The latest C&C International earnings report for Q3 2025 has sent ripples through the market, leaving many investors questioning the company’s immediate future. The provisional results revealed a significant miss on operating profit, raising valid concerns about short-term stock performance and investor sentiment. But does this quarterly stumble signal a fundamental flaw in the company’s long-term strategy, or is it merely a speed bump on the path to sustained growth? This comprehensive C&C International stock analysis will dissect the numbers, explore the underlying causes of the underperformance, and provide a clear, actionable outlook for investors.

Breaking Down the C&C International Q3 2025 Earnings Report

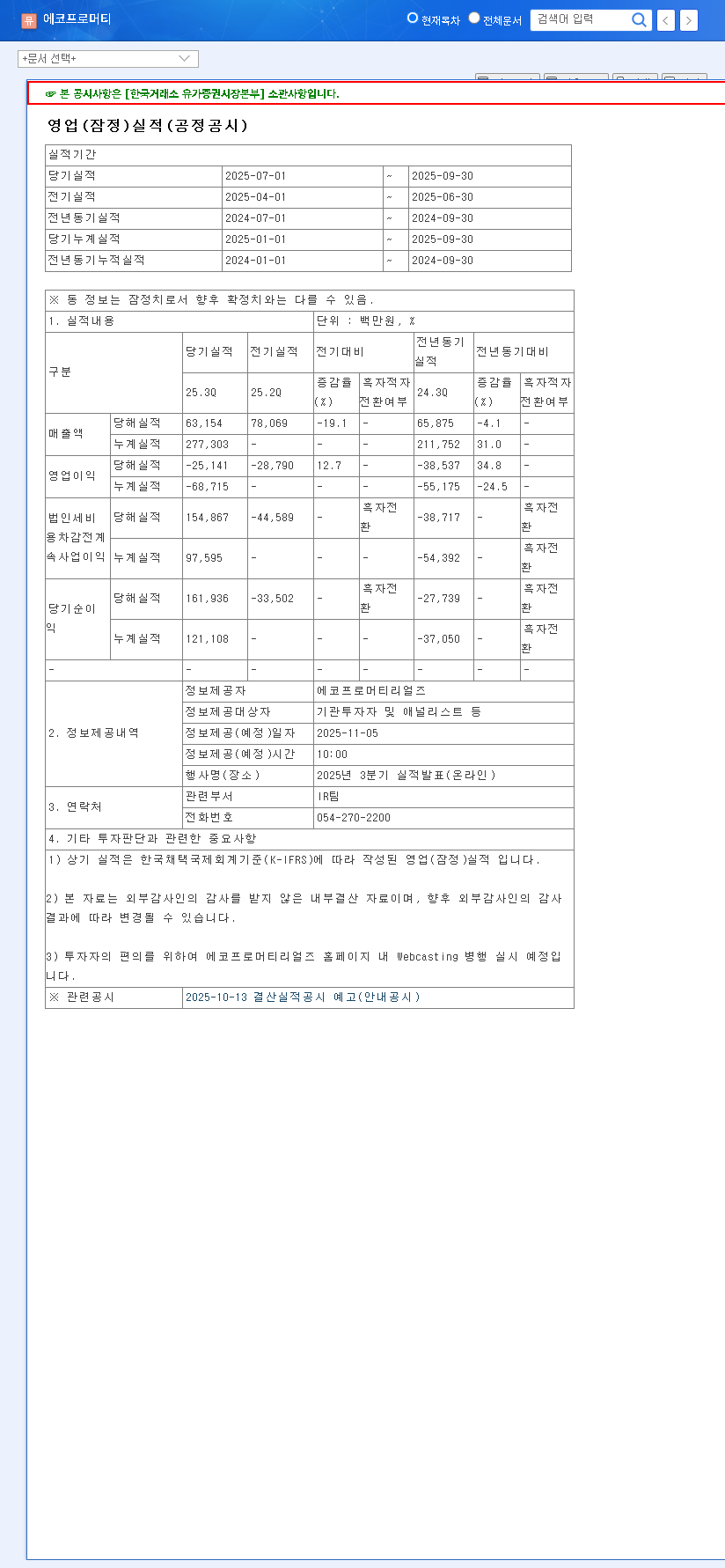

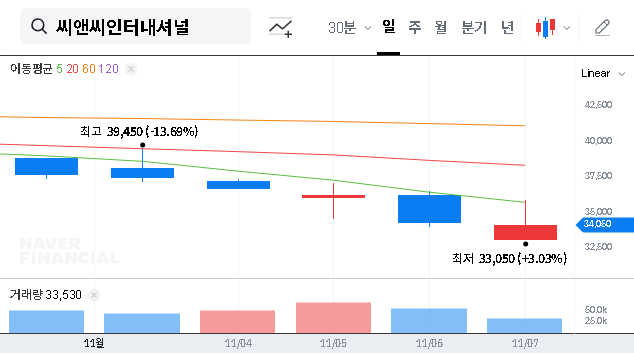

C&C International Co., Ltd. officially announced its provisional earnings for the third quarter of 2025, with several key metrics falling short of consensus estimates. The most notable deviation was in operating profit, which is a critical indicator of core business profitability. You can view the full filing directly from the source. Official Disclosure.

Key Financial Metrics at a Glance

- •Revenue: KRW 75.4 billion, missing estimates by a narrow 1.47%.

- •Operating Profit: KRW 6.9 billion, a significant 28.13% below estimates.

- •Net Profit: KRW 7.5 billion, missing estimates by a slight 1.32%.

The core issue isn’t a decline in sales, but a sharp squeeze on profitability. The 28% miss in operating profit, despite a minor revenue dip, points squarely towards rising internal costs and strategic spending rather than a collapse in market demand.

Why Did Operating Profit Fall Short of Expectations?

To understand the future, we must first understand the past. The gap in performance wasn’t caused by a single issue but a confluence of strategic decisions and operational factors that temporarily impacted the bottom line. These factors are crucial for any thorough C&C International stock analysis.

Strategic Investments in Future Growth

The company has increased its investment in Research & Development (R&D) to secure future growth engines and stay ahead in the competitive cosmetic ODM market. Similarly, initial costs associated with launching new business ventures have been incurred. While these expenditures depress current profits, they are essential for long-term innovation and market expansion.

Rising Operational Costs (SG&A)

A primary driver of the profit miss appears to be a notable increase in Selling, General, and Administrative (SG&A) expenses. This can include higher marketing spend, increased headcount, or other operational overheads. Investors will need to monitor if this is a temporary surge or a new, higher baseline for operating costs.

C&C International Stock Analysis: Short-Term Pain vs. Long-Term Gain

Given the Q3 2025 earnings miss, the stock is likely to face headwinds. However, a prudent investor must weigh the immediate market reaction against the company’s fundamental, long-term prospects.

Positive Catalysts for Growth

- •Strong Industry Tailwinds: The global cosmetic ODM industry continues to expand, fueled by the rise of indie beauty brands, the growth of e-commerce, and the enduring global appeal of K-Beauty. Learn more in our Comprehensive Guide to the K-Beauty Market.

- •Future Growth Drivers: The current pain from R&D and new business spending could transform into future gains as these initiatives bear fruit.

- •Core Competencies: C&C International maintains key competitive strengths, including robust in-house product planning and a deep understanding of customer needs.

Potential Headwinds to Monitor

- •Profitability Concerns: A sustained increase in SG&A expenses could permanently hinder profitability if not managed effectively.

- •Macroeconomic Pressures: Rising interest rates can increase financing costs, while exchange rate volatility can impact both revenue and the cost of imported raw materials.

- •Intense Competition: The K-Beauty and cosmetic ODM space is highly competitive, requiring continuous innovation to maintain market share.

An Actionable Investment Strategy

In light of the recent C&C International earnings report, a one-size-fits-all approach is unwise. Your strategy should align with your investment timeline and risk tolerance.

For the Short-Term & Cautious Investor

A conservative stance is warranted. The market is likely to punish the stock for the profit miss. It would be prudent to wait for the dust to settle, observe the stock’s price action in the coming weeks, and await further guidance from the company on its Q4 outlook before considering a new position.

For the Patient Long-Term Investor

For those with a longer horizon, this could present a buying opportunity, but it requires careful monitoring. Key areas to watch in subsequent C&C International earnings calls and reports include management’s ability to control SG&A costs, tangible results from R&D spending (e.g., new product lines or major client wins), and trends in key client orders. For more on long-term investing principles, see this excellent guide from a high-authority site like Investopedia.

In conclusion, while the Q3 2025 earnings report presents a clear short-term challenge, the long-term growth story for C&C International and the broader cosmetic ODM industry is not necessarily broken. Cautious, informed decision-making based on future performance will be paramount.