This comprehensive Seegene stock analysis delves into the company’s recent Q3 2025 earnings report. While the numbers fell short of market expectations, causing immediate concern among investors, a deeper look reveals a more complex picture. Does this dip represent a temporary hurdle or a fundamental flaw in Seegene’s growth story? We will dissect the financials, evaluate the technological advantages, and provide a clear Seegene investment outlook for stakeholders.

Decoding the Seegene Q3 2025 Earnings Report

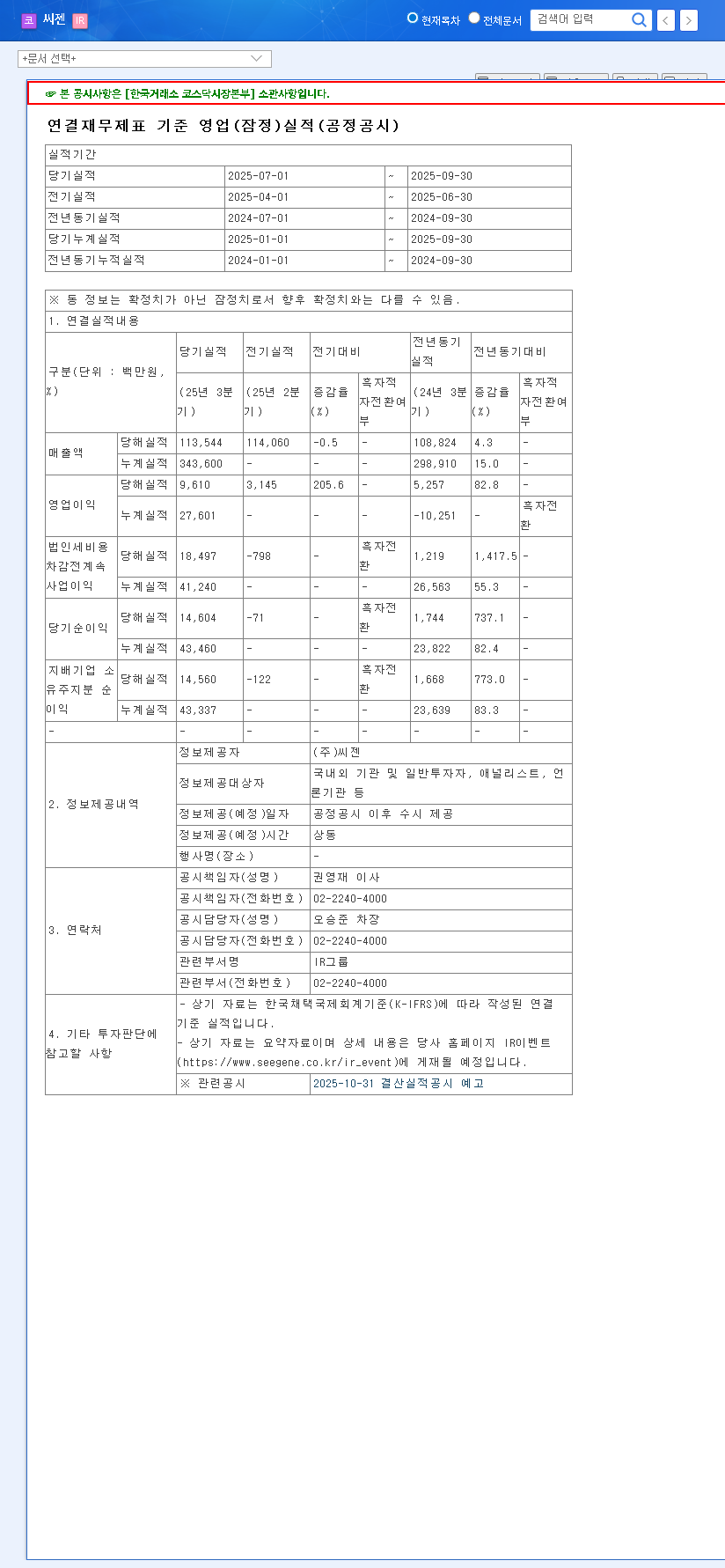

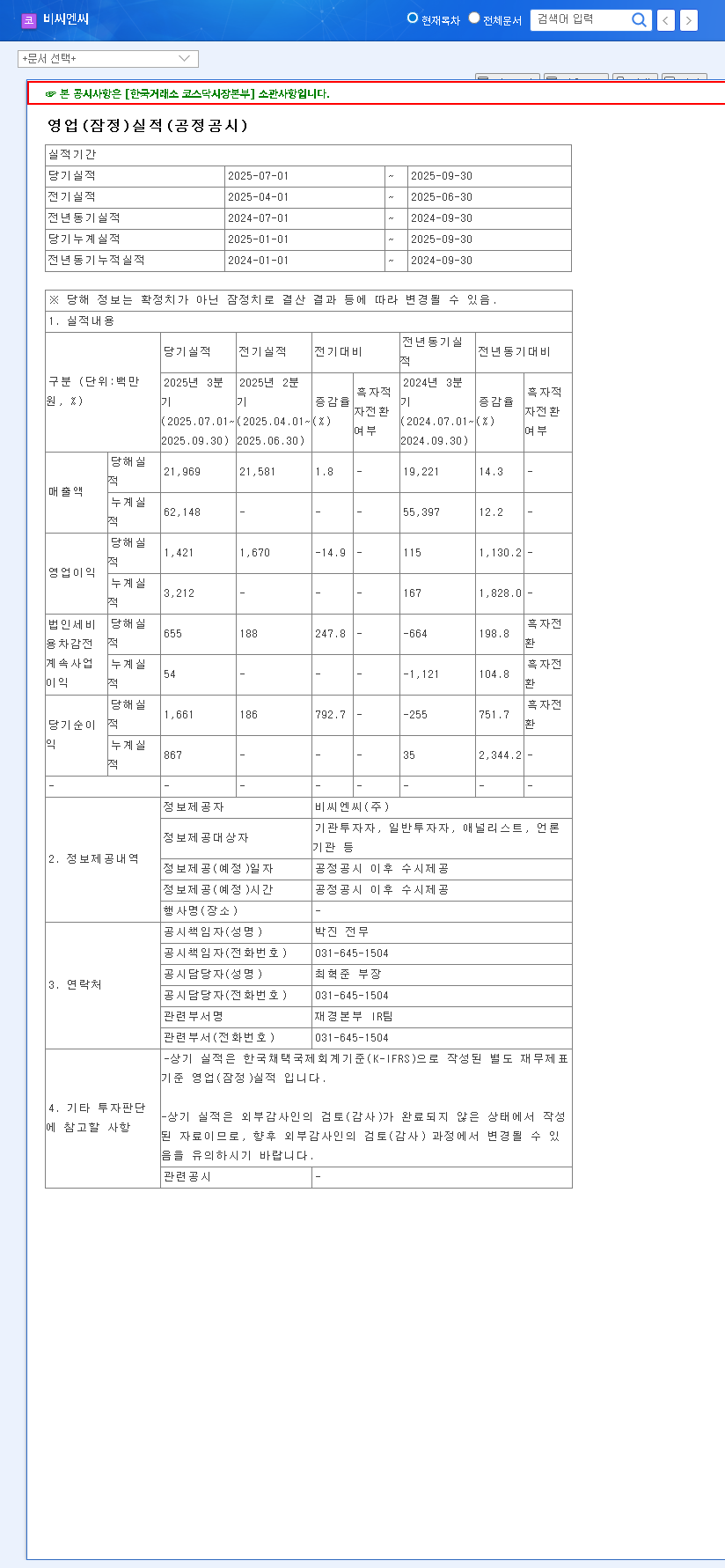

On November 7, 2025, SEEGENE, INC. (Seegene) announced its preliminary consolidated financial results for the third quarter. The report immediately triggered discussions due to key metrics missing consensus estimates. The complete preliminary results were filed, and the Official Disclosure is available for public review.

Key Financial Highlights:

- •Revenue: KRW 113.5 billion, which was 9% below the market estimate of KRW 125 billion.

- •Operating Profit: KRW 9.6 billion, falling 14% short of the market’s expectation of KRW 11.2 billion.

- •Net Profit: KRW 14.6 billion.

While these figures might cause short-term pressure on the stock, it’s important to note that revenue has been relatively stable since late 2024, and the company has maintained profitability since Q2 2024, indicating a resilient operational base.

Seegene Financial Analysis: Beyond the Headlines

To form a complete picture, a thorough Seegene financial analysis must look past a single quarter’s performance and evaluate the core pillars of the business: its financial health, technological moat, and market position.

Robust Financial Bedrock

Based on the 2025 semi-annual report, Seegene’s financial foundation is remarkably strong. Revenue grew 21% year-over-year, and both operating and net profit turned positive, signaling a significant performance turnaround. Key indicators of financial stability include a very low debt-to-equity ratio of 0.22% and a substantial treasury share holding of 11.7%, which can be used to enhance shareholder value.

Unpacking Seegene’s Technological Moat

Seegene’s competitive edge is anchored in its proprietary Syndromic Quantitative PCR technology. This allows for ‘High Multiplex’ diagnostics, where a single patient sample can be tested for numerous pathogens simultaneously. This capability provides a comprehensive diagnostic picture far more quickly and efficiently than traditional methods. This leadership is protected by 36 core patents and has led to 124 product approvals globally. Furthermore, the ‘SG OneSystem™’ initiative, alongside strategic collaborations with giants like Microsoft and Springer Nature, is enhancing its AI capabilities and global reach.

While the Q3 earnings miss may cause short-term turbulence, Seegene’s underlying fundamentals and technological leadership suggest a resilient long-term trajectory.

Riding the Wave of a Growing Market

Seegene operates within the global In-Vitro Diagnostics (IVD) market, which is projected to grow to USD 119.4 billion by 2030 at a CAGR of 6.75%, according to market analysis from leading firms like Grand View Research. The molecular diagnostics segment, Seegene’s specialty, is a key driver of this growth. This expanding market provides a powerful tailwind for the company’s long-term ambitions.

Balancing a Cautious Seegene Investment Outlook

The Q3 report creates a duality for investors: clear short-term risks balanced against promising long-term potential. A sound Seegene investment outlook requires weighing both sides carefully.

The Bull Case: Reasons for Optimism

- •Improving Fundamentals: Sustained profitability and year-over-year revenue growth point to strengthening core operations.

- •Technological Leadership: Core multiplex technology provides a durable competitive advantage.

- •Strategic Expansion: Proactive M&A and global expansion efforts are paving the way for future growth.

The Bear Case: Key Risks to Monitor

- •Market Sentiment: Missing estimates can negatively impact investor confidence in the short term.

- •High Export Dependency: With 93% of sales from exports, the company is exposed to exchange rate volatility. Learn more about managing currency risk in a portfolio.

- •Macroeconomic Headwinds: Rising interest rates could increase borrowing costs, and contingent liabilities from acquisitions pose a potential financial risk.

Investor Takeaway and Action Plan

In conclusion, our Seegene stock analysis reveals a company at a crossroads. The short-term narrative is dominated by the earnings miss, but the long-term story is one of strong Seegene fundamentals, technological superiority, and strategic growth. Investors should monitor short-term price volatility while continually reassessing the company’s long-term growth trajectory against the identified market and financial risks. A patient, well-informed approach is paramount.