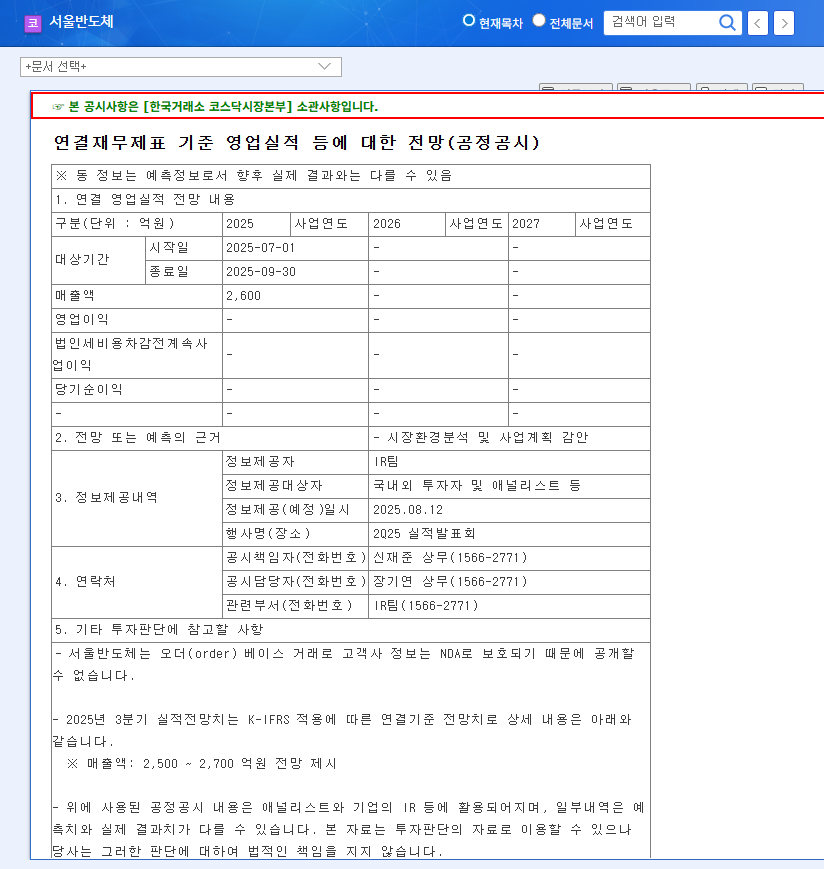

A sound Seoul Semiconductor investment strategy requires a clear understanding of the company’s current challenges and future potential. SEOUL SEMICONDUCTOR CO., LTD. (KOSDAQ: 046890) recently released a Q4 2025 revenue forecast of 260 billion KRW, a figure that has sent ripples of concern through the investment community. This projection signals a significant acceleration of the revenue decline observed in previous quarters, raising critical questions about profitability and the company’s path forward. For current and prospective investors, navigating this period of uncertainty is paramount. This comprehensive analysis will dissect the factors behind the bleak outlook, evaluate the company’s fundamental strengths and weaknesses, and provide actionable strategies for your Seoul Semiconductor stock portfolio.

The official Q4 2025 forecast represents a staggering 65% decrease compared to Q3 2025 revenue, highlighting the urgency for investors to reassess their positions and the company’s strategic response. The full details can be found in the Official Disclosure (DART).

Deconstructing the Q4 2025 Performance Deterioration

The projected drop in revenue is not an isolated event but the culmination of several persistent headwinds. The Q3 2025 results already painted a concerning picture, with revenue falling 9.4% year-over-year and the company swinging to an operating loss of 32.3 billion KRW. The Q4 forecast suggests these issues are intensifying, creating significant downward pressure on the 046890 stock analysis and overall market sentiment.

1. Macroeconomic and LED Market Analysis

Several external factors are contributing to Seoul Semiconductor’s difficulties. A broad global economic slowdown, as reported by major financial institutions, has dampened consumer and industrial demand for products that utilize LEDs, from smartphones and televisions to automotive lighting. Furthermore, the LED market analysis reveals intensified price competition, particularly from Chinese manufacturers, which erodes profit margins for established players. Compounding these issues is exchange rate volatility; a strengthening Korean Won against the US Dollar can significantly impact the profitability of an export-heavy company like Seoul Semiconductor.

2. Scrutinizing Financial Health and Cash Flow

A closer look at the balance sheet reveals emerging financial strain. While a debt-to-equity ratio of 81.6% is not yet alarming, its slight increase is a trend worth monitoring. More pressing is the contraction in liquidity, driven by a combination of falling current assets and high current liabilities. While operating cash flow saw some improvement, it was overshadowed by larger cash outflows for investing and financing activities, putting the company’s overall cash position under pressure. These financial metrics are critical for any long-term Seoul Semiconductor investment thesis.

The Beacon of Hope: Unwavering Technological Competitiveness

Despite the grim financial outlook, Seoul Semiconductor’s core strength remains its technological prowess. The company continues to invest heavily in its future, with R&D expenditure accounting for 10.9% of revenue. This commitment has resulted in a formidable portfolio of over 18,000 patents, creating a significant competitive moat.

- •Mini LED & Micro LED: These technologies are critical for the next generation of high-performance displays in premium TVs, monitors, and automotive dashboards. Mastering this area is key to future growth. For more details, you can read our guide on understanding Micro LED technology.

- •VCSEL (Vertical-Cavity Surface-Emitting Laser): A vital component for 3D sensing, facial recognition, and LiDAR systems used in smartphones and autonomous vehicles. Success here could open up vast new revenue streams.

Investor Action Plan: Navigating the 046890 Stock

Given the conflicting signals of poor short-term performance and strong long-term technology, investors must adopt a nuanced strategy.

Short-Term Strategy: Caution and Monitoring

The deeply negative Seoul Semiconductor Q4 2025 forecast will undoubtedly weigh on investor sentiment, likely causing continued downward pressure on the stock price. The lack of specific profit forecasts adds to the uncertainty. For short-term traders, a conservative ‘sell’ or ‘hold’ position is advisable. It is prudent to wait for clear signs of a turnaround, such as revenue stabilization or positive management guidance, before considering new positions.

Long-Term Investment Strategy: A Bet on Innovation

For long-term investors, the core Seoul Semiconductor investment thesis rests on its ability to commercialize its next-generation technologies. The key is to monitor whether its R&D leadership translates into tangible profit generation. Watch for new product announcements, major design wins with global brands, and improvements in gross margins as indicators that its technology is gaining market traction. A long-term position requires patience and a belief that innovation will ultimately triumph over cyclical market downturns.

Conclusion: A Cautious Path Forward

Seoul Semiconductor (046890) is at a critical juncture. The Q4 2025 earnings outlook is a clear negative signal that demands a cautious short-term approach. However, the company’s substantial investment in future technologies like Micro LED and VCSEL provides a potential pathway to recovery and long-term growth. A positive investment case can only be rebuilt when the company demonstrates effective cost controls, robust risk management, and, most importantly, tangible profitability improvements driven by its impressive innovation pipeline.