The latest KB Financial Group earnings report for the first half of 2025 has sent ripples through the investment community. Despite facing a landscape of domestic and global economic headwinds, the group delivered a significant ‘earnings surprise,’ outperforming analyst expectations and showcasing remarkable resilience. This comprehensive KB Financial analysis will unpack the key figures, explore the strategic drivers behind this success, and evaluate the potential risks and opportunities for investors considering KB Financial Group stock.

We will delve into the performance of its core subsidiaries, its advancements in digital finance, and its strategic positioning for future growth. Whether you are a current shareholder or a potential investor, this deep dive provides the critical insights you need to make an informed decision.

Unpacking the H1 2025 Financial Results

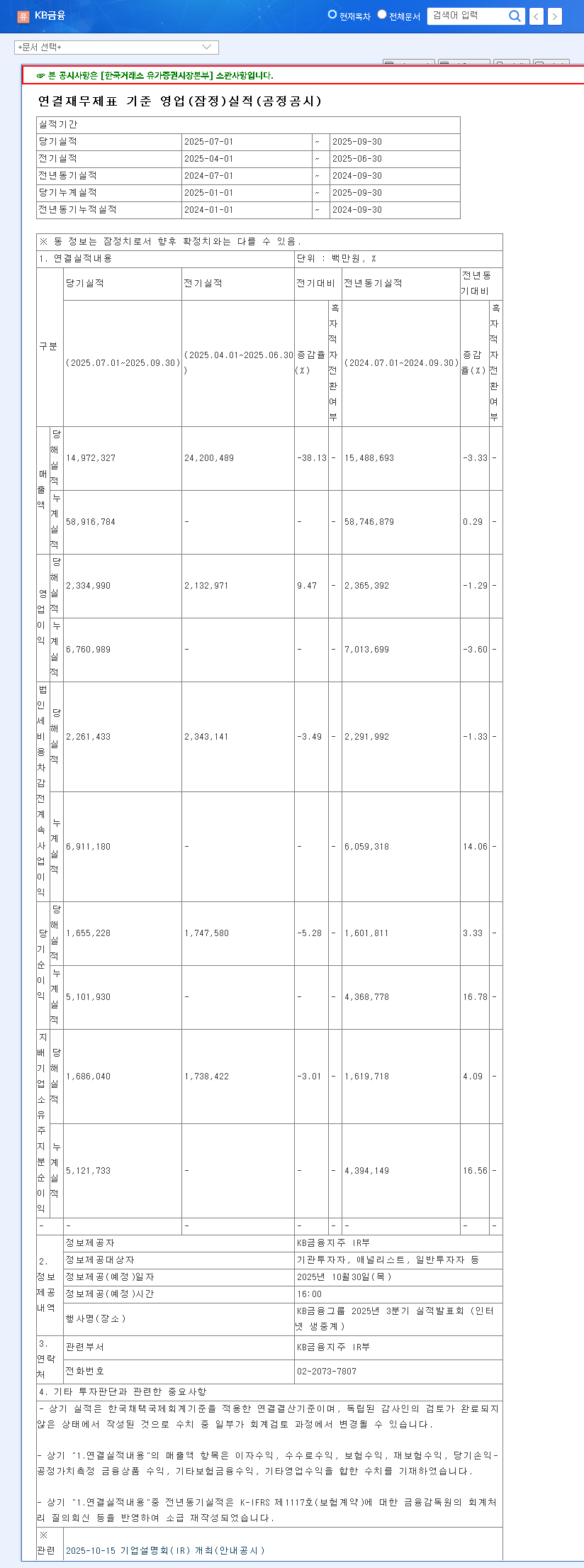

KB Financial Group Inc. announced its provisional H1 2025 financial results, posting a performance that comfortably surpassed market consensus. The numbers highlight the group’s robust operational strength and effective management. According to the Official Disclosure filed with DART, the key figures are:

- •Revenue: KRW 14,972.3 billion

- •Operating Profit: KRW 2,335.0 billion (Exceeding market expectation of KRW 2,135.5 billion)

- •Net Profit: KRW 1,686.0 billion (Exceeding market expectation of KRW 1,550.8 billion)

- •Year-on-Year Growth: Both operating and net profit increased by a healthy 9%.

These impressive metrics underscore KB Financial’s capacity for stable and profitable management even amidst significant market uncertainty, reinforcing confidence in the KB Financial Group stock as a solid long-term holding.

Core Growth Drivers: The Pillars of Success

The strong KB Financial Group earnings were not a matter of luck but the result of a well-executed strategy built on diversified strengths. The balanced performance across its key subsidiaries was the primary catalyst.

Synergy Across Key Subsidiaries

- •KB Kookmin Bank: The flagship banking arm generated solid interest income, driven by prudent loan growth and effective management of its Net Interest Margin (NIM).

- •KB Securities: Capitalizing on market dynamics, the securities division maintained stable operating strength through robust brokerage fees and growth in its Wealth Management (WM) business.

- •KB Insurance: Strategic profitability improvements, including an optimized loss ratio and growth in direct premiums, contributed significantly to the group’s bottom line.

KB Financial’s diversified portfolio has proven to be a powerful shield against market volatility, with non-banking segments increasingly contributing to overall profitability and de-risking the group’s revenue streams.

Advancements in Digital and AI Capabilities

A cornerstone of KB Financial’s forward-looking strategy is its aggressive digital transformation. The company is investing heavily to stay ahead of fintech challengers by enhancing user experience and operational efficiency. Key initiatives include the continuous advancement of its flagship mobile app, ‘KB Star Banking,’ and strengthening its cloud/AI business capabilities through KB Data Systems. This focus on technology is crucial for securing future growth and responding to evolving consumer behaviors.

Navigating Headwinds: Potential Risks and Challenges

While the H1 2025 performance is commendable, a thorough KB Financial analysis requires acknowledging the potential risks on the horizon. Investors should remain vigilant of these factors.

- •Macroeconomic Uncertainty: Persistent inflation, interest rate volatility, and geopolitical tensions could impact loan demand and credit quality. Investors should monitor global economic outlooks from authoritative sources like leading financial news agencies.

- •Intensified Competition: The rise of agile fintech firms and internet-only banks continues to pressure traditional financial institutions to innovate rapidly.

- •Real Estate PF Risk: The health of the real estate market is a critical factor. Potential downturns could expose the group to risks associated with its Project Financing (PF) loan portfolio, requiring stringent risk management.

- •Regulatory Scrutiny: As a systemically important financial institution, KB Financial is subject to rigorous oversight. Strengthening compliance and internal controls remains a continuous priority.

Investor Action Plan & Future Outlook

KB Financial Group has demonstrated strong fundamentals and a clear strategy for sustainable growth. Its stable revenue streams, diversified business model, and high credit ratings present a compelling investment case. However, the path forward depends on management’s ability to navigate the aforementioned risks while executing its growth initiatives.

Key factors for investors to monitor include the execution of its shareholder return policy (dividends, share buybacks), the tangible results from its digital investments, and its agility in responding to macroeconomic shifts. For a deeper understanding of valuation, investors may want to review our guide on how to analyze bank stocks. In conclusion, while caution is warranted due to external uncertainties, KB Financial’s robust performance and strategic direction offer a positive outlook for discerning investors.

Frequently Asked Questions (FAQ)

What were the highlights of KB Financial Group’s H1 2025 earnings?

KB Financial reported a major ‘earnings surprise’ with an operating profit of KRW 2,335.0 billion and a net profit of KRW 1,686.0 billion, both surpassing market expectations and growing 9% year-on-year.

What drove this strong financial performance?

The success was driven by the balanced, strong performance of its main subsidiaries: solid interest income from KB Kookmin Bank, stable operations at KB Securities, and improved profitability at KB Insurance.

What are the key risks for KB Financial Group stock?

Investors should monitor risks including macroeconomic volatility (interest rates, economic slowdown), fierce competition from fintech, potential real estate Project Financing (PF) exposure, and ongoing regulatory compliance needs.

How is KB Financial preparing for future growth?

The group is focused on securing future growth by diversifying its business portfolio, enhancing its digital and AI capabilities through significant technology investments, and expanding its presence in overseas markets.