The latest DS DANSUK earnings report for Q3 2025 has captured significant market attention, revealing a pivotal turnaround in operating profit. DS DANSUK CO., LTD. (KRX: 017860) announced provisional earnings that signal a potential recovery, yet also highlight persistent financial challenges. This comprehensive analysis will dissect the DS DANSUK Q3 2025 performance, evaluate its underlying fundamentals, and provide a forward-looking investment strategy for investors monitoring the company’s stock trajectory.

While the swing back to operating profitability is a significant milestone, the persistent net loss and macroeconomic headwinds require a cautious and informed investment approach. We will explore both the opportunities and the risks ahead.

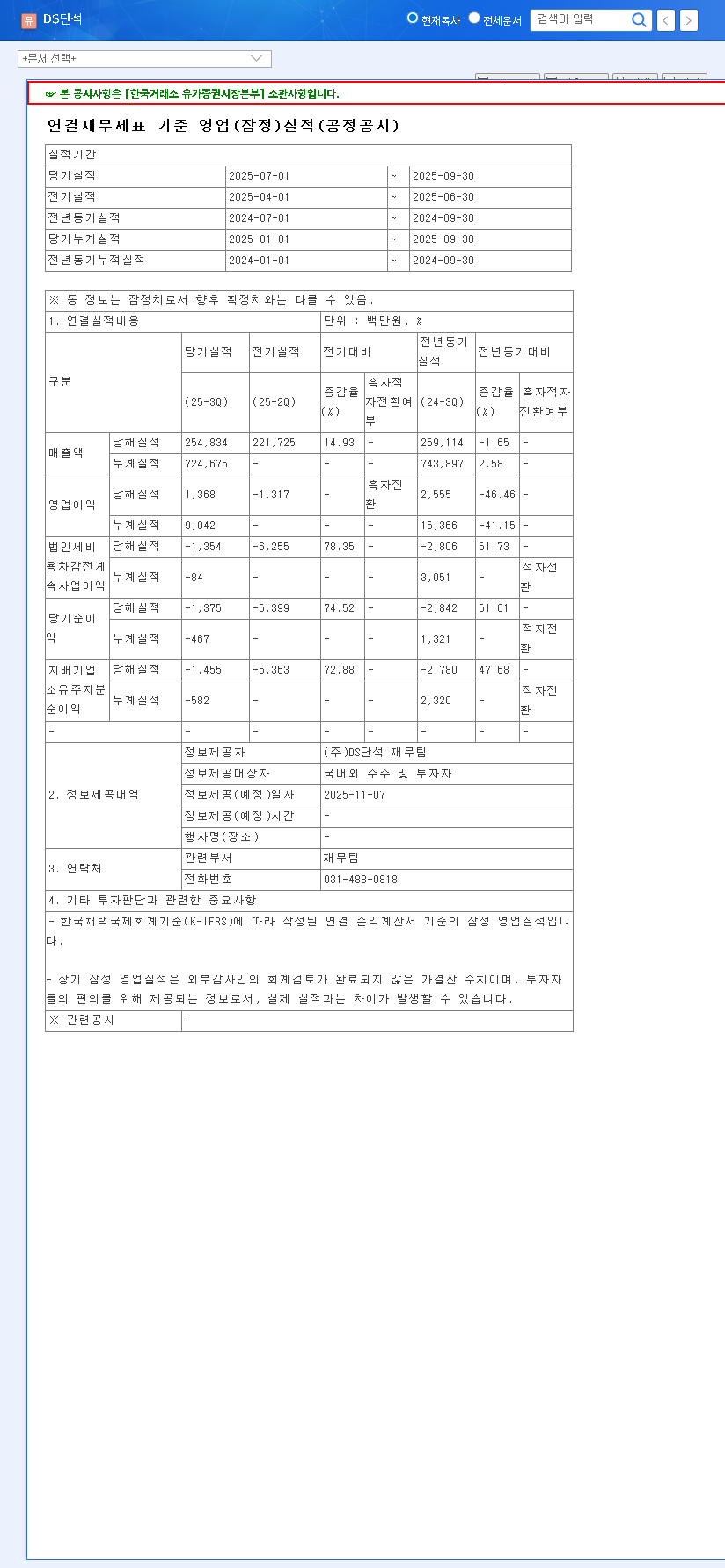

Deep Dive into DS DANSUK’s Q3 2025 Earnings Report

The provisional results for the third quarter present a mixed but cautiously optimistic picture. The headline figures, which you can verify in the Official Disclosure (DART), show a significant sequential improvement.

Key Financial Metrics Unpacked

- •Revenue: Reached KRW 254.8 billion, a healthy 14.9% increase from the previous quarter (QoQ), signaling a rebound in business activity.

- •Operating Profit: A notable turnaround to KRW 1.4 billion from a loss of KRW 1.3 billion in Q2 2025. This suggests that operational efficiency measures and cost controls are beginning to yield results.

- •Net Income: Remained in the red at KRW -1.5 billion. While still a loss, it’s a significant improvement from the KRW -5.4 billion loss in the prior quarter, indicating that non-operating pressures are easing but not eliminated.

This quarterly performance, when viewed against the volatile backdrop of the past year, marks a critical inflection point. The company has navigated from a KRW 3.2 billion operating loss in Q4 2024 to a KRW 9.0 billion profit in Q1 2025, followed by a dip back into loss in Q2. The Q3 recovery suggests a potential stabilization, which is a core tenet of our DS DANSUK investment strategy.

The Dual Narrative: Recovery Signals vs. Lingering Risks

Understanding the future of DS DANSUK requires balancing the promising aspects of its business model with the very real challenges it faces in the current economic climate.

The Bull Case: ESG Tailwinds and Operational Gains

The positive momentum is rooted in both internal improvements and external market trends. The operating profit turnaround is not just a number; it reflects tangible progress in cost management and production efficiency. Furthermore, DS DANSUK’s core business segments—bio-energy, battery recycling, and plastic recycling—are perfectly aligned with global ESG (Environmental, Social, and Governance) mandates. As governments and corporations worldwide intensify their focus on sustainability, the demand for DS DANSUK’s services is set for long-term structural growth. This trend is well-documented by major financial news outlets like Reuters’ Sustainable Business section.

The Bear Case: Financial Burdens and Macroeconomic Headwinds

Despite the operational recovery, significant hurdles remain. The persistent net loss is a major concern, primarily driven by high interest expenses from a substantial debt load. This financial burden restricts flexibility and reinvestment capacity. Moreover, the company is exposed to several macroeconomic risks:

- •Currency & Commodity Volatility: Fluctuations in the won/dollar exchange rate and international oil prices directly impact the profitability of its bio-energy division.

- •Capacity Utilization: Key divisions like plastic recycling are still operating at low utilization rates, which hampers overall profitability until demand or operational throughput increases.

- •Interest Rate Environment: A prolonged period of high global interest rates will continue to strain the company’s finances due to its debt obligations.

Investment Outlook and Strategic Recommendations

Given the complex factors at play, a nuanced investment approach is necessary. A thorough DS DANSUK stock analysis must differentiate between short-term catalysts and long-term value drivers.

Short-Term (1-3 Months)

The positive Q3 2025 earnings could provide a short-term boost to investor sentiment, potentially leading to a technical rebound in the stock price. However, the persistent net loss and recent stock declines may cap this upside. Investors should watch for follow-through momentum and signs that the market believes this recovery is sustainable.

Mid-to-Long-Term (6+ Months)

The long-term thesis rests on two pillars: sustained profitability and the successful execution of its ESG-centric business model. For long-term value to be unlocked, DS DANSUK must:

- •Achieve a consistent net profit turnaround to begin deleveraging and strengthening its balance sheet.

- •Increase capacity utilization in its core recycling segments to improve margins.

- •Show concrete progress and revenue generation from any announced new business ventures.

The company’s alignment with powerful trends in the circular economy is its greatest asset. For more information on this topic, you can read our guide to circular economy investing.

Conclusion: A Cautious but Watchful Stance

The DS DANSUK Q3 2025 earnings report marks a hopeful step forward, but the journey to sustainable profitability is far from over. Investors should view this as a potential turnaround story that is still in its early stages. A prudent strategy involves closely monitoring the upcoming Q4 earnings and the company’s 2026 business plan for concrete evidence that the operational improvements are durable and that a plan is in place to resolve the underlying financial weaknesses. The potential is significant, but the risks demand careful and continuous evaluation.