Analyzing the Q3 2025 Kakao Earnings Shock

The latest Kakao Corp. earnings report for Q3 2025 has sent a seismic wave through the market, delivering a significant ‘earnings shock’ that fell dramatically short of analyst consensus. For investors holding or watching Kakao Corp. (035720), this moment is pivotal. The results raise critical questions about the company’s current trajectory, the health of its core business segments, and its future growth prospects in an increasingly competitive landscape. This comprehensive analysis will dissect the numbers, explore the underlying causes, and provide a clear, actionable framework for investors navigating what’s next for this South Korean tech giant.

Understanding the context behind this financial downturn is crucial. We will move beyond the headlines to offer a detailed look at the internal and external factors contributing to the underperformance, from struggling business units to challenging macroeconomic conditions.

The Q3 2025 Results: A Stark Miss on All Fronts

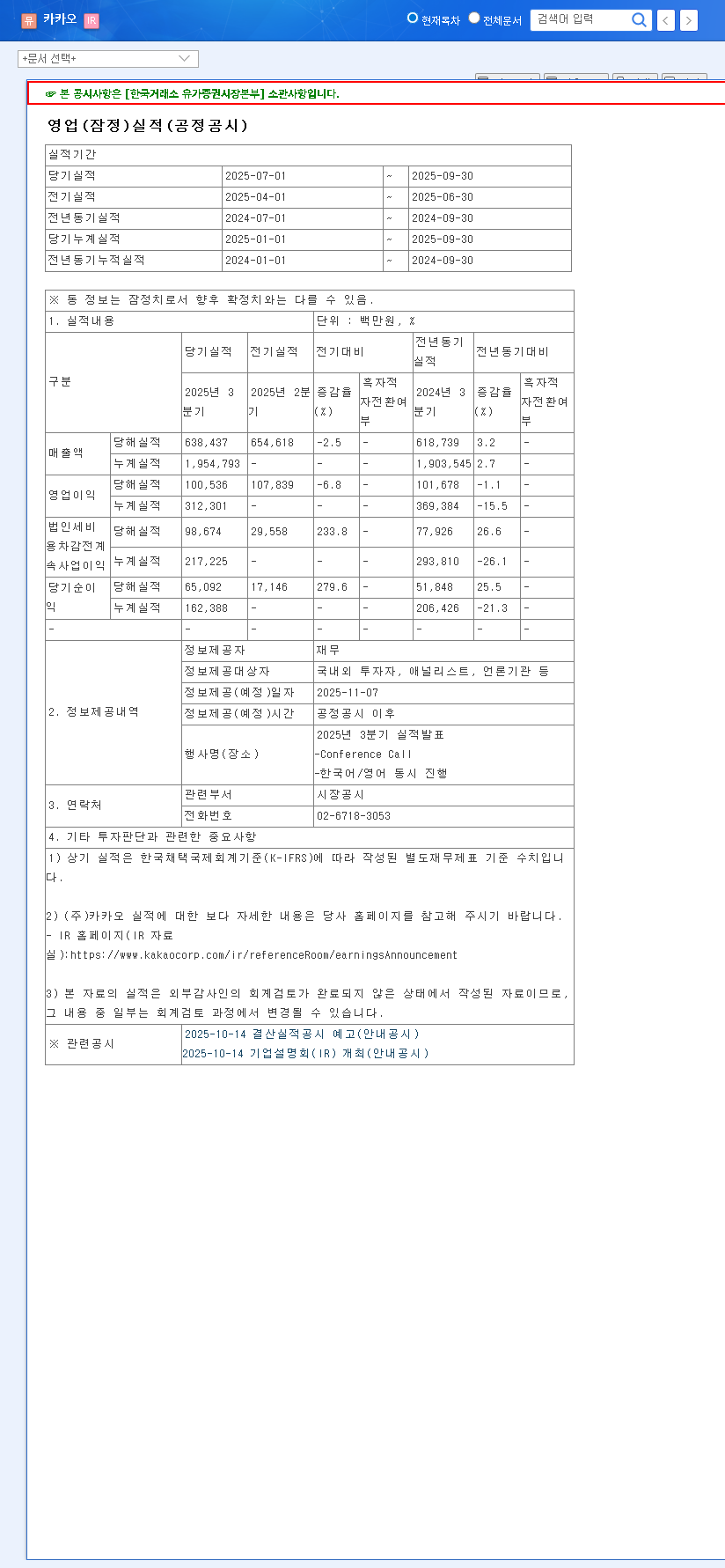

The term ‘earnings shock’ is not an exaggeration. Kakao Corp.’s preliminary operating results for the third quarter of 2025 revealed a staggering discrepancy from market expectations. The performance wasn’t just a slight miss; it was a fundamental deviation from projected growth, signaling potential systemic issues.

Key Financial Figures vs. Expectations

The announced figures painted a grim picture when compared to the consensus forecasts:

- •Revenue: Reported at KRW 638.4 billion, a shocking 69% below the expected KRW 2,031.6 billion.

- •Operating Profit: Came in at KRW 100.5 billion, a 39% miss from the anticipated KRW 164.5 billion.

- •Net Profit: Totaled KRW 65.1 billion, falling 52% short of the KRW 136.9 billion forecast.

This sharp quarter-over-quarter decline, with revenue plummeting 68.5% from Q2 2025, underscores a rapid deterioration of the company’s financial performance. For a detailed breakdown of the official figures, investors can review the Official Disclosure filed with the Financial Supervisory Service (DART).

Unpacking the Root Causes of the Underperformance

A multi-faceted crisis led to this Kakao earnings shock. The issues stem from both internal business unit struggles and external macroeconomic pressures that the company failed to navigate effectively.

1. Unexpected Headwinds in the Platform Business

Kakao’s platform businesses, including Talk Biz and Commerce, have long been the bedrock of its growth. However, Q3 saw these reliable engines falter. A slowdown in the digital advertising market, as noted by sources like Reuters, has impacted ad-revenue-dependent services globally. Concurrently, intensified competition from rivals in the e-commerce space has eroded margins and slowed transaction growth, putting unexpected pressure on this core segment.

2. Intensified Decline in the Content Division

While the content business showed signs of weakness in the first half of 2025, the slump deepened dramatically in Q3. The massive 69% revenue miss points to critical failures, likely a combination of underperforming new game launches, a weakening competitive edge in its webtoon and media offerings, and challenges in expanding its global footprint against established players.

The convergence of a global economic slowdown, high interest rates, and unfavorable currency exchange rates created a perfect storm, negatively impacting everything from consumer spending on Kakao’s platforms to the profitability of its overseas ventures.

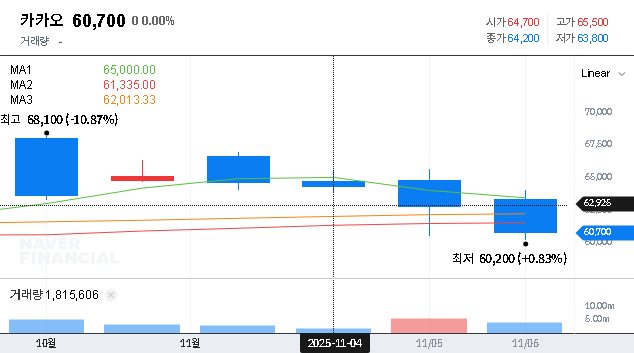

Impact on 035720 Stock and Investor Outlook

The repercussions of this severe earnings miss are likely to be swift and significant. The primary concern for investors is the immediate impact on the 035720 stock price, which is expected to face heavy downward pressure as the market digests this negative surprise. Beyond short-term volatility, there are longer-term implications for the company’s financial health and strategic position.

Sustained underperformance could trigger a credit rating downgrade by agencies, increasing borrowing costs and further damaging investor confidence. Furthermore, the results highlight a potential loss of market share to more agile competitors, a risk that threatens the company’s long-term fundamental value.

Action Plan for Kakao Corp. Investors

In light of this challenging Kakao investor analysis, a measured and strategic approach is required. Actions should be differentiated based on short-term risk management and long-term value assessment.

Short-Term (Next 1-3 Months)

- •Adopt a Cautious Stance: Given the high probability of a stock price decline, investors may consider reducing exposure or holding off on new purchases until the dust settles.

- •Monitor Management’s Response: Closely watch for official communications from Kakao’s leadership. A clear, credible plan to address the root causes is essential for restoring confidence.

Mid-to-Long-Term (6+ Months)

- •Evaluate Turnaround Potential: Assess whether the platform business can regain its footing and if the heavy investments in AI and data centers can begin to yield tangible results.

- •Reassess Valuation: After a potential price drop, the stock may present a new valuation. Investors must weigh this against the now-higher perceived risks to determine if it offers an attractive entry point for long-term growth. For more on valuation, you can read our guide on Understanding Kakao’s Core Business Model.

In conclusion, the Kakao Corp. earnings for Q3 2025 are a clear warning sign. Investors must remain vigilant, balancing the immediate risks with a careful evaluation of the company’s ability to navigate this crisis and execute a successful turnaround strategy.