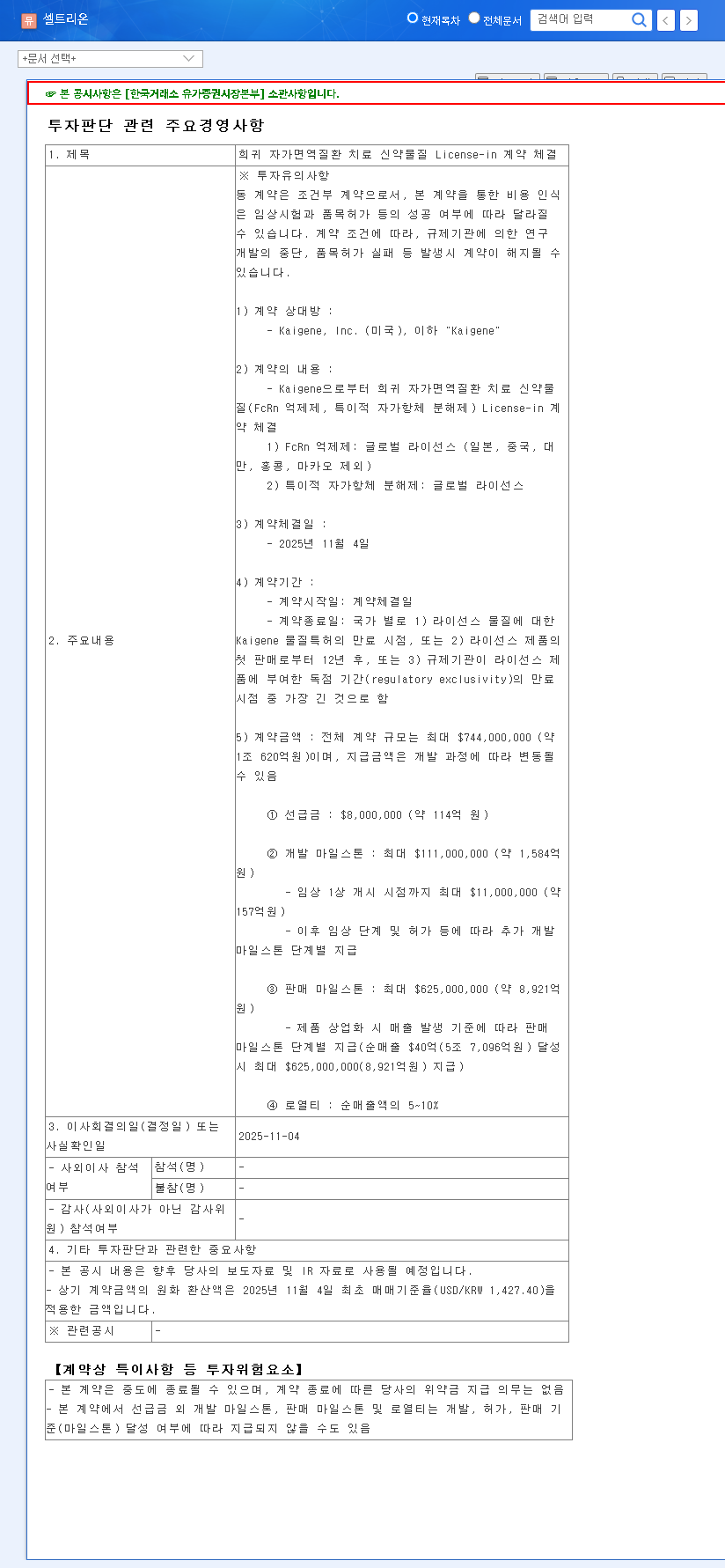

In a landmark move signaling a strategic pivot, global biopharmaceutical giant Celltrion, Inc. has made a significant investment into the future of innovative medicine. The company recently announced a major licensing agreement for a promising new rare autoimmune disease drug, solidifying its commitment to evolving beyond its biosimilar stronghold. This deal, valued at up to $744 million, involves novel drug candidates from Kaigene Inc. and is poised to become a new growth engine, capturing the attention of investors and the pharmaceutical industry alike.

This comprehensive analysis will dissect the agreement, explore the science behind the technology, weigh the potential rewards against the inherent risks, and provide a clear roadmap for stakeholders monitoring Celltrion’s ambitious journey.

Dissecting the Landmark Agreement

On November 4, 2025, Celltrion formalized a global license-in agreement with Kaigene Inc., securing the rights to two pioneering drug candidates targeting rare autoimmune diseases. As detailed in the Official Disclosure, this strategic acquisition focuses on an FcRn inhibitor and a specific autoantibody degrader. This move is a cornerstone of Celltrion’s ‘Vision 2030’, aiming to generate 40% of its sales from innovative new drugs.

The Financial Framework

- •Total Deal Value: Up to $744 million (approximately KRW 1.062 trillion).

- •Upfront Payment: An initial investment of $8 million to secure the license.

- •Milestone Payments: Up to $111 million tied to specific development and regulatory achievements.

- •Royalties & Sales Milestones: A tiered royalty structure of 5-10% on net sales, plus additional payments based on commercial success.

The Strategic Rationale: Targeting the High-Value Rare Disease Market

Celltrion’s decision to acquire this rare autoimmune disease drug candidate is a calculated move to diversify away from its highly successful, yet increasingly competitive, biosimilar portfolio. The rare disease market, often referred to as the orphan drug market, offers unique advantages, including higher pricing power, extended market exclusivity, and often a more streamlined regulatory pathway. For more context, you can explore our guide on Understanding Biosimilars vs. Innovative Drugs.

“This is more than just a pipeline expansion; it’s a statement of intent. Celltrion is leveraging its robust cash flow from biosimilars to become a fully-integrated, innovative pharmaceutical powerhouse. The FcRn inhibitor space is hot, and this deal places them squarely in the game.”

What is an FcRn Inhibitor?

FcRn inhibitors represent a cutting-edge class of drugs. In many autoimmune diseases, the body mistakenly produces antibodies (IgG) that attack its own tissues. The neonatal Fc receptor (FcRn) is a protein that normally protects these antibodies from being broken down, extending their lifespan. An FcRn inhibitor works by blocking this receptor, which causes the harmful autoantibodies to be cleared from the body more rapidly. This mechanism has shown significant promise in treating conditions like myasthenia gravis, chronic inflammatory demyelinating polyneuropathy (CIDP), and others. For a deeper scientific perspective, the National Institutes of Health (NIH) provides extensive research on this topic.

Weighing the Opportunity Against the Risk

While the long-term potential is immense, this venture into innovative new drug development comes with a distinct set of challenges that investors must carefully consider.

Positive Catalysts for Growth

- •Enhanced Corporate Value: Successful development would transition Celltrion’s valuation model from a stable biosimilar manufacturer to a high-growth innovative pharma company.

- •Portfolio Diversification: Reduces reliance on any single market segment and opens up substantial new revenue streams.

- •Strengthened R&D Credibility: A successful clinical program would significantly boost market confidence in Celltrion’s R&D capabilities.

Potential Risks and Headwinds

- •Clinical Trial Uncertainty: The path from pre-clinical to commercialization is long and fraught with risk. The majority of drug candidates fail during Phase II or Phase III trials.

- •Fierce Competition: The FcRn inhibitor market is competitive, with established players like argenx (Vyvgart) and UCB. Celltrion must demonstrate a clear clinical or commercial advantage.

- •Financial Burden: The upfront and milestone payments are just the beginning. The costs of running global clinical trials are substantial and could impact short-term profitability.

- •Macroeconomic Factors: As a USD-denominated deal, fluctuations in the KRW/USD exchange rate could significantly alter the final cost.

Investor Action Plan: What to Monitor

For investors, this high-stakes venture requires careful and continuous monitoring. Key inflection points will determine the success of this Celltrion rare autoimmune disease drug project.

- •Clinical Trial Data Readouts: Pay close attention to announcements regarding the outcomes of Phase I (safety), Phase II (efficacy), and Phase III (pivotal) trials. Positive data will be a major stock catalyst.

- •Regulatory Filings and Approvals: Monitor filings with major regulatory bodies like the FDA and EMA. Approval in these key markets is critical for commercial success.

- •Quarterly Financials: Track the company’s R&D spend and cash flow to ensure the development costs are being managed effectively without unduly straining the core business.

- •Competitive Landscape: Keep an eye on the progress of competitors in the FcRn inhibitor and broader autoimmune disease space.

In conclusion, Celltrion’s deal with Kaigene Inc. is a bold and potentially transformative step. While it introduces new risks, it also unlocks a new frontier of growth that could redefine the company’s future for decades to come.