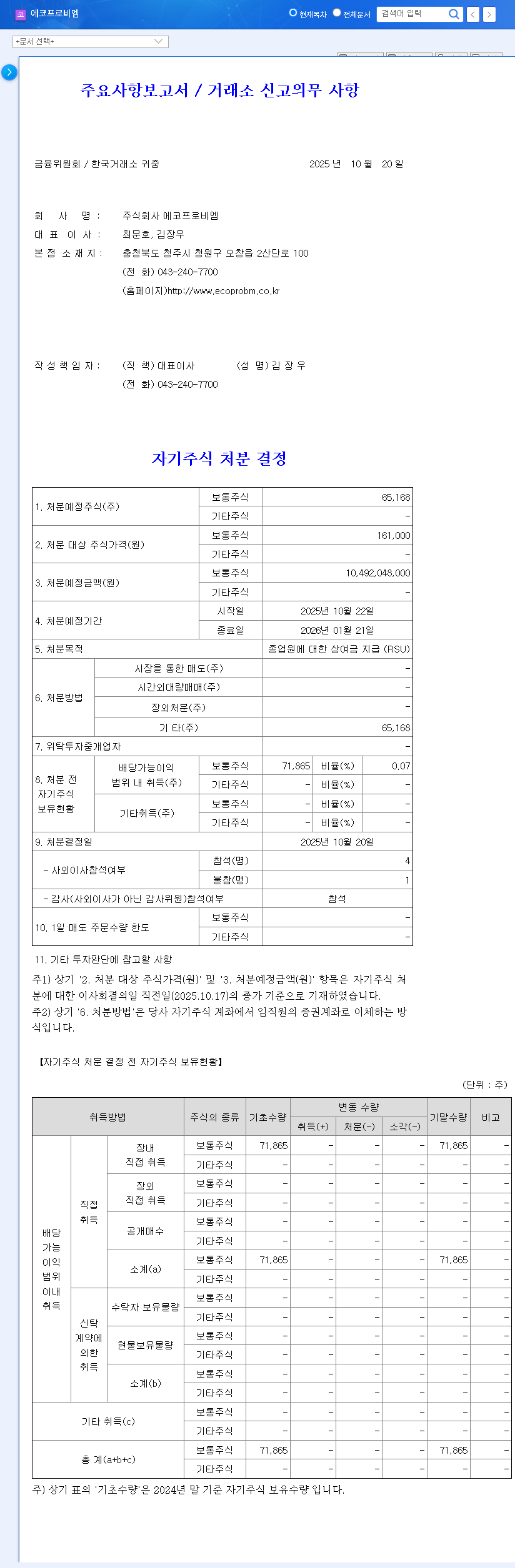

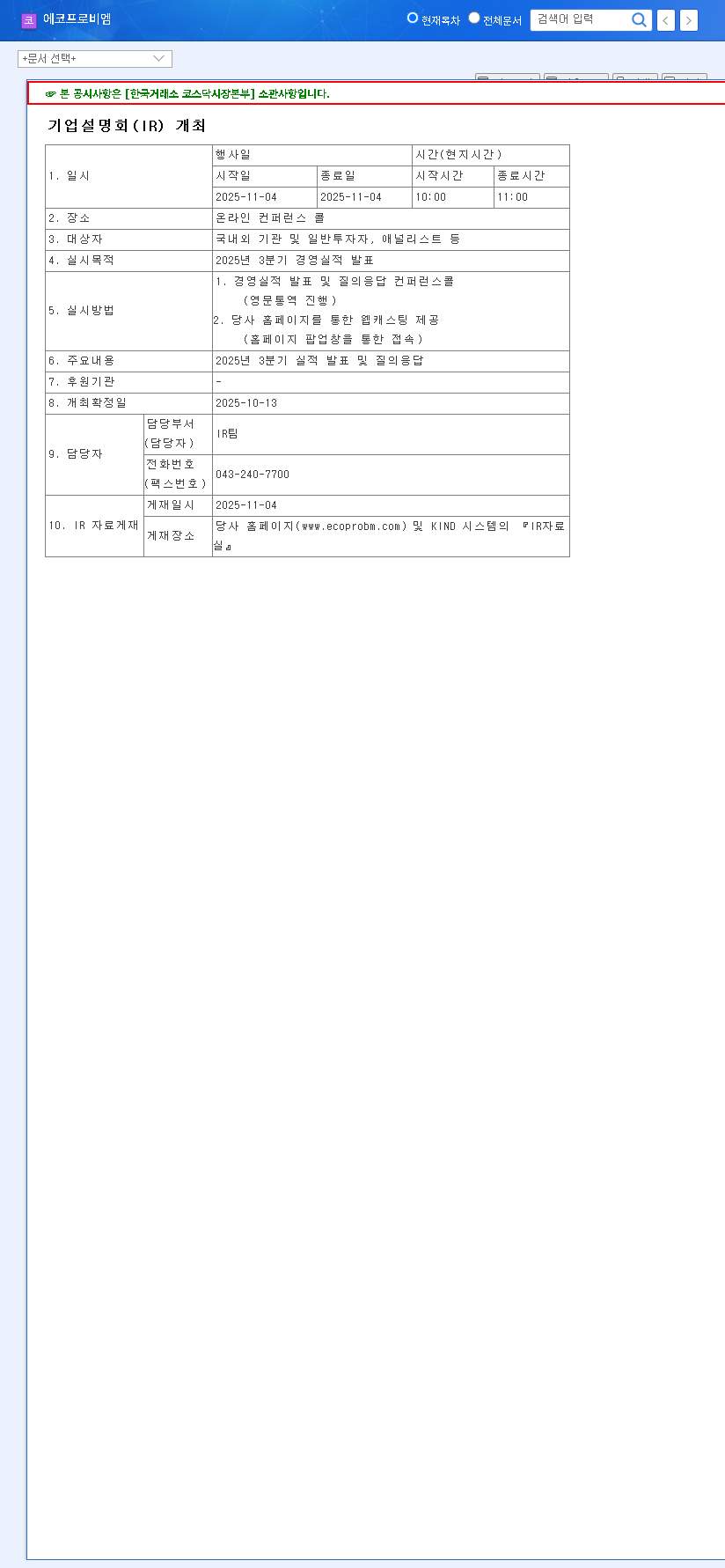

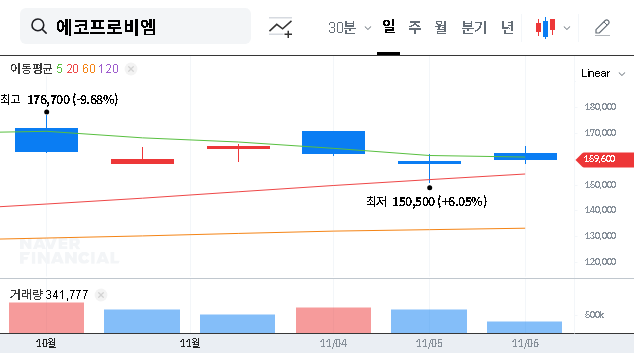

On November 7, 2025, ECOPRO BM will host a non-deal roadshow (NDR) for major investors. This platform is designed to offer a transparent look into the company’s current operational health, strategic direction, and financial standing. Given the recent positive performance shifts, investor expectations are incredibly high for this ECOPRO BM IR. The company’s management will have the opportunity to directly address market concerns and showcase their vision for growth. For official details on this event, you can view the Official Disclosure on DART.

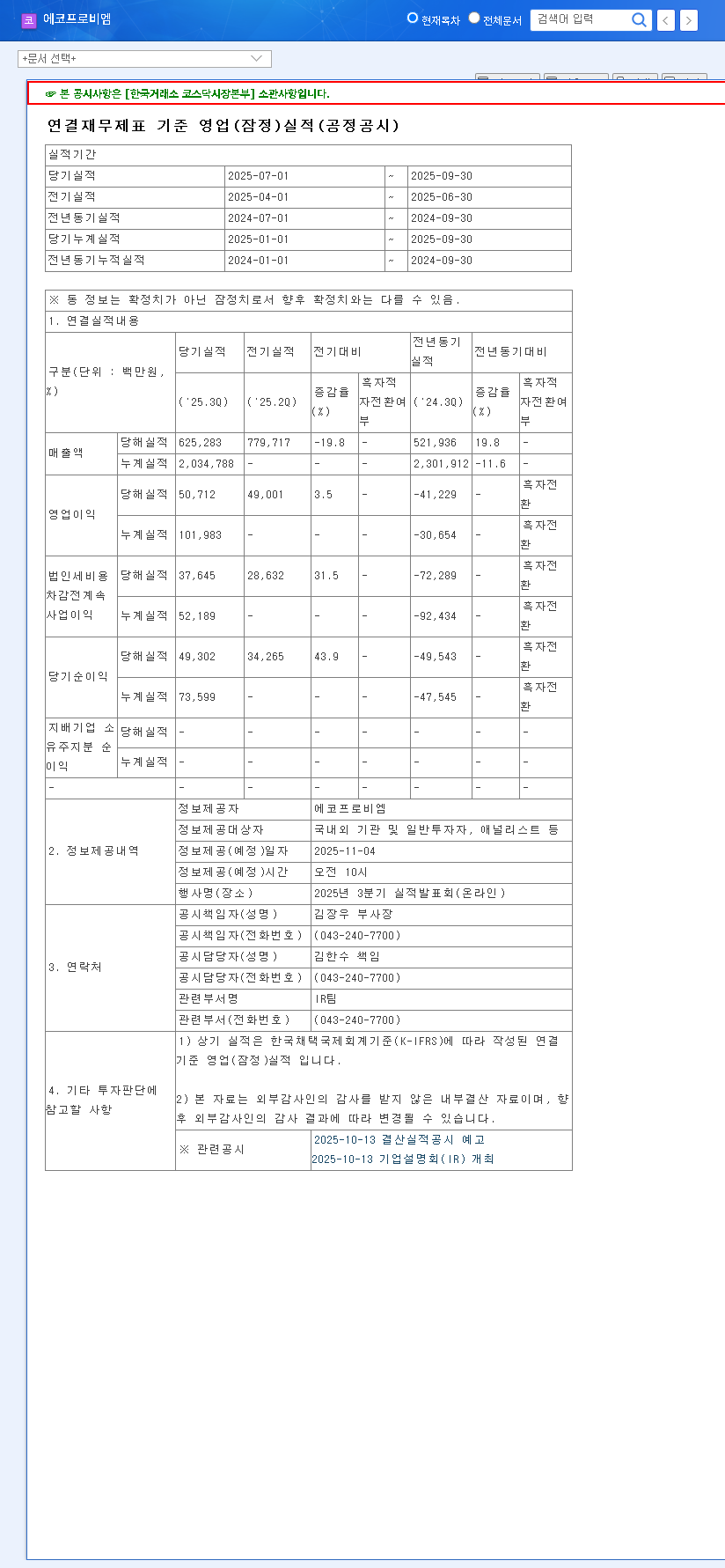

Unpacking the H1 2025 Performance: A Tale of Two Realities

To understand the future, we must first analyze the present. ECOPRO BM’s first-half performance of 2025 was a mixed bag, revealing both impressive resilience and underlying financial pressures that investors must consider.

📈 The Bright Side: Profitability and Market Dominance

The biggest headline was the company’s successful return to profitability. This signals strong operational management and robust demand for its high-value products.

- •Profit Turnaround: Despite a 48.9% YoY revenue dip to KRW 1.4095 trillion, ECOPRO BM achieved an operating profit of KRW 51.271 billion, a remarkable feat driven by cost-cutting and a better product mix.

- •Cathode Material Leadership: The company holds a powerful position in the high-nickel NCA (Nickel Cobalt Aluminum) and NCM (Nickel Cobalt Manganese) cathode material markets, which are critical for high-performance EV batteries.

- •Future Growth Engines: Aggressive CAPA expansion, development of overseas facilities, and R&D into next-gen materials position the company to capitalize on the booming global EV and ESS markets.

📉 The Headwinds: Financial Strain and External Risks

However, the financial statements also reveal points of caution that could weigh on the ECOPRO BM stock if not addressed clearly during the IR.

- •Negative Cash Flow: The consolidated operating cash flow turned negative to the tune of -KRW 260.176 billion, a significant concern for liquidity and financial health.

- •High Debt Levels: A persistent reliance on borrowing to fund expansion creates a financial burden, especially in a volatile interest rate environment.

- •External Volatility: The company’s profitability is highly sensitive to price fluctuations in raw materials like nickel and lithium, as well as geopolitical tensions and customer concentration (92.1% with major clients).

The upcoming IR conference is a pivotal moment. ECOPRO BM must convince investors that its growth strategy is robust enough to overcome its financial headwinds and market volatility.

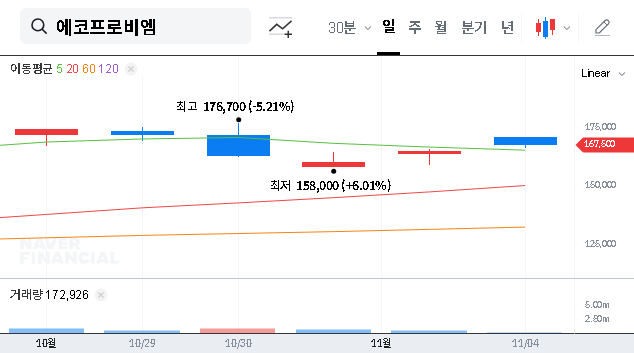

Potential Scenarios & Impact on ECOPRO BM Stock

The outcome of the IR will likely push the stock in one of two directions. A successful presentation could restore confidence and trigger a significant rally for this promising EV battery stock.

The Bull Case: Restored Confidence and Upward Momentum

If management delivers a transparent and compelling narrative—providing clear strategies for improving cash flow, managing debt, and diversifying its customer base—investor sentiment could improve dramatically. Detailed, realistic roadmaps for expansion and R&D would help the market re-evaluate the company’s long-term value, potentially leading to a sustained price increase.

The Bear Case: Unanswered Questions and Amplified Risk

Conversely, if the presentation is vague, avoids tough questions about financial health, or presents overly optimistic projections without substance, it could backfire. The exposure of unexpected negative information or a failure to address market anxieties could lead to a sell-off as uncertainty and perceived risk increase.

Investor Action Plan: What to Watch for at the IR

To conduct a thorough ECOPRO BM analysis, investors should focus intently on the following points during the conference:

- •Financial Health Roadmap: Demand concrete plans for improving operating cash flow and a clear strategy for managing and reducing debt.

- •Profit Sustainability: Scrutinize the feasibility of their cost-reduction initiatives and plans to further increase sales of high-margin products.

- •Growth Strategy Specifics: Look for realistic timelines, funding plans, and execution capabilities for CAPA expansion and overseas projects.

- •Risk Management: Assess how the company plans to mitigate risks from raw material price volatility and customer dependency.

- •Q&A Session Insights: Pay close attention to how management handles challenging questions from analysts and investors. Their candor (or lack thereof) can be very revealing. For more on this, check out our guide to analyzing corporate earnings calls.

In conclusion, the November 7th IR event is a watershed moment for ECOPRO BM and its investors. A well-executed conference that addresses key concerns could solidify its position as a top-tier EV battery stock and unlock significant value. However, investors must remain vigilant, balance optimism with caution, and make decisions based on a thorough analysis of the information presented.

Disclaimer: This report is for informational purposes only and is based on publicly available information. It does not constitute investment advice. The ultimate responsibility for investment decisions rests with the individual investor.