When a major institutional investor like the National Pension Service (NPS) adjusts its holdings in a prominent company, the market takes notice. The recent news of the NPS reducing its stake in Kiwoom Securities has sent ripples through the investment community, leaving many to wonder: is this a warning sign, or a golden opportunity? This analysis delves deep into the situation, evaluating the strength of Kiwoom Securities’ fundamentals against the backdrop of this significant portfolio shift.

Instead of a knee-jerk reaction, savvy investors should see this as a moment to assess the company’s intrinsic value. We will dissect the short-term noise from the long-term potential, providing a clear perspective on whether the current market volatility presents a strategic entry point for buying Kiwoom Securities stock.

The NPS Announcement: What Exactly Happened?

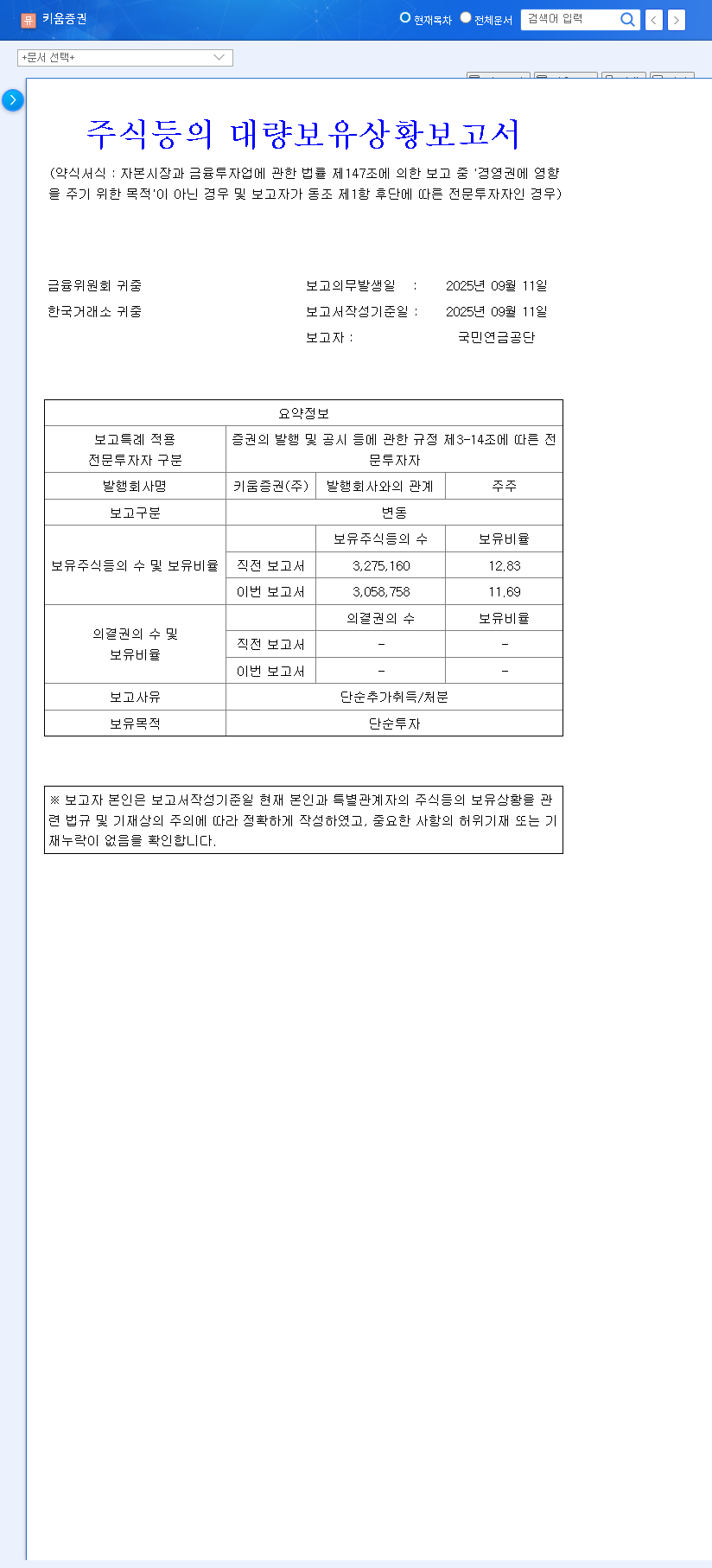

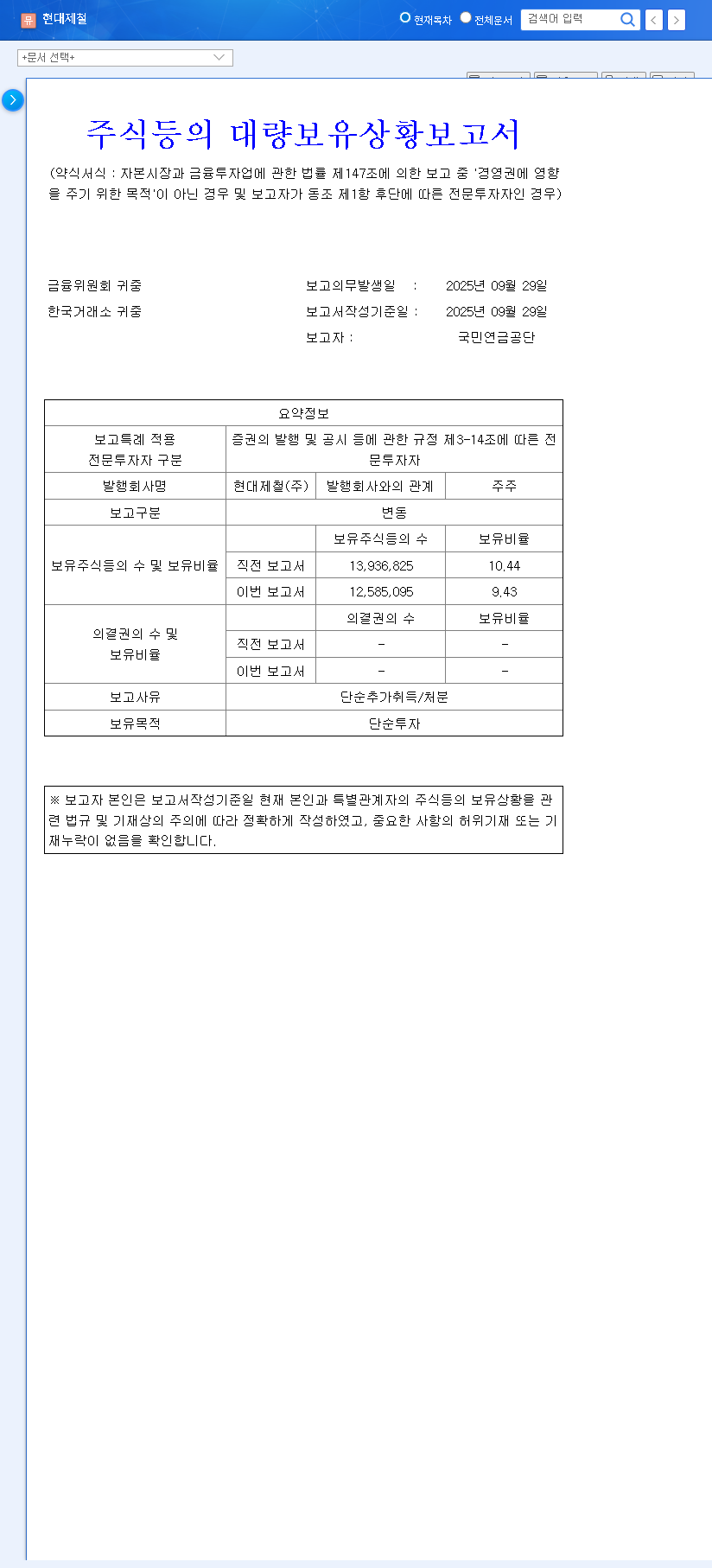

On September 29, 2025, the National Pension Service officially disclosed a reduction in its ownership of Kiwoom Securities Co., Ltd. (KRX: 039490). The pension fund’s stake decreased from 12.83% to 11.69%, a net reduction of 1.14 percentage points. The reason cited in the filing was a ‘simple additional acquisition/disposal’, suggesting the move is part of a broader portfolio rebalancing strategy rather than a targeted verdict on the company’s future. You can view the Official Disclosure on the DART system for full details. While any sale by a major holder can create short-term selling pressure, it is crucial to look beyond the headline and analyze the underlying health of the business.

Fundamental Analysis: Kiwoom Securities’ Robust H1 2025 Performance

Regardless of the NPS Kiwoom Securities news, the company’s performance in the first half of 2025 paints a picture of exceptional financial health and market leadership. The fundamentals suggest that its intrinsic value is stronger than ever.

1. Impressive Earnings Growth

Kiwoom Securities reported outstanding financial results, with a consolidated operating profit of KRW 733.8 billion (a 12.9% year-over-year increase) and a net profit of KRW 545.7 billion (a 14.4% YoY increase). This growth was fueled by a vibrant domestic stock market, the company’s dominant retail investor base, and well-balanced expansion in its Investment Banking (IB) and Sales & Trading (S&T) divisions.

2. Unshakeable Market Leadership

The company solidified its number one position in the domestic stock brokerage market, holding a 19.3% overall share and an impressive 29.5% share among retail investors. This demonstrates a deep competitive moat. Furthermore, Kiwoom has successfully diversified its revenue streams beyond brokerage, reducing its dependency on trading volumes alone.

3. Rock-Solid Financial Stability

With a consolidated net capital ratio of 1,344.47%, Kiwoom Securities boasts top-tier financial stability, far exceeding regulatory requirements. This massive capital buffer allows it to navigate market volatility with ease and provides a strong foundation for future growth. Its healthy liquidity ratio of 113% further underscores its excellent risk management.

Decoding the Market Impact: Short-Term Jitters vs. Long-Term Outlook

The short-term reaction to the NPS sale may cause temporary weakness in Kiwoom Securities stock due to negative investor sentiment. However, this is likely to be a transient effect, as the sale is not linked to any fundamental flaw in the company’s operations.

In the long term, this event could even be beneficial. The increase in the free float of shares can lead to higher trading liquidity, making the stock more attractive to a wider range of investors. As the market absorbs these shares, the focus will inevitably return to the company’s strong performance and growth trajectory. To better understand these concepts, you can learn more in our guide on fundamental analysis for stocks.

The Macro Environment and Investment Thesis

Kiwoom Securities operates within a global macroeconomic context. Current interest rate policies from central banks like the U.S. Federal Reserve provide a relatively stable environment for interest income. While currency fluctuations and shifts in global trade can present challenges, Kiwoom’s diversified business model and strong domestic footing provide significant insulation. The core driver of its value remains its ability to serve its massive client base and capitalize on capital market activities.

Based on stellar H1 2025 earnings, dominant market position, and robust financial health, the investment opinion on Kiwoom Securities remains a confident ‘Buy’. The NPS stake reduction should be viewed as short-term market noise, not a red flag.

Recommended Investment Strategy

- •Utilize any price dips caused by the NPS disclosure as a strategic opportunity for staggered, long-term accumulation of Kiwoom Securities stock.

- •Focus on the company’s powerful fundamentals and long-term growth prospects rather than short-term market sentiment.

- •Continuously monitor Kiwoom’s commitment to its shareholder return policies, such as share buybacks, which further enhance investor value.

Frequently Asked Questions

Why did the NPS sell its shares in Kiwoom Securities?

The official disclosure states the reason as ‘simple investment purposes.’ This strongly implies the sale was part of a routine portfolio rebalancing or profit-taking strategy, not a negative assessment of Kiwoom’s future.

What is the likely impact on Kiwoom Securities’ stock price?

In the short term, the price may experience some volatility or weakness. However, because the company’s fundamentals are exceptionally strong, this effect is not expected to last. Over the long term, the increased share liquidity could be a net positive.

Is Kiwoom Securities still considered a good investment?

Yes. Based on its powerful earnings growth, market leadership, and solid financial health demonstrated in H1 2025, the investment outlook for Kiwoom Securities remains highly positive. The current situation may represent a valuable buying opportunity for long-term investors.